Understanding the Difference Between Credit Card Annual APR and Interest Rate

When people hear about credit card APR vs. interest rate, they often assume they’re the same thing. However, understanding the difference between credit card Annual Percentage Rate (APR) and interest rate is crucial for anyone trying to manage debt wisely or improve their credit. These two terms directly affect how much you pay to borrow money — and misunderstanding them can cost you hundreds in unnecessary fees or interest.

In this guide, Masters Credit Consultants explains in detail how credit card APR and interest rate differ, why each matters, and how to use this knowledge to protect your financial health.

What Is a Credit Card Interest Rate?

Your credit card interest rate is the cost of borrowing money expressed as a percentage. It’s the rate charged on your unpaid balance if you carry a balance from month to month.

For example, if your card has a 20% interest rate and you owe $1,000, you’ll be charged approximately $200 per year in interest (if the balance remains unpaid).

However, it’s important to know that interest rates can vary based on:

Your credit score

The type of transaction (purchases, balance transfers, cash advances)

Market conditions and your lender’s risk policies

The interest rate is the foundation of how your credit card company calculates your APR — but the APR itself includes more than just the rate.

What Is Credit Card APR and How Is It Different?

The credit card Annual Percentage Rate (APR) represents the total cost of borrowing money over a year — including both the interest rate and additional fees such as finance charges or annual fees.

In simple terms, the APR gives you the full picture of how expensive a credit card really is.

Here’s a breakdown:

Interest Rate: The base cost of borrowing money.

APR: The total annualized cost including interest and certain fees.

For instance, if two credit cards have a 20% interest rate, but one has a $50 annual fee, its APR will be higher than the one without a fee.

This makes APR a better comparison tool when evaluating multiple credit cards.

Understanding APR in Detail — Formula, Calculation, and Real-Life Examples

The Annual Percentage Rate (APR) represents the true yearly cost of borrowing money, including the interest rate and certain fees tied to the credit card. Understanding how APR works — and how it affects your balance — helps you avoid costly surprises and plan smarter repayment strategies.

Let’s break it down with some real-world examples 👇

Example 1: Standard Purchase APR

Imagine you have a credit card with a 20% APR and a balance of $1,000 that you don’t pay off for 12 months.

Interest charged over the year ≈ $200

Total owed after one year ≈ $1,200

This means your Annual Percentage Rate (APR) determines how much extra you’ll pay for carrying a balance — the higher the APR, the more interest you’ll owe.

✅ Key takeaway: Always try to pay your balance in full each month to avoid paying interest at all.

Example 2: Introductory APR vs. Standard APR

Many credit cards offer introductory APRs, such as 0% APR for 12 months on purchases or balance transfers.

Let’s say you make a $2,000 purchase on a card offering 0% APR for 12 months.

If you pay $167 per month for 12 months, you’ll pay off the balance before interest begins.

But if you still owe $500 after the promo period, and the regular APR rises to 22%, interest starts applying to that $500 immediately.

✅ Key takeaway: Promotional APRs can save you money — but only if you pay off your balance before the introductory period ends.

Example 3: Cash Advance APR

Cash advances are among the most expensive forms of credit.

Suppose you withdraw $300 from your credit card, and your cash advance APR is 28%, with a 3% cash advance fee.

Immediate fee: $9

Annualized interest: $84 (if unpaid for 12 months)

Total cost ≈ $393

✅ Key takeaway: Cash advances should be avoided unless absolutely necessary, as they come with higher APRs and no grace period.

Example 4: Penalty APR After a Missed Payment

If you miss a payment or violate card terms, many lenders impose a penalty APR, often around 29.99%.

If your regular balance is $2,000 and you miss one payment, your new balance can grow by hundreds in just a few months.

✅ Key takeaway: Always pay at least the minimum payment on time to avoid triggering a penalty APR.

Example 5: Comparing APRs Across Two Credit Cards

| Card Type | Interest Rate | Annual Fee | APR | Notes |

|---|---|---|---|---|

| Card A | 18% | $0 | 18% APR | No extra fees, lower borrowing cost |

| Card B | 18% | $75 | 21% APR | Annual fee increases total borrowing cost |

Even though both cards have the same interest rate, Card B’s APR is higher because of its annual fee — showing that APR is a more accurate measure of a card’s true cost.

✅ Key takeaway: Always compare APRs, not just interest rates, when shopping for a new card.

How to Calculate Credit Card APR — Step-by-Step

Although most credit card companies disclose APR upfront, it’s helpful to know how it’s calculated manually.

Here’s a simple step-by-step example:

Example 1: Basic APR Calculation

Let’s say:

Your card’s interest rate is 20% annual.

You borrowed $1,000 and carried that balance for one year.

You paid an annual fee of $50.

1: Calculate the total cost of borrowing.

$1,000 × 20% = $200 interest

$50 annual fee = $250 total cost

2: Divide the total cost by the loan amount.

$250 ÷ $1,000 = 0.25

3: Multiply by 100 to get the APR.

0.25 × 100 = 25% APR

✅ Result: Your true cost of borrowing is 25% APR, not 20%, once the fee is included.

Example 2: APR for a Short-Term Balance

Imagine you borrow $2,000 on a credit card for 6 months and pay $120 in interest and $20 in fees.

A: Add total cost of borrowing.

$120 + $20 = $140

B: Divide by the loan amount.

$140 ÷ $2,000 = 0.07

C: Annualize for a full year (multiply by 2, since 6 months = half a year).

0.07 × 2 = 0.14

D: Multiply by 100 to get the APR.

0.14 × 100 = 14% APR

✅ Result: The effective APR on that 6-month loan is 14%.

How Daily or Monthly APR Is Calculated

Credit card companies apply daily periodic rates to calculate interest.

Formula:

Daily Periodic Rate = APR ÷ 365

Example:

If your card APR is 21.9%, then:

21.9 ÷ 365 = 0.06% daily interest

If your average daily balance is $1,000, you’ll pay:

$1,000 × 0.0006 × 30 days = $18 per month in interest.

✅ Key takeaway: Even small differences in APR can add up significantly over time, especially if you carry balances from month to month.

How Masters Credit Consultants Helps You Lower APR

High APRs are often caused by poor credit scores or negative marks on your credit report.

Masters Credit Consultants specializes in:

Removing inaccurate or outdated accounts

Disputing unverifiable negative items

Coaching clients to rebuild credit strategically

When your credit improves, lenders trust you more — which means lower APRs, better loan offers, and higher approval limits.

Types of Credit Card APRs You Should Know

Not all APRs are created equal. Knowing which type you’re dealing with can save you from unexpected costs:

Purchase APR: The rate applied to regular purchases.

Cash Advance APR: Usually higher, applies to cash withdrawals from your credit card.

Balance Transfer APR: The rate charged when moving debt from one card to another.

Penalty APR: A higher rate applied after a missed payment or violation of terms.

Introductory APR: A temporary promotional rate, often 0%, used to attract new customers.

When your introductory APR expires, your rate may jump to the standard purchase APR, so always read the fine print carefully.

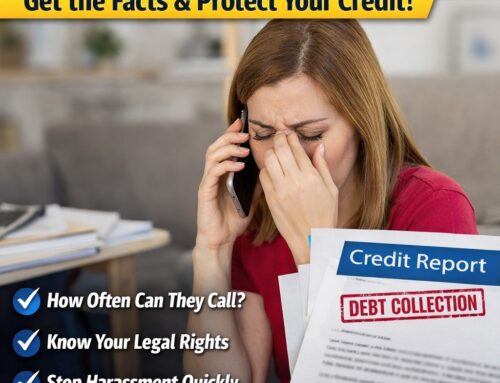

How APR and Interest Rate Affect Your Credit Score

The difference between credit card APR and interest rate can impact your financial behavior and, in turn, your credit score. High-interest or high-APR cards make it harder to pay off balances, which can increase your credit utilization ratio — a key factor in your credit score.

To maintain a strong credit profile, Masters Credit Consultants recommends:

Paying more than the minimum balance each month.

Avoiding cash advances due to their high APRs.

Keeping utilization below 30%.

Monitoring your credit with a trusted service like IdentityIQ for 3-bureau reports, dark web alerts, and $1M identity theft insurance.

Why Knowing the Difference Between APR and Interest Rate Matters

Understanding the difference between APR and interest rate empowers you to make smarter financial decisions. Here’s why:

Better Comparison: When comparing cards, APR gives a more accurate cost overview.

Avoiding Surprises: Interest rate may seem low, but a high APR can hide fees.

Debt Management: Knowing your APR helps plan payoff strategies effectively.

When you’re rebuilding or improving credit, these insights can help you minimize debt costs and improve your financial stability.

How to Lower Your Credit Card APR or Interest Rate

If your APR feels too high, here are actionable steps to reduce it:

Negotiate with your issuer: Many banks will reduce your rate if you have a good payment history.

Transfer balances: Use cards offering 0% APR on balance transfers to reduce interest costs.

Improve your credit: A higher credit score leads to better rate offers.

Seek expert help: Work with professionals like Masters Credit Consultants, who specialize in improving credit reports and guiding clients toward better financial products.

Masters Credit Consultants Can Help You Manage High APRs

High APRs often reflect a history of credit issues. Masters Credit Consultants helps clients remove inaccurate items, repair credit, and strategically rebuild creditworthiness — giving you the leverage to qualify for lower interest rates in the future.

They also guide clients through:

Understanding credit utilization

Rebuilding credit with secured cards

Correcting credit report errors with major bureaus

Learn more at MastersCredit.com.

Additional Information:

On www.masterscredit.com:

Credit Repair Services: https://www.masterscredit.com/credit-repair-services/

Denied for Credit and Don’t Know Why? https://www.masterscredit.com/denied-for-credit-and-dont-know-why/

Free Credit Consultation: https://www.masterscredit.com/sign-up/

How to Build Business Credit Quickly: https://www.masterscredit.com/how-to-build-business-credit-quickly/

On www.ymafinancial.com:

Business Startup Funding: https://www.ymafinancial.com/business-startup-funding/

Business Consulting Services: https://www.ymafinancial.com/business-consulting-services/

Building Business Credit with YMA Financial: https://www.ymafinancial.com/building-business-credit/

Final Thoughts on Credit Card APR vs. Interest Rate

The difference between credit card APR and interest rate may seem small, but it’s one of the most important details in personal finance. Understanding both terms allows you to compare cards accurately, avoid high fees, and make smarter credit decisions.

If your credit report or score is holding you back from getting better rates, Masters Credit Consultants can help.

📞 Contact Masters Credit Consultants Today

Masters Credit Consultants specializes in professional credit repair, score improvement, and personalized financial education.

📞 Phone: 1-844-620-8796

🌐 Website: www.masterscredit.com

💬 Schedule Your Free Credit Consultation:

Book Your Appointment Here

Take control of your credit and your financial future — start today!

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment