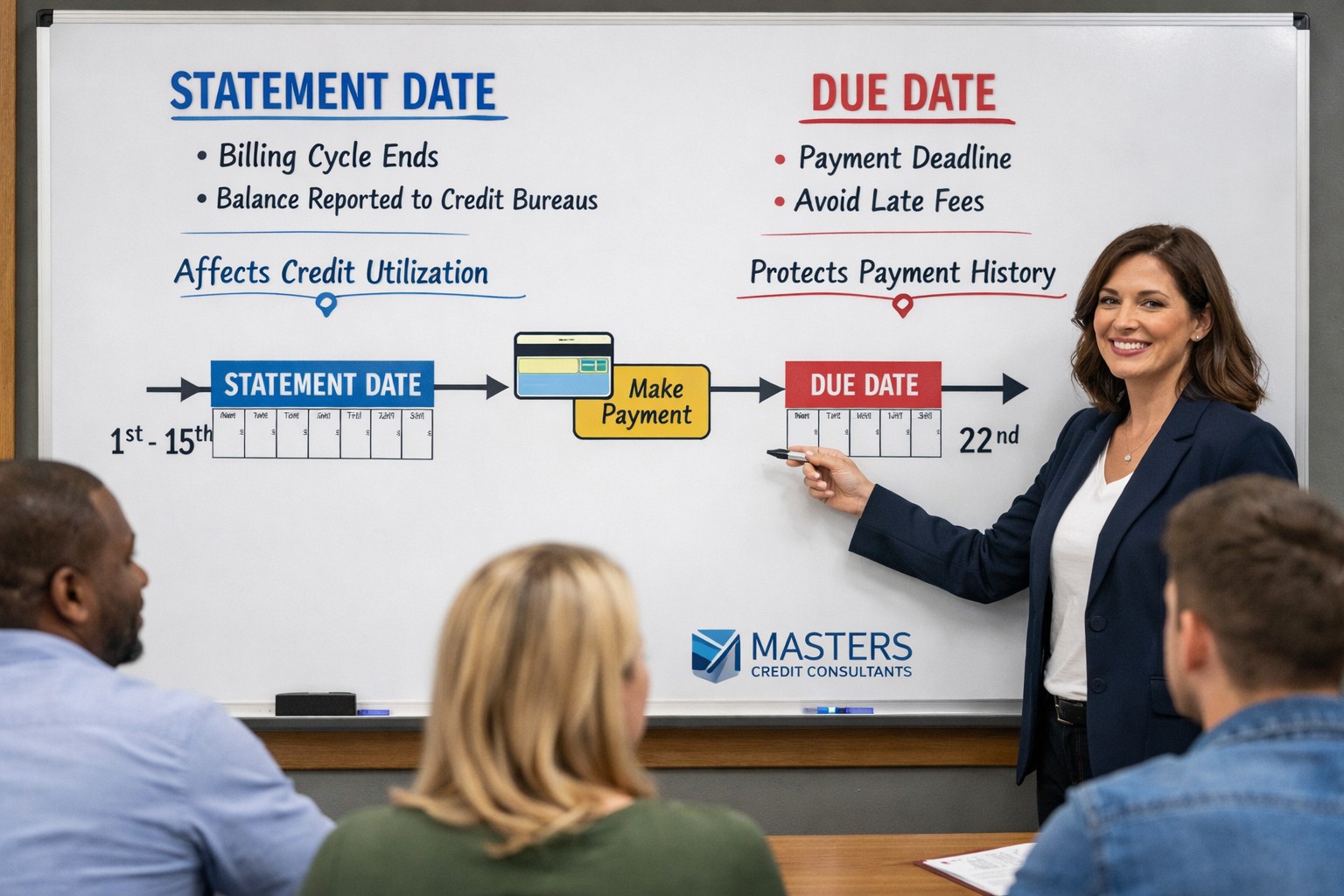

Due Date vs Statement Date: How Credit Card Timing Impacts Your Credit Score

Understanding due date vs statement date and how it impacts your credit can change your score faster than most people realize.

Your statement date determines what balance gets reported.

Your due date determines whether you pay interest or get a late mark.

Timing is everything.

In This Article You’ll Learn:

The real difference between statement date and due date

How reporting dates impact credit utilization

How to use payment timing to boost your credit score strategically

CLICK BELOW TO SCHEDULE NOW!!!

Table of Contents

What Is a Statement Date? (And Why It Matters for Your Credit Score)

The statement date is the day your billing cycle closes.

On that day, your credit card company calculates your balance. Then, it sends that balance to the credit bureaus.

⚠️ Critical Insight:

The balance reported on your statement date is what impacts your credit utilization ratio — not your due date balance.

Because credit utilization makes up a major portion of your credit score, the statement date directly affects your numbers.

Therefore, even if you pay in full before the due date, a high balance reported before the statement closes can still hurt your score temporarily.

What Is a Due Date? (And How It Protects Your Payment History)

The due date is the deadline to make at least your minimum payment.

If you miss the due date:

You may incur late fees

You may pay penalty interest

You risk a 30-day late mark

Since payment history accounts for 35% of your score, missing the due date can cause serious damage.

⚠️ Important Reminder:

Paying before the due date protects your payment history.

Paying before the statement date protects your utilization ratio.

They serve two completely different purposes.

How Due Date vs Statement Date Impacts Your Credit Score

Understanding due date vs statement date and how it impacts your credit allows you to control two major scoring factors:

1️⃣ Credit Utilization (30% of your score)

If your statement balance shows 80% utilization, your score drops.

Even if you pay it off days later, the damage is already reported.

2️⃣ Payment History (35% of your score)

If you pay after the due date, your lender may report you late.

That mark can stay on your credit report for up to seven years.

Therefore, knowing the difference gives you leverage.

Credit Utilization Strategy: The Timing Hack Most People Miss

Here’s the advanced strategy professionals use:

✔ Pay your balance down before the statement date

⚠️ Advanced Tip: Do not use your credit card between your due date and your statement date. You can use the card again after the statement date. This will prevent accidentally increasing your credit utilization ratio after the due date, but before the statement closes and the lender reports the data to the credit bureaus.

✔ Keep reported utilization under 30% (ideally under 10%)

✔ Then pay remaining balance before the due date

This two-step method ensures:

Low reported balance

No interest

No late payments

As a result, your score stays optimized month after month.

Common Mistakes With Due Date vs Statement Date

Many people believe paying before the due date is enough.

However, that assumption often costs points.

Common mistakes include:

Paying in full only on the due date

Maxing out cards mid-cycle

Ignoring statement closing dates

Making one large payment instead of strategic timing

Because lenders report based on statement cycles, misunderstanding this timing leads to unnecessary score drops.

The Best Strategy to Maximize Your Credit Score Fast

To optimize your score consistently:

Learn each card’s statement closing date

Pay balances down 3–5 days before that date

Keep utilization below 10%

Automate minimum payments before the due date

Additionally, monitor your credit reports monthly.

For accurate three-bureau monitoring, consider IdentityIQ (7-day trial):

https://www.identityiq.com/securepreferred.aspx?offercode=431295SH

IdentityIQ provides:

Experian, Equifax, and TransUnion reports

Score updates every 30 days

3-bureau daily monitoring

$1,000,000 identity theft insurance

Because consistent credit report access enables timely disputes, monitoring is essential.

When Should You Get Professional Help?

If your credit score is stuck despite paying on time, the issue may be:

High reported utilization

Outdated reporting

Inaccurate balances

Late payments reporting incorrectly

In that case, working with professionals can accelerate results.

Masters Credit Consultants is one of the best companies assisting clients with credit repair, utilization strategy, and reporting optimization.

Additional Helpful Tips

To strengthen your credit education journey, read:

How to Stop Collection Calls in South Carolina Immediately

https://www.masterscredit.com/2026/02/15/how-to-stop-collection-calls-in-south-carolina/Denied Credit? Now What? We Have Answers!!!

https://www.masterscredit.com/2026/02/15/denied-credit-now-what-we-have-answers/Why Is My Personal Credit Hurting My Business Credit Approvals?

(www.masterscredit.com)

For business credit guidance, explore:

https://www.ymafinancial.com

People Also Ask

Does paying before the statement date increase credit score?

Yes. Paying before the statement date lowers reported utilization, which can increase your score.

Is it better to pay on statement date or due date?

It is better to pay before the statement date for utilization and before the due date for payment history protection.

Why did my credit score drop even though I paid on time?

Your reported balance may have been high on the statement date.

Can I change my statement date?

Some lenders allow billing cycle adjustments upon request.

Related Questions

How much does credit utilization impact my score?

Should I pay my credit card twice a month?

What balance should I leave on my card?

Does zero balance hurt my credit score?

Schedule Your Free Credit Consultation

If you are unsure how to strategically manage your due date vs statement date timing, let professionals guide you.

📞 Phone: 1-844-620-8796

🌐 Website: www.masterscredit.com

👉 Schedule Your Free Credit Consultation:

https://masterscreditconsultantsfreeconsultationbooknow.as.me/schedule/912546ad/appointment/31582691/calendar/6643355

Masters Credit Consultants is one of the best companies helping clients improve credit scores, remove inaccurate reporting, and build long-term credit strength.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment