When it comes to financial health, few things have as significant an impact as your credit score. Your credit score is a crucial factor that lenders, landlords, and even potential employers consider when making decisions about you. It’s a three-digit number that represents your creditworthiness and reflects your ability to manage debt responsibly.

If you find yourself with a 500 credit score, it’s essential to understand that you’re facing a challenging situation. A credit score of 500 is considered poor, and it indicates that you have a history of missed payments, high credit utilization, or even bankruptcy. But don’t lose hope just yet—there are steps you can take to improve your credit score and get back on track financially.

Understanding the Factors Impacting Your Credit Score

Before diving into the strategies to improve your credit score, let’s first explore the factors that contribute to its calculation. Your credit score is based on several key elements:

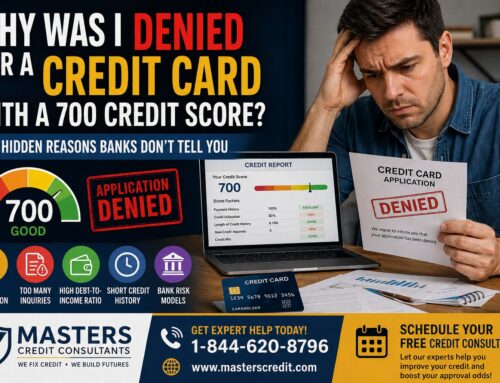

- Payment History: This is the most critical factor and accounts for approximately 35% of your credit score. Late payments, defaulted accounts, and bankruptcies can significantly impact your score in a negative way.

- Credit Utilization: This refers to the percentage of your available credit that you’re currently using. High credit utilization ratios suggest a higher risk to lenders and can lower your credit score.

- Credit History Length: The length of your credit history matters. Having a longer credit history allows lenders to assess your creditworthiness more accurately.

- New Credit Applications: Applying for multiple new lines of credit within a short period can negatively impact your credit score, as it may suggest financial instability.

- Credit Mix: Lenders like to see a mix of different types of credit, such as credit cards, loans, and mortgages. A diverse credit portfolio can demonstrate responsible credit management.

Now that we have a better understanding of what factors influence your credit score, let’s move on to the steps you can take to improve it.

Review Your Credit Reports

The first step in the credit score improvement process is to review your credit reports from all three major credit bureaus: Experian, Equifax, and TransUnion. Carefully examine each report for errors, inaccuracies, or fraudulent accounts. If you find any discrepancies, promptly dispute them with the credit bureaus to have them corrected or removed.

Create a Budget and Stick to It

Improving your credit score requires disciplined financial habits. Start by creating a realistic budget that takes into account your income, expenses, and debt obligations. This will help you gain a clear understanding of your financial situation and enable you to make better decisions with your money. Be sure to allocate funds to pay down existing debt and avoid accumulating new debt.

Pay Your Bills on Time

Since payment history is a significant factor in calculating your credit score, it’s crucial to make all your future payments on time. Late payments can have a severe negative impact on your creditworthiness. Set up payment reminders or automatic payments to avoid missing due dates. Over time, consistent on-time payments will help rebuild your credit history.

Reduce Credit Card Balances

High credit card balances can weigh down your credit score, especially if you’re utilizing a significant portion of your available credit. Aim to keep your credit utilization ratio below 30%. If possible, pay off your credit card balances in full each month to minimize interest charges and improve your credit utilization ratio.

Consider Debt Consolidation or Negotiation

If you’re struggling with multiple debts, it might be worth exploring options like debt consolidation or negotiation. Debt consolidation involves combining multiple debts into a single loan with a lower interest rate, making it easier to manage. Debt negotiation, on the other hand, involves working with creditors to settle your debts for less than the full amount owed. Both approaches can help you regain control of your finances and improve your credit score over time.

Build Positive Credit History

Building a positive credit history is essential for improving your credit score. If you’re unable to qualify for traditional credit cards or loans due to your low credit score, consider alternative options like secured credit cards or credit-builder loans. These tools can help you demonstrate responsible credit usage and gradually rebuild your creditworthiness.

Seek Professional Help

Improving your credit score can be a complex and challenging process, especially if you’re dealing with significant financial difficulties. In such cases, it may be beneficial to seek the assistance of credit counseling agencies or financial professionals who specialize in credit repair. They can provide personalized guidance, help you develop a tailored action plan, and negotiate with creditors on your behalf.

In conclusion, while a 500 credit score may seem daunting, it’s important to remember that it’s not the end of the road. By implementing the strategies mentioned above and adopting responsible financial habits, you can begin to rebuild your credit and improve your overall financial well-being. It may take time and patience, but with perseverance and determination, you can come back from a 500 credit score and pave the way for a brighter financial future.

At Masters Credit Consultants, we offer a no-obligation, free credit consultation session to residents nationwide. During this session, we will discuss your credit situation and provide you with recommendations on how to improve your score. We will also give you an overview of our services and pricing options.

If you’re struggling with a low credit score, don’t despair. With the right strategies and partners, you can improve your score and take control of your financial future. Masters Credit Consultants can help you achieve your credit goals and provide you with ongoing support to maintain a strong credit score. Contact us today to schedule your free credit consultation.

[wpi_designer_button slide_id=6350]

Note: The information on this website is for general purposes only and does not constitute financial or legal advice.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment