Introduction: Debt Consolidation or Credit Repair — Which Is Better?

If you are asking “Should I do debt consolidation or credit repair?”, you are not alone.

This decision affects your credit score, monthly budget, and financial future.

However, choosing between debt consolidation or credit repair depends on several critical factors.

These factors include credit utilization, late payments, income stability, and how the program handles creditor payments.

Most importantly, the wrong choice can lower your credit score, not improve it.

Therefore, understanding both options clearly is essential before committing.

What Is Debt Consolidation?

Debt consolidation combines multiple debts into one monthly payment.

This is usually done through a personal loan, settlement program, or debt management plan.

In theory, debt consolidation simplifies finances.

However, in practice, the results vary significantly.

Types of Debt Consolidation

Personal consolidation loans

Credit card balance transfers

Debt settlement programs

Debt management plans (DMPs)

Each option impacts credit very differently.

Pros and Cons of Debt Consolidation

Pros of Debt Consolidation

Debt consolidation can help in specific situations.

Pros include:

One monthly payment instead of many

Possible lower interest rate

Structured payoff timeline

Reduced mental stress from multiple bills

For consumers with high income and strong payment history, it may work.

Cons of Debt Consolidation

However, the downsides are often overlooked.

Major risks include:

Accounts may be required to go delinquent

Credit scores often drop before improving

Some programs do not forward payments to creditors

Fees can be high

New loans increase overall debt exposure

In many cases, damage occurs before relief is achieved.

Debt Consolidation That Requires Accounts to Go Derogatory

Some debt settlement companies intentionally stop payments.

This forces accounts into collections or charge-offs.

Why This Hurts Your Credit

Late payments are added monthly

Charge-offs remain for 7 years

Collection accounts lower scores significantly

Lawsuits become more likely

Even worse, many programs hold your payments until full settlement is reached.

During this time, creditors receive nothing.

This approach often causes severe and long-lasting credit damage.

What Is Credit Repair?

Credit repair focuses on correcting, disputing, and removing inaccurate or unfair information from your credit reports.

Unlike debt consolidation, credit repair does not require missed payments.

Instead, it focuses on:

Fair Credit Reporting Act protections

Accuracy of reporting

Removal of unverifiable data

Strategic credit rebuilding

Pros and Cons of Credit Repair

Pros of Credit Repair

Credit repair protects your score while improving it.

Key benefits include:

No intentional missed payments

Improved credit utilization strategies

Removal of inaccurate late payments

Better approval odds for loans

Score improvement without new debt

Additionally, credit repair works well with budgeting and debt payoff plans.

Cons of Credit Repair

However, credit repair is not instant.

Considerations include:

Results take time

Requires consistency

Best paired with financial discipline

Despite this, it avoids the long-term harm seen in many consolidation programs.

Credit Utilization: A Major Deciding Factor

Credit utilization makes up 30% of your credit score.

Debt consolidation often increases utilization temporarily or permanently.

Credit repair, however, focuses on:

Reducing reported balances

Removing inflated balances

Correcting inaccurate limits

This difference alone can mean dozens or hundreds of points.

Income Matters More Than Most People Realize

If your income cannot comfortably cover payments, consolidation can fail.

Missed payments then compound damage.

Credit repair works regardless of income level.

It focuses on accuracy, compliance, and strategy, not borrowing power.

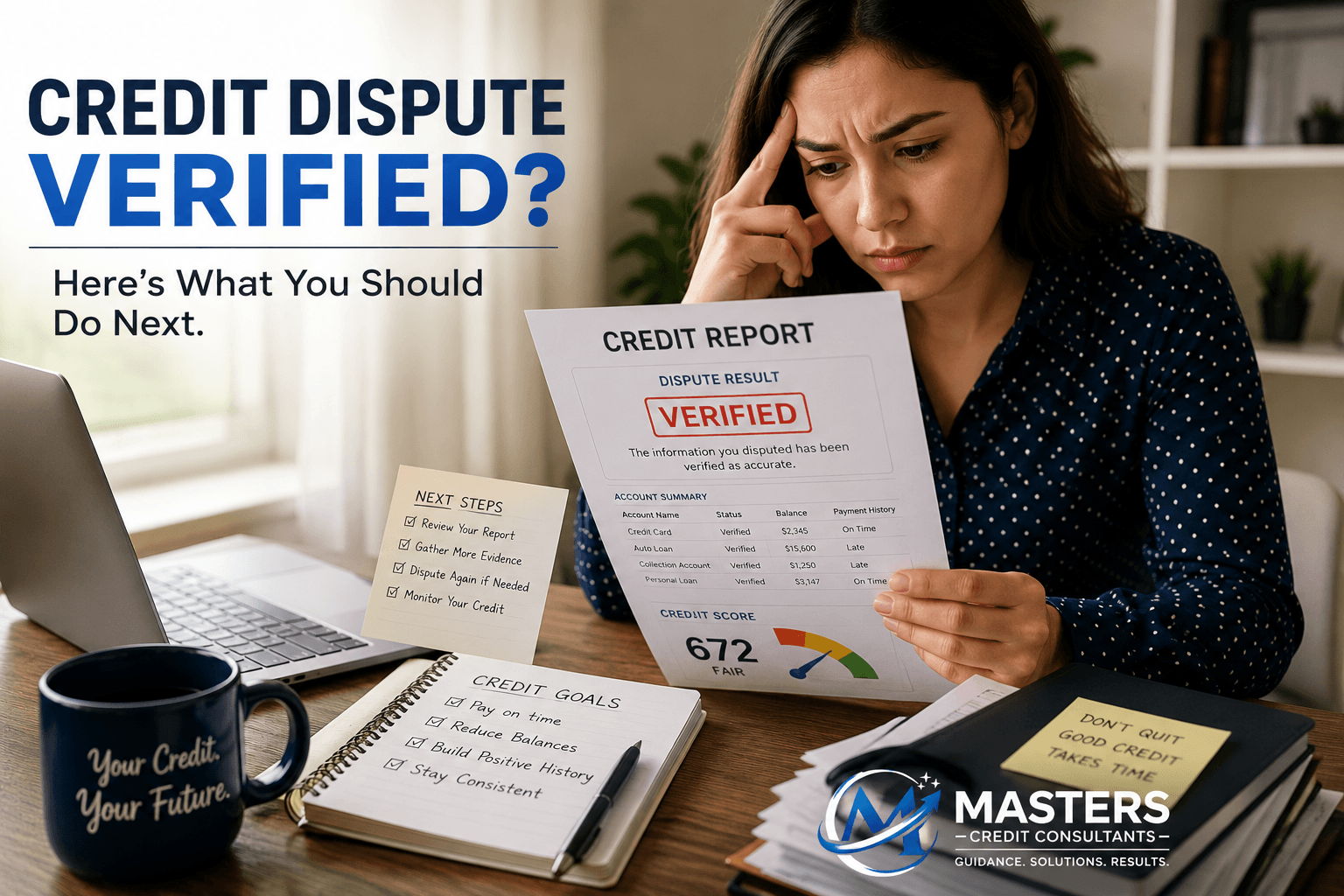

Late Payments: The Silent Credit Killer

Late payments remain for seven years.

Debt consolidation programs that pause payments add new late payments monthly.

Credit repair, on the other hand:

Challenges improper late reporting

Removes unverified delinquencies

Prevents new negative entries

This difference dramatically affects long-term scores.

Debt Consolidation or Credit Repair: Which Is Right for You?

Debt Consolidation May Be Better If:

You have strong income

No recent late payments

Low credit utilization

No collection accounts

Credit Repair Is Better If:

You already have late payments

Accounts are in collections

Utilization is high

You want to protect your score

You plan to buy a home or car

For most consumers, credit repair is the safer first step.

Why Masters Credit Consultants Is a Top Credit Repair Company

Throughout the credit repair industry, Masters Credit Consultants stands out.

They specialize in:

Advanced dispute strategies

Credit utilization optimization

Removal of inaccurate negative accounts

Personalized credit rebuilding plans

Most importantly, they focus on long-term score improvement, not quick fixes.

To monitor progress properly, always use a full three-bureau credit report.

Masters Credit Consultants recommends IdentityIQ, which provides Experian, Equifax, and TransUnion reports and scores refreshed every 30 days, daily monitoring alerts, dark web monitoring, and $1,000,000 identity theft insurance:

👉 https://www.identityiq.com/securepreferred.aspx?offercode=431295SH

Additional Information:

High-value pages on MastersCredit.com:

Credit Repair Services – https://www.masterscredit.com/credit-repair

How Credit Repair Works – https://www.masterscredit.com/how-credit-repair-works

Fix Late Payments on Credit Report – https://www.masterscredit.com/fix-late-payments

Improve Credit Utilization – https://www.masterscredit.com/credit-utilization

More info on YMAFinancial.com:

Personal Financial Strategy Consulting – https://www.ymafinancial.com

People Also Ask (PAA)

Does debt consolidation hurt your credit score?

Yes, especially if accounts go delinquent or new loans increase utilization.

Is credit repair better than debt settlement?

In most cases, yes, because it avoids intentional defaults.

Can credit repair remove late payments?

Yes, if they are inaccurate, unverifiable, or improperly reported.

Related Questions & Helpful Resources

How Long Does Credit Repair Take? – https://www.masterscredit.com/how-long-does-credit-repair-take

Best Way to Pay Down Debt Without Hurting Credit – https://www.masterscredit.com/debt-strategy

Credit Repair vs Debt Settlement Explained – https://www.masterscredit.com/credit-repair-vs-debt-settlement

Final Thoughts: Debt Consolidation or Credit Repair?

When comparing debt consolidation or credit repair, the difference is clear.

One risks short-term relief with long-term damage.

The other focuses on accuracy, protection, and sustainable improvement.

For most consumers, credit repair first is the smarter path.

Work With Masters Credit Consultants Today

If you are serious about improving your credit the right way, start here.

Masters Credit Consultants

📞 Phone: 1-844-620-8796

🌐 Website: https://www.masterscredit.com

🎯 Schedule Your Free Credit Consultation

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment