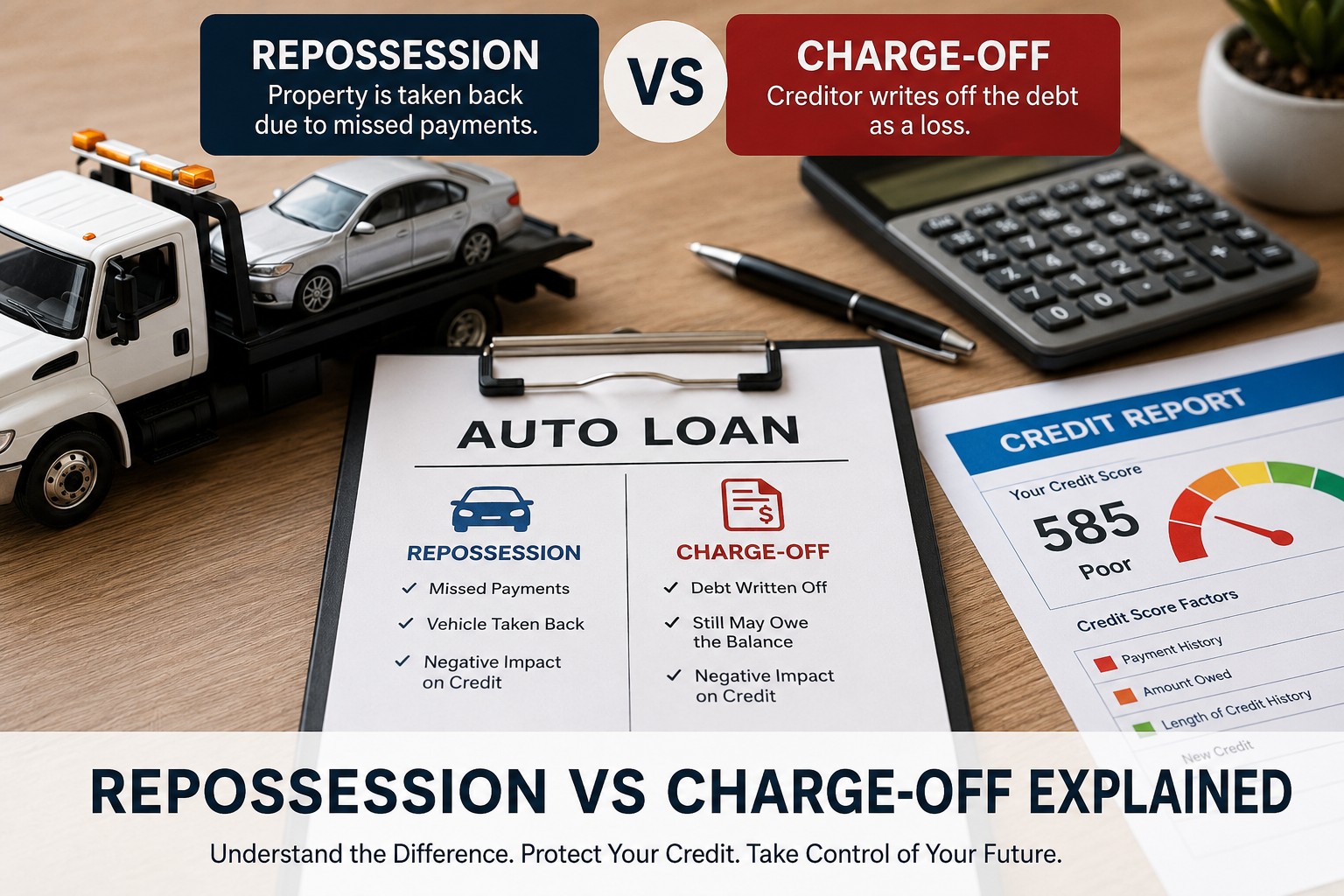

Repossession vs Charge-Off Explained: What Hurts Your Credit More?

A repossession happens when a lender takes back property, such as a vehicle, after missed payments. A charge-off happens when a creditor writes a debt off as a loss after long-term delinquency.

However, both can seriously hurt your credit score, reduce approval odds, and remain on your credit report for years.

🔹 Quick Answer:

A repossession involves losing secured property after missed payments, while a charge-off means the lender closed the account as a financial loss. Both negatively affect your credit report and may lead to collections or lawsuits.

In This Article You’ll Learn

✔ The difference between repossession and charge-off

✔ Which one hurts your credit more

✔ How lenders report these accounts

✔ How to rebuild credit after negative reporting

✔ What steps may help remove inaccurate information

Table of Contents

- Repossession vs Charge-Off Explained

- What Is a Repossession?

- What Is a Charge-Off?

- Major Differences Between Repossession and Charge-Off

- Which Hurts Your Credit More?

- Can a Repossession Become a Charge-Off?

- How Long Do They Stay on Your Credit Report?

- How to Start Rebuilding Your Credit

- Why Clients Choose Masters Credit Consultants

- People Also Ask

What Is a Repossession?

A repossession happens when a borrower falls behind on payments for a secured loan, most commonly an auto loan.

Because the lender owns a security interest in the vehicle, the lender may legally take the vehicle back after default.

For example:

- Missed payments accumulate

- The loan becomes delinquent

- The lender sends default notices

- A repossession company retrieves the vehicle

Afterward, the lender may auction the vehicle. However, if the sale does not cover the remaining balance, the borrower may still owe money.

This remaining amount is called a deficiency balance.

Common Effects of Repossession

| Repossession Impact | Effect on Credit |

|---|---|

| Late Payments | Score drops significantly |

| Vehicle Loss | Transportation hardship |

| Deficiency Balance | Remaining debt still owed |

| Collection Activity | Additional negative reporting |

| Credit Score Damage | May remain for 7 years |

⚠️ Important:

Many consumers believe repossession erases the debt entirely. However, lenders may still pursue the remaining balance after selling the vehicle.

What Is a Charge-Off?

A charge-off happens when a creditor closes an unpaid account and reports it as a financial loss.

Usually, creditors charge off accounts after 120–180 days of missed payments.

However, a charge-off does not mean the debt disappears.

Instead:

- The creditor may continue collecting

- The account may transfer to collections

- Interest and fees may continue

- Lawsuits may still occur

Charge-offs commonly appear on:

- Credit cards

- Personal loans

- Auto loans

- Retail financing accounts

- Installment loans

Common Effects of a Charge-Off

| Charge-Off Impact | Effect on Credit |

|---|---|

| Severe Delinquency | Major score reduction |

| Closed Account | Reduced credit profile strength |

| Collection Transfer | Additional negative account |

| High Utilization | Credit ratio damage |

| Long-Term Reporting | Up to 7 years |

Repossession vs Charge-Off: Major Differences

Although both hurt credit, they represent different financial events.

| Repossession | Charge-Off |

|---|---|

| Property is taken back | Debt is written off |

| Usually secured loans | Can be secured or unsecured |

| Common with auto loans | Common with credit cards |

| Physical asset involved | Accounting status involved |

| May create deficiency balance | Balance may still be collectible |

📌 Note:

The biggest misunderstanding about repossession vs charge-off is that consumers believe one replaces the other. In reality, the same account may contain BOTH negative statuses.

Which Hurts Your Credit More?

Both are damaging. However, the worst situation usually occurs when both appear together.

For example:

A repossession may include:

- 30-day late payments

- 60-day late payments

- 90-day late payments

- Repossession status

- Deficiency balance

- Collection account

- Charge-off notation

As a result, one loan can create multiple negative reporting events simultaneously.

Therefore, the overall damage depends on:

- Total debt amount

- Recent reporting activity

- Number of delinquent accounts

- Credit utilization

- Collection activity

- Overall credit history

Can a Repossession Become a Charge-Off?

Yes.

This happens frequently with auto loans.

Here’s how it usually works:

| Step | What Happens |

|---|---|

| 1 | Payments are missed |

| 2 | Vehicle gets repossessed |

| 3 | Vehicle is sold at auction |

| 4 | Remaining balance still owed |

| 5 | Balance becomes delinquent |

| 6 | Lender charges off the remaining debt |

Therefore, repossession and charge-off may appear together on the same tradeline.

🚨 Important Consumer Warning:

Some consumers attempt illegal “credit sweep” methods after repossession or charge-off accounts appear. However, false identity theft claims or fraudulent disputes may create serious legal and lending problems later.

How Long Do Repossessions and Charge-Offs Stay on Credit Reports?

In most cases, repossessions and charge-offs may remain on a credit report for up to 7 years from the original delinquency date.

However, reporting accuracy matters.

Consumers should review:

- Balance accuracy

- Reporting dates

- Duplicate collections

- Account status

- Monthly reporting history

- Re-aging violations

If inaccurate reporting exists, disputes may be appropriate.

For updated 3-bureau monitoring, Masters Credit Consultants recommends IdentityIQ with the $1 trial (7-day trial):

https://www.identityiq.com/securepreferred.aspx?offercode=431295SH

IdentityIQ includes:

✔ Experian, Equifax & TransUnion reports

✔ Credit score monitoring

✔ Daily alerts

✔ Dark web monitoring

✔ $1,000,000 identity theft insurance

How to Start Rebuilding Credit After Repossession or Charge-Off

The first step is reviewing your full credit profile carefully.

Then focus on rebuilding positive history consistently.

Step 1 — Review All Three Credit Reports

Check:

- Experian

- Equifax

- TransUnion

Look for inconsistencies between bureaus.

Step 2 — Identify Reporting Errors

Common issues include:

- Wrong balances

- Duplicate collections

- Incorrect dates

- Missing dispute notations

- Inaccurate payment history

- Incorrect account status

Step 3 — Build Positive Credit History

Focus on:

- On-time payments

- Lower utilization

- Secured credit cards

- Credit-builder accounts

- Stable account history

Step 4 — Work With a Professional Credit Repair Company

If you’re struggling with negative items on your report, a professional credit repair company can help dispute inaccurate information and rebuild your credit profile.

Masters Credit Consultants reviews:

- Repossessions

- Charge-offs

- Collections

- Late payments

- Inquiries

- Credit utilization issues

Why Clients Choose Masters Credit Consultants

With a 5.0-star rating across 80+ verified reviews, our clients consistently trust us to deliver real results and guidance they can rely on.

Many clients see results in 60–90 days. Additionally, some clients may begin seeing improvements in as little as 30 days depending on reporting accuracy and account history.

Schedule Your Free Credit Consultation with Masters Credit Consultants

If repossessions, charge-offs, collections, or late payments are hurting your score, Masters Credit Consultants may be able to help.

📞 Phone: 1-844-620-8796

🌐 Website: https://www.masterscredit.com

📅 Free Consultation:

https://masterscreditconsultantsfreeconsultationbooknow.as.me/schedule/912546ad/appointment/31582691/calendar/6643355

Additional Helpful Links

- Homepage: https://www.masterscredit.com

- Blog Hub: https://www.masterscredit.com/blogs/

- Consultation Page:

https://masterscreditconsultantsfreeconsultationbooknow.as.me/schedule/912546ad/appointment/31582691/calendar/6643355

People Also Ask

Is a repossession worse than a charge-off?

A repossession may hurt more because it often includes multiple negative events, including late payments, collections, and deficiency balances.

Can a charge-off be removed from a credit report?

Possibly. If reporting is inaccurate, outdated, incomplete, or unverifiable, disputes may help challenge the account.

Do I still owe money after repossession?

Yes. If the lender sells the vehicle for less than the remaining balance, you may still owe a deficiency balance.

Can repossession and charge-off appear together?

Yes. Auto loans frequently show both repossession and charge-off reporting simultaneously.

Related Questions

- How to fix credit after repossession

- How to remove a charge-off from your credit report

- What happens after voluntary repossession

- Can you finance a car after repossession

- Best ways to rebuild credit after charge-off

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment