When it comes to managing your finances, understanding how different factors can impact your credit score is crucial. One such factor that can have a significant impact on your creditworthiness is a charge-off. In this comprehensive guide, we will delve into the details of what a charge-off is, how it affects your credit score, and what steps you can take to mitigate its impact.

What is a Charge-off?

A charge-off occurs when a creditor decides to write off a debt as uncollectible. This typically happens when you have fallen behind on your payments for a prolonged period, usually six months or more. While a charge-off is a significant negative mark on your credit report, it doesn’t mean that you are absolved of your debt obligation. You are still responsible for repaying the debt.

Understanding the Impact on Your Credit Score:

A charge-off can have a detrimental effect on your credit score. When a charge-off is reported to the credit bureaus, it indicates that you have failed to meet your financial obligations, which can significantly lower your creditworthiness. The exact impact on your credit score depends on various factors, including the overall health of your credit profile, the amount of the charge-off, and how recent it is.

Negative Effects on Your Credit History:

Once a charge-off is reported, it remains on your credit report for up to seven years from the date of the first delinquency. During this period, the charge-off will be visible to lenders and can negatively impact your ability to obtain new credit, secure favorable interest rates, or even rent a property. Potential lenders may view a charge-off as an indication of financial irresponsibility, making them hesitant to extend credit to you.

How Charge-offs Compare to Other Negative Marks:

While a charge-off is undoubtedly damaging to your credit score, it is important to understand how it compares to other negative marks on your credit report. Charge-offs are typically considered more severe than late payments or collection accounts. However, they are generally not as severe as bankruptcies or foreclosures. It is crucial to note that a single charge-off can significantly impact your creditworthiness, and multiple charge-offs can further worsen the situation.

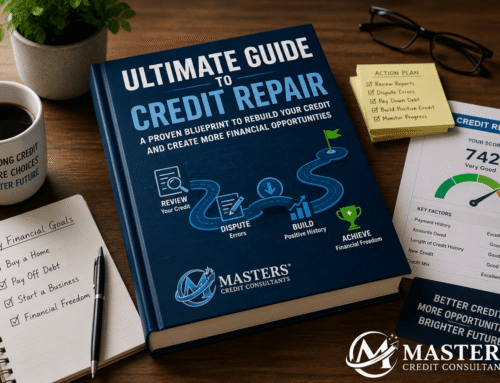

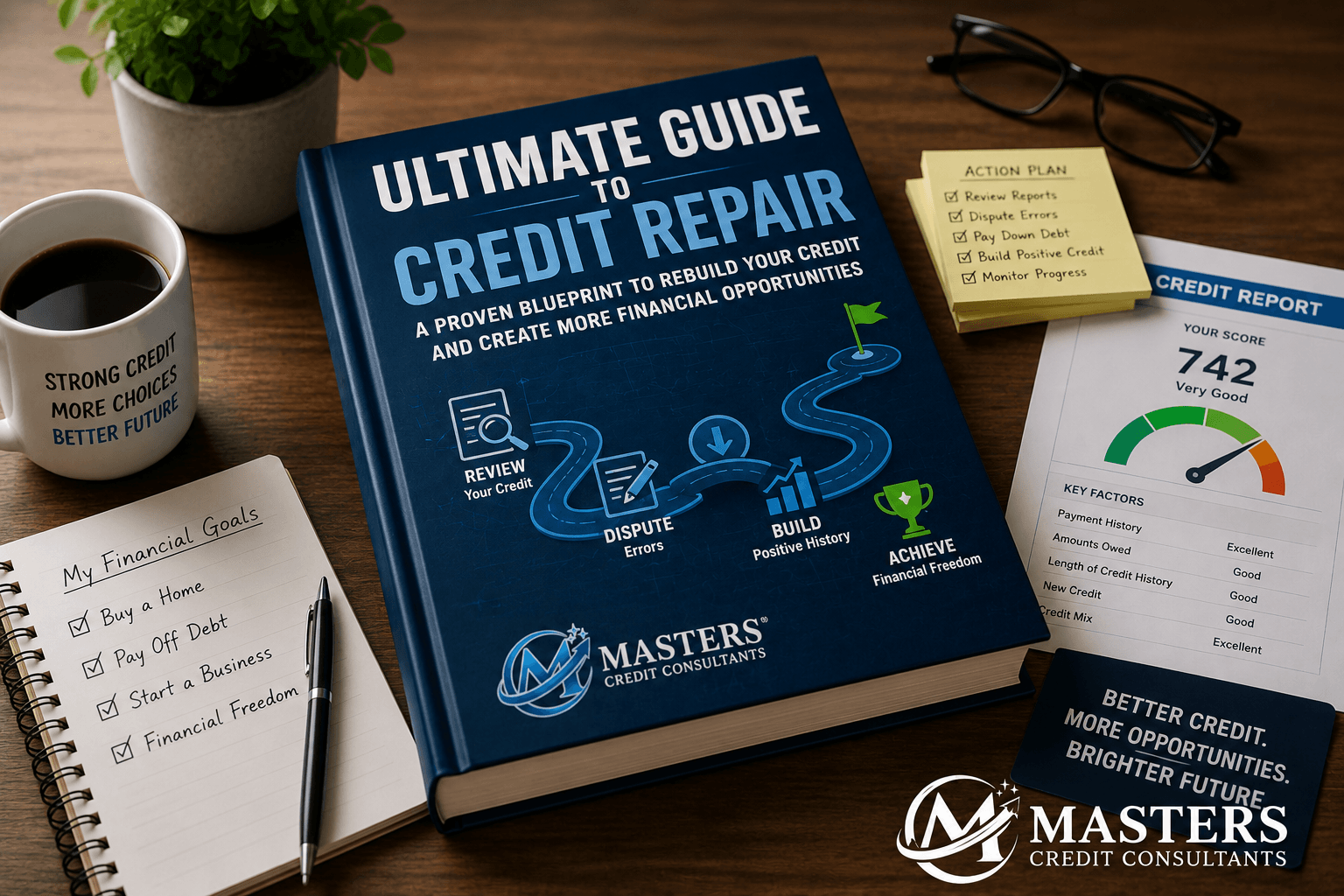

Mitigating the Impact of a Charge-off:

Although a charge-off can have a significant impact on your credit score, there are steps you can take to mitigate its effects and work towards credit repair. Here are some strategies to consider:

a) Payment Arrangements: Reach out to the creditor and try to negotiate a payment arrangement. In some cases, they may be willing to remove the charge-off from your credit report in exchange for payment.

b) Paying off the Debt: Settle the debt in full or negotiate a settlement amount with the creditor. While the charge-off will still be visible on your credit report, showing that you have satisfied the debt can demonstrate your commitment to resolving your financial obligations.

c) Establish Positive Credit History: Focus on building a positive credit history by making timely payments on your current debts and keeping your credit utilization low. Over time, positive credit behavior can help offset the negative impact of the charge-off.

d) Dispute Inaccurate Information: Review your credit report carefully and dispute any inaccuracies or inconsistencies. The credit bureaus are obligated to investigate and correct any errors found.

Factors Affecting the Severity of the Impact

- Credit History: The length of your credit history plays a role in determining the impact of a charge-off. If you have a long history of responsible credit management, the negative impact may be relatively less severe.

- Credit Utilization Ratio: Your credit utilization ratio, which is the amount of credit you are currently using compared to your total available credit, can also influence the impact of a charge-off. Maintaining a low credit utilization ratio demonstrates responsible credit management.

- Additional Negative Items: If your credit report already contains other negative items, such as late payments or collection accounts, the impact of a charge-off may be amplified.

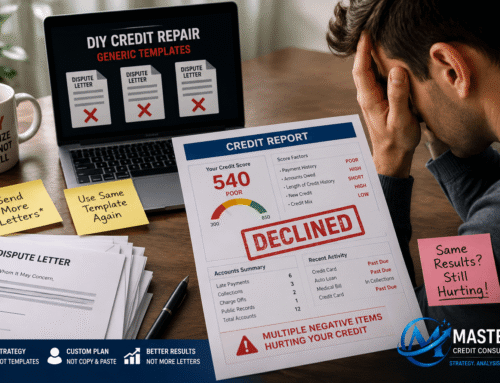

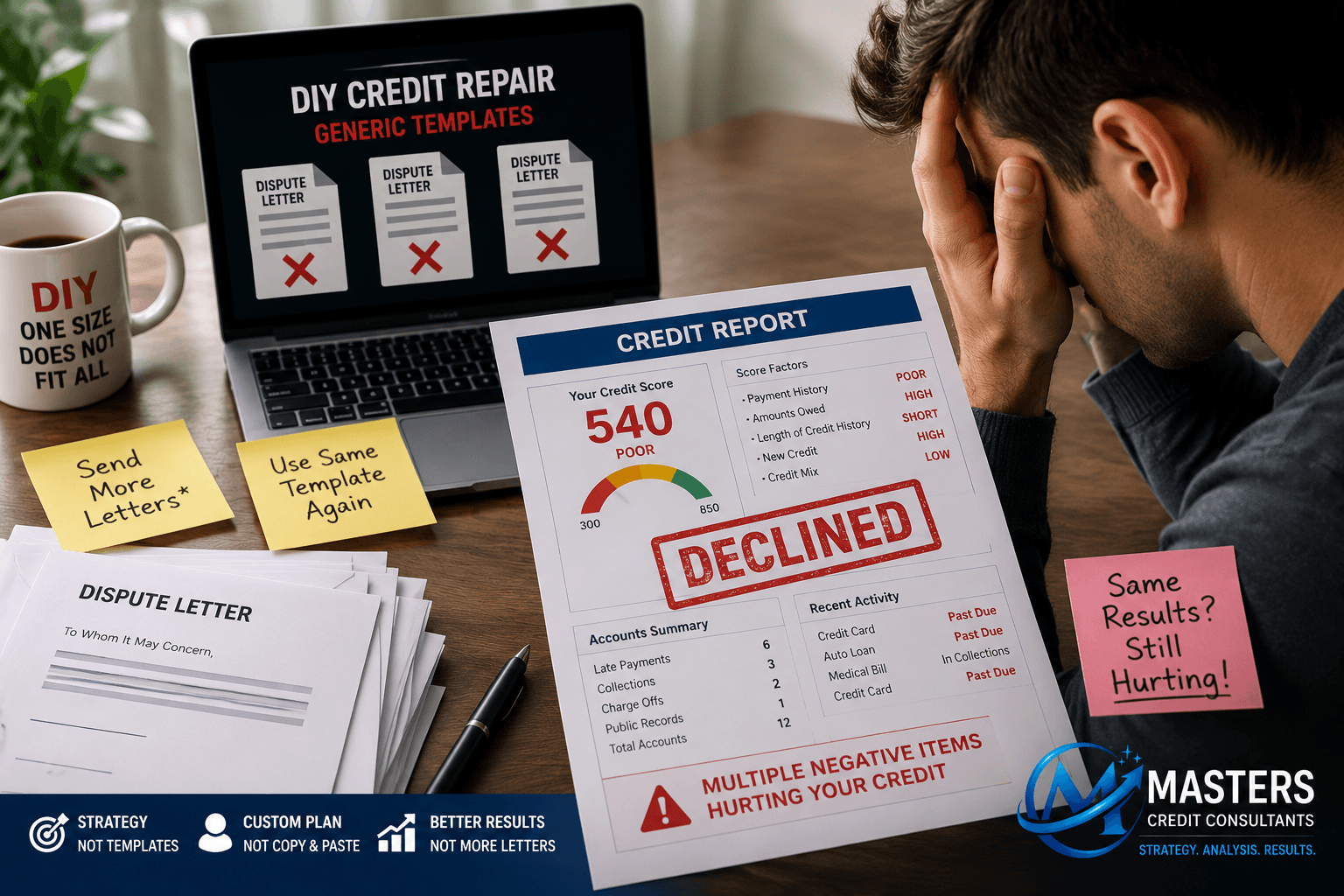

Seeking Professional Assistance:

If you find yourself overwhelmed by the complexities of dealing with a charge-off and its impact on your credit score, seeking professional assistance can be beneficial. Credit counseling agencies or reputable credit repair companies can provide guidance, help you navigate the credit repair process, and provide strategies to improve your creditworthiness.

A charge-off can have a substantial impact on your credit score and overall creditworthiness. However, it is not the end of the road. By understanding the consequences of a charge-off and taking proactive steps to address it, you can begin the journey toward credit repair. Remember, responsible financial management, consistent payments, and positive credit behavior are key to rebuilding your creditworthiness over time.

We have a new location: Credit repair San Diego CA is now open!

Got charge-offs? We can help your credit score!

Got charge-offs? We can help your credit score!

We understand life gets busy and charge-offs can happen! Luckily, our team at Masters Credit Consultants knows how to deal with Charge-offs head on! Do yourself a favor and signup for our free credit consultation. We’ll take a deep dive into your credit history and show you what needs to be done to repair your credit. Signup here or call now: 1-844-620-8796

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment