If you’ve ever asked, “why is my credit card balance not showing after I made a payment?”, you’re not alone. You pay your bill expecting to see your balance drop — or disappear — only to notice that it hasn’t updated yet. This confusion usually happens because of timing differences between your due date, statement closing date, and payment processing date.

In this article, we’ll break down exactly why your credit card balance may not be reflecting your payment right away, how to align your payments with your statement cycle, and why not charging your card until after the statement date can ensure your credit reports show an accurate (and lower) balance.

Understanding Why Your Credit Card Balance Isn’t Showing After a Payment

There are several reasons why your credit card balance might not show after a payment — and it’s almost always tied to how your billing and reporting cycles work.

Payment processing and verification holds

When you make a payment, it usually takes 1–3 business days to process. Some banks or credit card issuers may place temporary holds, especially if it’s your first payment from a new account or a large amount. During this time, the payment is “pending,” meaning it hasn’t yet posted to your available credit or reported to the credit bureaus.

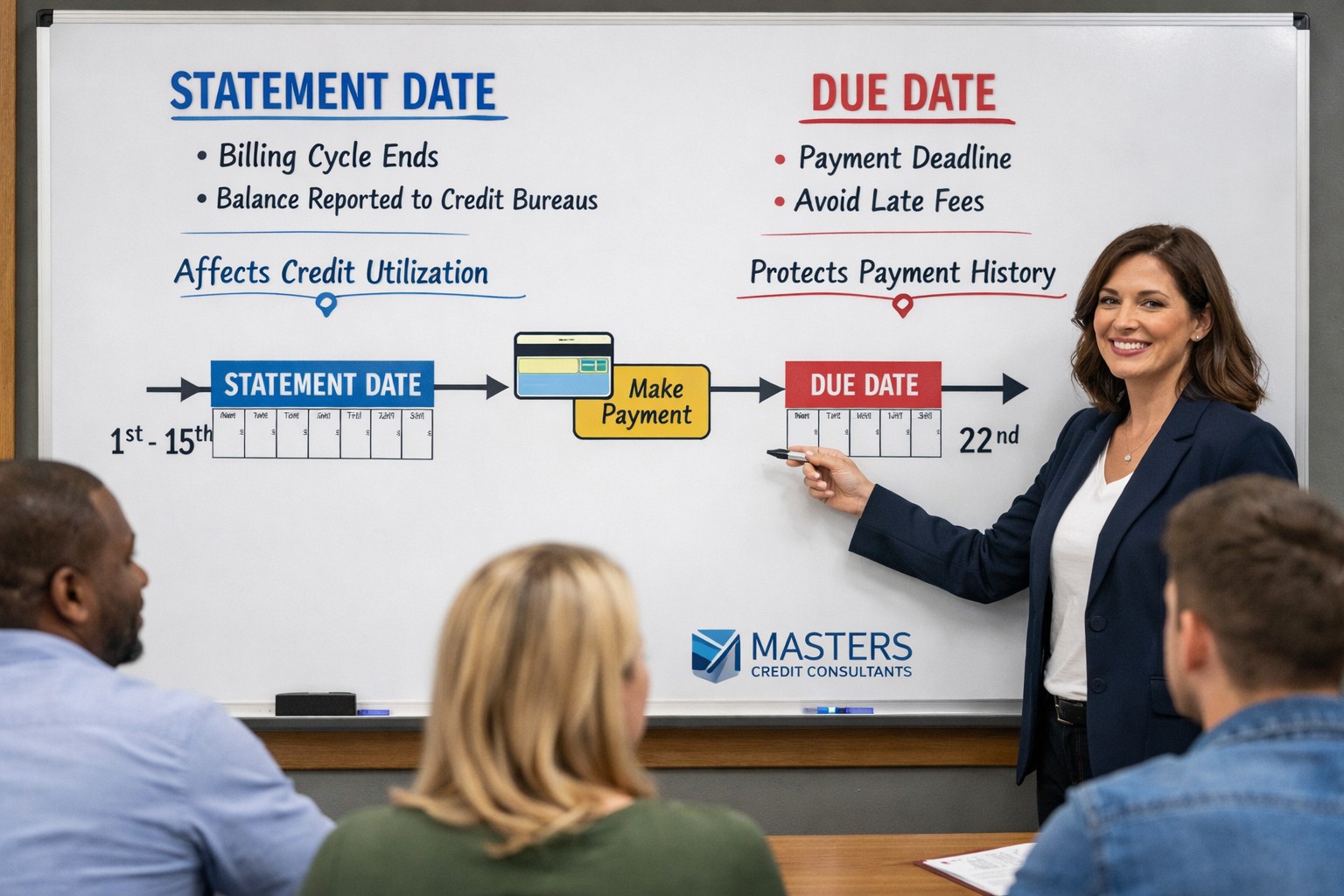

The Difference Between Statement Date and Due Date

Your statement closing date and payment due date are two separate things — and mixing them up often explains why your credit card balance isn’t showing after you made a payment.

Statement closing date is the end of your billing cycle. This is when your balance is finalized and sent to the credit bureaus.

Payment due date is the deadline to pay the previous statement’s balance to avoid interest or late fees.

Example — Paying on the due date but using the card before the statement closes

Let’s say your payment is due on the 15th of each month, and your statement closes on the 18th.

You pay your balance in full on the 15th, which satisfies your obligation and avoids interest.

However, if you use your credit card again on the 16th or 17th — before the statement closes on the 18th — those new charges will show up as part of your current balance.

When your lender reports to the credit bureaus after the 18th, the new purchases will appear on your report — making it look like you still have a balance even though you “paid in full.”

This timing difference is one of the biggest reasons consumers ask: “Why is my credit card balance not showing after I made a payment?” The solution is simple — pay your balance before the statement closing date and avoid new charges until after the statement closes.

How to Ensure Your Payment Reflects Correctly

Understanding when and how payments post can help you make smarter moves that improve your credit report and score.

Pay before the statement closing date

To make sure your balance reports as low as possible to the credit bureaus, pay your bill a few days before the statement closing date — not just by the due date. This ensures your reported balance reflects your payment, not the pre-payment amount.

Wait to make new purchases until after the statement closes

Even though it’s tempting to use your available credit right after paying it off, doing so before your statement closes can cause your balance to report higher. If you want your report to show zero or low utilization, wait until after your statement date to start spending again.

Allow time for payment posting

After you make a payment, give it a few days to post. Payments made on weekends or holidays may not process immediately, and online updates to your available balance can lag behind real-time posting.

Why Timing Matters for Your Credit Report

Understanding why your credit card balance isn’t showing after a payment directly ties to how your issuer reports to the credit bureaus.

Credit card companies typically send your balance information to Experian, Equifax, and TransUnion once per billing cycle — usually right after the statement closing date. If your payment happens after that, the previous balance gets reported. This means your credit utilization (the ratio of your balance to your limit) may appear higher until the next cycle.

A small timing tweak can boost your credit score

If your goal is to improve your credit score, simply pay early — ideally a few days before the statement closes — and don’t use your card again until that statement date passes. This ensures your reported balance is lower, reducing utilization and increasing your score.

Common Reasons Your Balance Isn’t Updating

Here are the most common scenarios that lead to confusion:

Payment made after statement closing date – Your payment won’t be reflected until the next reporting cycle.

Payment on due date + new purchases before statement date – You technically paid on time, but new charges made before the closing date make it appear like your balance never dropped.

Pending or held payments – Banks may hold payments for verification, especially large or unusual ones.

New transactions or fees – Annual fees or pending authorizations can make your balance appear unchanged.

Issuer reporting lag – Credit card companies often report 1–5 days after statement closing, so updates may take time to appear on your report.

Step-by-Step Strategy to Keep Your Reported Balances Low

Identify your statement closing date and due date in your online account.

Schedule your payment at least three days before the closing date.

Avoid new charges until after your statement closes.

Wait for the new cycle to begin before checking your credit report for updates.

Review your credit reports monthly to confirm the updated balances.

By mastering this routine, you’ll never wonder again, “why is my credit card balance not showing after I made a payment?”

Masters Credit Consultants — Your Partner for Credit Optimization

Timing your payments correctly is just one piece of the credit improvement puzzle. If you’re dealing with confusing balances, reporting errors, or inaccurate information on your credit report, Masters Credit Consultants can help.

They specialize in:

Removing inaccurate or outdated information from credit reports.

Coaching you on payment timing and utilization strategies.

Providing expert insights into how your credit data impacts loan approvals and credit scores.

Masters Credit Consultants is recognized as one of the top credit repair companies in the nation for helping clients boost their scores and reach financial goals.

📞 Schedule Your Free Credit Consultation Today

Masters Credit Consultants

📞 Phone: 1-844-620-8796

🌐 Website: www.masterscredit.com

📅 Schedule Now: Free Credit Consultation

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment