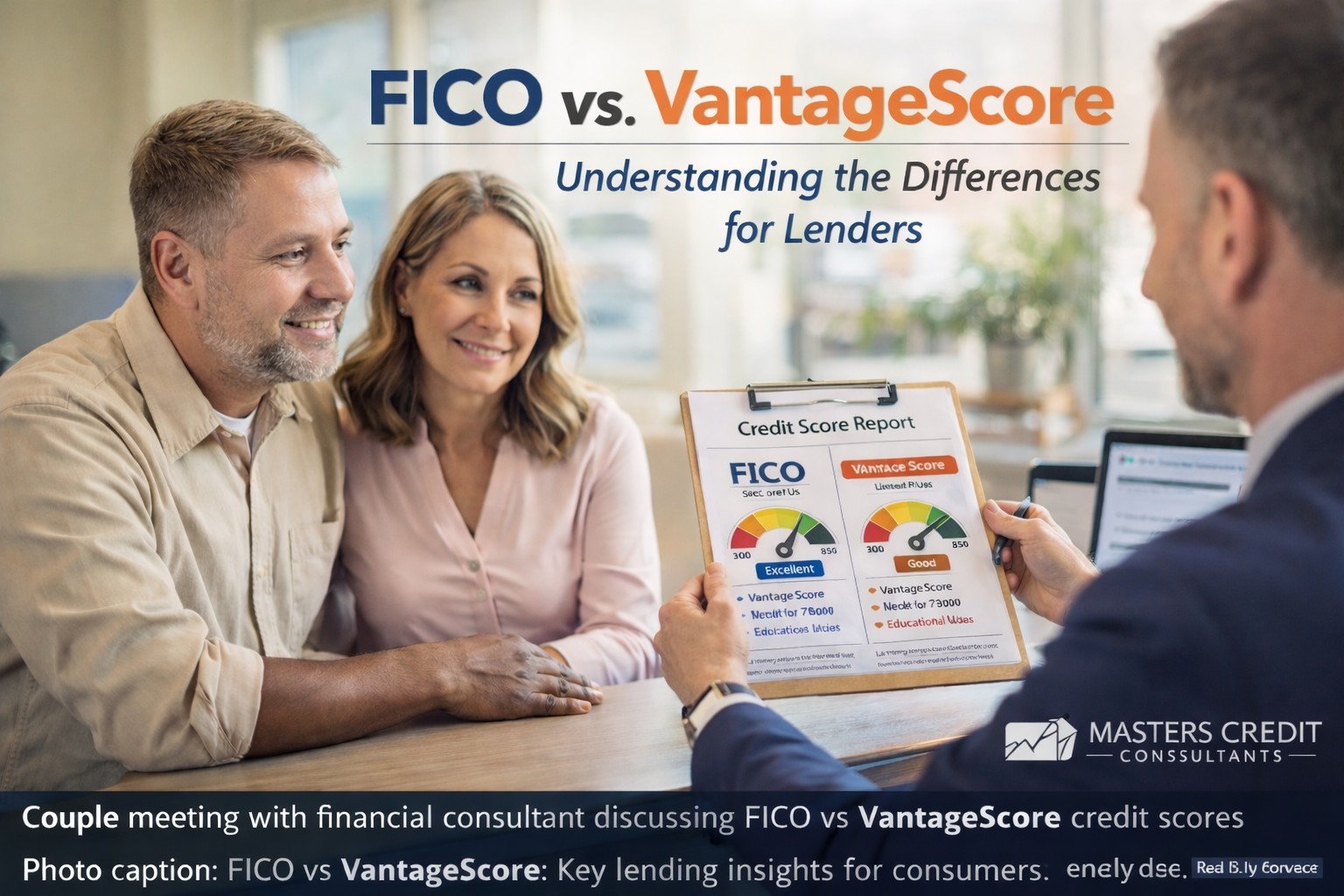

Why Understanding FICO vs VantageScore Models Matters Today

(FICO vs VantageScore model explained for real-world lending)

First, most consumers see multiple scores online.

However, lenders rarely view those scores equally.

Therefore, understanding the difference prevents costly surprises.

Additionally, credit decisions affect homes, cars, and business funding.

Consequently, model confusion can delay approvals or increase rates.

What Is the FICO Score Model?

(FICO vs VantageScore model explained with lender priority)

The FICO Score is the most widely used model.

Importantly, it was created by Fair Isaac Corporation.

Moreover, about 90% of top lenders rely on FICO scores.

Therefore, FICO remains the gold standard.

FICO Score Factors

Payment history (35%)

Amounts owed (30%)

Length of credit history (15%)

Credit mix (10%)

New credit (10%)

Because weighting is strict, small mistakes matter.

As a result, precision credit repair becomes critical.

What Is the VantageScore Model?

(FICO vs VantageScore model explained for consumer platforms)

VantageScore was created by Experian, Equifax, and TransUnion.

Notably, it was designed for broader access.

Additionally, VantageScore can score thinner files.

Therefore, newer consumers often see VantageScore first.

VantageScore Factors

Payment history

Depth of credit

Credit utilization

Balances

Recent credit behavior

However, lender adoption remains limited.

Thus, visibility does not equal lender acceptance.

Key Differences: FICO vs VantageScore Model Explained Side-by-Side

| Category | FICO | VantageScore |

|---|---|---|

| Lender Usage | Extremely high | Limited |

| Score Range | 300–850 | 300–850 |

| Thin Files | Harder | Easier |

| Industry Versions | Many | Few |

Therefore, consumers often see higher VantageScores.

However, lenders usually pull FICO.

Which Credit Score Do Lenders Actually Use?

(FICO vs VantageScore model explained for approvals)

Mortgage lenders primarily use FICO 2, 4, and 5.

Auto lenders often use FICO Auto Scores.

Credit cards almost always use FICO 8 or 9.

Meanwhile, VantageScore is mainly educational.

Thus, relying on it alone is risky.

Why Your Scores Can Be So Different

(FICO vs VantageScore model explained through scoring logic)

First, models weigh behaviors differently.

Next, reporting timing affects calculations.

Finally, dispute handling impacts each model uniquely.

Consequently, one model may jump quickly.

Meanwhile, the other may lag.

How Credit Repair Impacts FICO vs VantageScore

(FICO vs VantageScore model explained with strategy)

Because FICO is stricter, repair must be compliant.

Therefore, aggressive “credit sweeps” often fail.

Instead, verified disputes and data accuracy matter.

As a result, ethical credit repair wins long-term.

👉 Masters Credit Consultants focuses on FICO-driven outcomes.

Moreover, strategies are lender-tested and compliant.

🔍 The Biggest Mistake Consumers Make

Although free apps show scores, lenders rarely use them.

Therefore, always optimize for FICO first, not vanity scores.

Monitoring Both Models the Right Way

(FICO vs VantageScore model explained for tracking)

While monitoring matters, not all tools are equal.

Instead of annual reports, use a comprehensive platform.

Recommended Credit Monitoring

IdentityIQ provides:

All 3 bureaus

FICO & VantageScore access

Daily monitoring

Dark web alerts

$1,000,000 identity theft insurance

👉 Start your $1 trial (7-day trial) here:

https://www.identityiq.com/securepreferred.aspx?offercode=431295SH

How Masters Credit Consultants Improves FICO Outcomes

(FICO vs VantageScore model explained with expert support)

First, inaccurate data gets challenged properly.

Next, utilization strategies are applied carefully.

Then, account seasoning is managed intentionally.

Because lenders trust FICO, results matter.

Therefore, Masters Credit Consultants focuses there.

Additional Helpful Links

Masters Credit Consultants – Home

https://www.masterscredit.comYMA Financial – Business Consulting Services

https://www.ymafinancial.com

References

Consumer Financial Protection Bureau (credit scoring education)

Experian Credit Education Center

Equifax Knowledge Center

People Also Ask

What is better, FICO or VantageScore?

FICO is better for lending decisions.

Why is my VantageScore higher than my FICO?

Because weighting differs.

Do mortgage lenders use VantageScore?

No, they use older FICO models.

How fast can FICO scores improve?

With correct strategies, improvement can begin in 30–60 days.

Related Questions

Which FICO score version matters most?

How does utilization impact FICO vs VantageScore?

Can disputes hurt my score?

Why do lenders ignore free credit app scores?

Final Takeaway: FICO vs VantageScore Model Explained Simply

Ultimately, lenders trust FICO, not consumer apps.

Therefore, optimizing the right model is essential.

Because mistakes are costly, expert help matters.

Schedule Your Free Credit Consultation

Masters Credit Consultants is one of the best companies to assist with credit repair.

📞 Phone: 1-844-620-8796

🌐 Website: https://www.masterscredit.com

👉 Schedule Your Free Credit Consultation:

https://masterscreditconsultantsfreeconsultationbooknow.as.me/schedule/912546ad/appointment/31582691/calendar/6643355

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment