Why Isn’t My Credit Score Improving? Here’s What to Do

The reason your credit score isn’t improving isn’t that you aren’t paying your bills on time. This article will look at factors like not adding new types of debt to your account, keeping your credit utilization ratio under 30%, and more. These are all very important factors, and they can significantly impact your score. So, how do you improve your credit score?

We have a new location: Credit repair Norfolk VA is now open!

Having a long credit history.

Having a long credit history is important in determining your credit score. Lenders view your payment history, not the number of accounts you have when determining your score. It also helps to maintain a low credit utilization ratio. However, while having a long history will increase your credit score, it isn’t enough to offset negative information. Instead, it is crucial to pay off your old accounts on time.

Review your bank statements and check for any irregular payments.

Identifying all of your creditors is a great way to increase your chances of paying your bills on time. Make a list of your creditors and recurring obligations, such as utility bills, gym memberships, and media subscriptions. Review your bank statements and check for any irregular payments. Many creditors allow you to make changes to the due date. If this is impossible, a few other methods will help you meet the deadlines.

Having a long credit history.

Having a long credit history is important in determining your credit score. Lenders view your payment history, not the number of accounts you have when determining your score. It also helps to maintain a low credit utilization ratio. However, while having a long history will increase your credit score, it isn’t enough to offset negative information. Instead, it is crucial to pay off your old accounts on time.

Try to avoid closing new accounts.

The longer your credit history is, the better. You should avoid closing new accounts to avoid damaging your credit score. You also want to avoid making a payment on a debt that has been “charged off” by the creditor, as this is a negative mark on your credit report. It is because the collection agency is likely to reactivate the debt. If this is the occurrence, you should pay off your credit card to a lower percentage of its credit limit.

Adding a trusted user to a credit card.

Adding a trusted user to a credit card will lengthen your credit history and improve your credit score. However, You should avoid this method since it is considered fraud if you apply for financing after transferring the authorized user status to another individual. You should also avoid piggybacking on someone else’s credit card. Some companies rent the authorized user status to someone else, so beware.

Adding new types of debt.

Adding new types of debt to your credit report will harm your credit score. Fortunately, most of these types of debt do not get marked as charge-offs until four to six months after they are due. As a result, paying off your charge-offs is not enough to eliminate the mark on your report. Charge-offs can stay on your report for seven years!

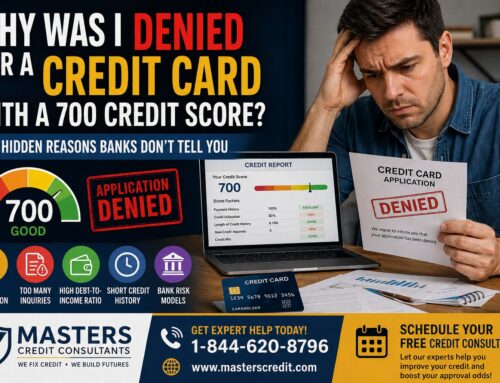

The credit utilization ratio is a simple formula to understand.

Add up all of your outstanding balances on your credit cards and divide that total by the amount of available credit. Multiply the result by 100 to get the percentage of your credit that you are using. This procedure will help you understand why you do not see any improvement in your score. And remember, it’s never too late to change the numbers on your credit report.

Take action now! Fix your credit to get the houses, cars, apartments, or credit cards you truly deserve. Level up your credit and level up your life! Contact us today for easy and fast credit repair. Masters Credit Consultants is here to help you now.

[wpi_designer_button slide_id=6350]

Our Most Popular Articles:

How Long Does an Eviction stay on Your Record?

What Is A 609 Dispute Letter And Does It Work?

How to Remove Late Payments from your Credit Report

Pay for Delete Letter Template for Credit Repair

How Long Do Late Payments Stay On Your Credit Report?

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment