Clearing Up the Confusion: How Long Does a Repo Stay on Your Credit Report?

If you’ve ever faced the unfortunate prospect of having your car repossessed, you’re probably familiar with the impact it can have on your credit score. But just how long will this negative mark stay on your credit report? It’s a common question, and one that can cause a lot of confusion. The truth is, the answer depends on a few different factors, and there’s no one-size-fits-all response.

However, understanding the basics of how credit reporting works can help you get a sense of what to expect. In this article, we’ll dive into the details of how long a repo stays on your credit report, and what you can do to start rebuilding your credit in the meantime. Whether you’re recovering from a recent repossession or just curious about the impact it could have on your financial future, read on to clear up the confusion.

What is a Repo and How Does it Affect Your Credit Score?

Before we dive into how long a repo stays on your credit report, let’s first define what a repo is and how it affects your credit score. A repo, short for repossession, occurs when you default on a loan for a vehicle, and the lender takes possession of the vehicle. This can happen for a variety of reasons, including missed payments or defaulting on the loan entirely. Once the vehicle has been repossessed, the lender may sell it to recover their losses.

A repo has a significant impact on your credit score because it is a clear sign that you were unable to fulfill your financial obligations. The lender reports the repossession to the credit bureaus, which then lowers your credit score. The exact amount that your credit score drops will depend on a variety of factors, including your overall credit history and how many other negative marks you have on your credit report.

It’s worth noting that not all repossessions are created equal. For example, if you voluntarily surrender your vehicle rather than having it repossessed, it may have less of a negative impact on your credit score. However, this will depend on the specific circumstances of your situation.

How Long Does a Repo Stay on Your Credit Report?

Now, let’s get to the heart of the matter. How long does a repo stay on your credit report? The answer to this question is not straightforward. In general, a repossession will stay on your credit report for seven years from the date it was first reported. This means that for seven years, lenders will be able to see that you had a repossession on your record, which can impact your ability to get approved for loans or credit cards.

However, there are a few things to keep in mind. First, the impact of a repo on your credit score will lessen over time. While it will still be visible on your credit report, its impact will be less significant the further in the past it is. Additionally, if you are able to rebuild your credit and establish a positive credit history, the impact of the repo will be less severe.

Another thing to keep in mind is that the exact length of time that a repo stays on your credit report can vary depending on where you live. Some states have their own laws regarding credit reporting, which can impact how long negative marks like repossessions stay on your report.

What Happens After a Repo is Reported on Your Credit Report?

Once a repo has been reported on your credit report, there’s not much you can do to remove it. It will stay on your report for the duration of the seven-year period, regardless of whether you pay off the remaining balance of the loan or not. However, there are a few things you can do to start rebuilding your credit in the meantime.

One of the most important things you can do is to establish a positive credit history. This means making on-time payments on any other loans or credit cards you have, and keeping your credit utilization low. It may also be helpful to open a secured credit card or take out a small personal loan, both of which can help establish a positive payment history.

Another thing to keep in mind is that you can still negotiate with your lender even after a repo has been reported on your credit report. For example, you may be able to work out a payment plan or settle the remaining balance of the loan for less than what you owe. While this won’t remove the repo from your credit report, it can help minimize the impact it has on your credit score.

How to Remove a Repo from Your Credit Report

As mentioned earlier, there’s not much you can do to remove a repo from your credit report. However, there are a few instances where it may be possible to have it removed. For example, if the repo was reported in error, you can dispute it with the credit bureaus and have it removed from your report.

Additionally, if the lender did not follow proper procedures when repossessing your vehicle, you may be able to have the repo removed. For example, if the lender did not provide you with proper notice before repossessing the vehicle, you may be able to have the repo removed from your report.

However, these instances are relatively rare. In most cases, you will need to wait out the seven-year period before the repo is removed from your credit report.

Tips for Rebuilding Your Credit After a Repo

While a repo can have a significant impact on your credit score, it’s not the end of the world. There are a few things you can do to start rebuilding your credit in the aftermath of a repossession.

First, as mentioned earlier, it’s important to establish a positive credit history. This means making on-time payments on any loans or credit cards you have, and keeping your credit utilization low. It may also be helpful to open a secured credit card or take out a small personal loan to help establish a positive payment history.

Another important factor to consider is your debt-to-income ratio. This is the amount of debt you have compared to your overall income. If you have a high debt-to-income ratio, it can be difficult to get approved for new loans or credit cards. To improve your debt-to-income ratio, consider paying down any debts you have and avoiding taking on new debt whenever possible.

Finally, it’s important to monitor your credit report regularly. This will help you keep track of any negative marks on your report, including the repo. It can also help you identify any errors or fraudulent activity on your report, which can be disputed with the credit bureaus.

Common Misconceptions About Repos and Credit Reports

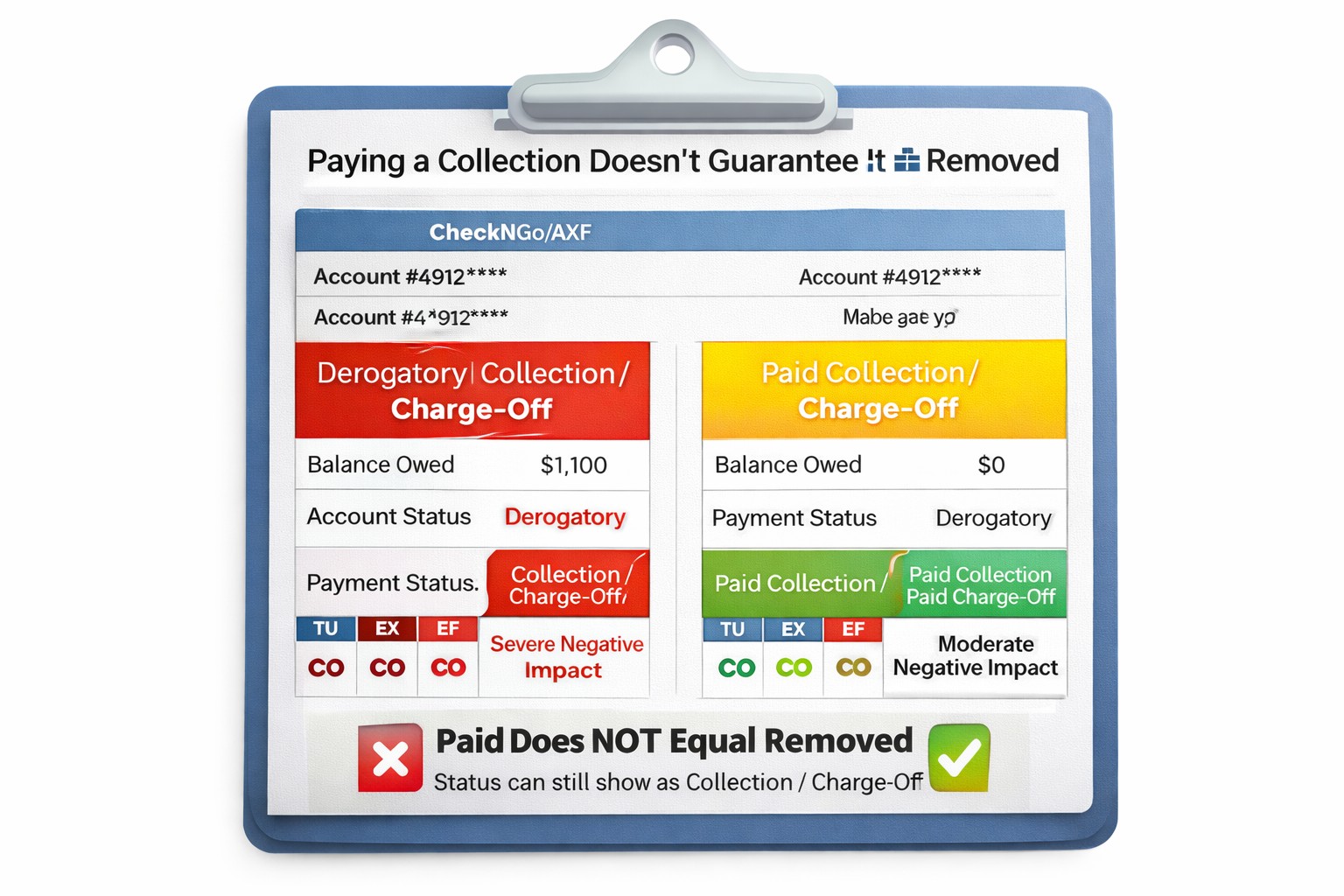

There are a few common misconceptions about repos and credit reports that are worth addressing. One of the most common is the idea that paying off the remaining balance of the loan will remove the repo from your credit report. Unfortunately, this is not the case. While paying off the loan can help minimize the impact of the repo on your credit score, it will still remain on your report for the seven-year period.

Another misconception is that you can hide a repo from potential lenders. This is not true, as the repo will be visible on your credit report for the duration of the seven-year period. It’s better to be upfront about the repo with potential lenders, as they will likely find out about it anyway.

When to Consider Bankruptcy Instead of Repossession

In some cases, repossession may not be the best option for dealing with a defaulted car loan. Depending on your financial situation, bankruptcy may be a better option. Filing for bankruptcy can help eliminate certain types of debt, including car loans. However, it’s important to keep in mind that bankruptcy will have a significant impact on your credit score and should only be considered as a last resort.

How to Avoid Repossession in the First Place

Of course, the best way to deal with a repo is to avoid it in the first place. There are a few steps you can take to minimize the risk of having your vehicle repossessed. First, make sure you can afford the loan payments before taking out the loan. This means considering all of your other expenses and ensuring that you have enough income to cover the loan payments.

It’s also important to communicate with your lender if you’re having trouble making payments. In some cases, the lender may be willing to work out a payment plan or other arrangement to help you avoid repossession.

Seeking Professional Help for Credit Issues

If you’re struggling with debt or credit issues, it may be helpful to seek professional help. There are a variety of organizations and services that can help you manage your debt and improve your credit score. For example, credit counseling services can help you create a budget and develop a plan to pay off your debts. Additionally, debt consolidation services can help you combine multiple debts into a single payment with a lower interest rate.

In conclusion, a repo can have a significant impact on your credit score and financial future. While there’s no way to remove a repo from your credit report before the seven-year period is up, there are a few things you can do to start rebuilding your credit in the meantime. Establishing a positive credit history, paying down debt, and monitoring your credit report regularly can all help minimize the impact of a repo on your credit score. If you’re struggling with debt or credit issues, consider seeking professional help to develop a plan for managing your finances.

Ready to take control of your financial future?

Call Masters Credit today at 1-844-620-8796 and let us propel your credit score to new heights!

1-844-620-8796

Don’t miss out on our free online credit evaluation – discover the key to unlocking better opportunities and achieving your financial goals. Take the first step towards a brighter tomorrow by taking our evaluation now!

Take our free online credit evaluation today!

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment