How to Remove a Repossession From Your Credit Report in 2026

A repossession can seriously damage your credit score. However, many consumers do not realize that some repossession accounts may contain inaccurate, incomplete, outdated, or unverifiable information. Because of this, there are legal methods that may help remove a repossession from your credit report in 2026.

If you are trying to rebuild your credit after a vehicle repossession, this guide explains the fastest strategies that may help improve your credit profile legally and effectively.

In This Article You’ll Learn

- How repossessions affect your credit score

- Legal ways to dispute repossession accounts

- How to rebuild your credit after repossession

- The difference between paid repossessions and deleted repossessions

- How professional credit repair may help

Table of Contents

- What Is a Repossession?

- How Long Does a Repossession Stay on Your Credit Report?

- Can a Repossession Be Removed Early?

- Common Repossession Reporting Errors

- How to Dispute a Repossession in 2026

- Should You Pay a Repossession Balance?

- How to Rebuild Credit After Repossession

- Best Credit Building Tools in 2026

- Why Clients Choose Masters Credit Consultants

- People Also Ask

- Related Questions

Can You Remove a Repossession From Your Credit Report?

Yes, a repossession may potentially be removed from your credit report if the account contains inaccurate, incomplete, outdated, duplicated, or unverifiable information under the Fair Credit Reporting Act (FCRA). Consumers may dispute repossession accounts directly with the credit bureaus or work with a professional credit repair company for assistance.

What Is a Repossession?

A repossession happens when a lender takes back a financed vehicle after missed payments. Once the vehicle is repossessed, the lender often sells the vehicle at auction to recover part of the remaining balance.

Unfortunately, repossessions usually hurt your credit in several ways:

- Payment history damage

- Increased debt-to-income concerns

- Collection account risk

- Deficiency balance reporting

- Major score drops

In many cases, consumers may see their scores drop between 80–150 points depending on the overall profile.

How Long Does a Repossession Stay on Your Credit Report?

A repossession can typically remain on your credit report for up to 7 years from the original delinquency date.

However, many consumers search for ways to remove repossession credit damage sooner because waiting seven years can severely affect:

- Loan approvals

- Interest rates

- Mortgage eligibility

- Auto financing

- Credit card approvals

Because of this, disputing inaccurate reporting becomes extremely important.

For additional insight, read:

- “How Long Does a Repossession Stay on Your Credit Report?” — Masters Credit Consultants Blog Hub

- “Repossession vs Charge-Off Explained” — Masters Credit Consultants Homepage

Can a Repossession Be Removed Early?

Yes — sometimes.

A repossession may potentially be removed early if:

- Dates are inaccurate

- Payment history is incorrect

- Account balances are wrong

- The lender cannot verify the account

- Duplicate reporting exists

- The account violates FCRA reporting standards

Important:

Not every repossession can be removed. However, many repossession accounts contain reporting inconsistencies that deserve investigation.

⚠️ NOTE!

Credit bureaus must verify disputed information under federal law. If they cannot properly verify the account, the item may need to be corrected or removed.

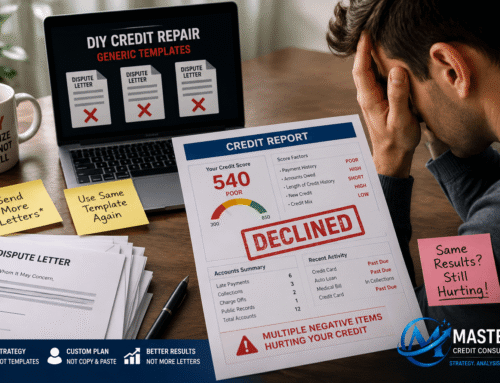

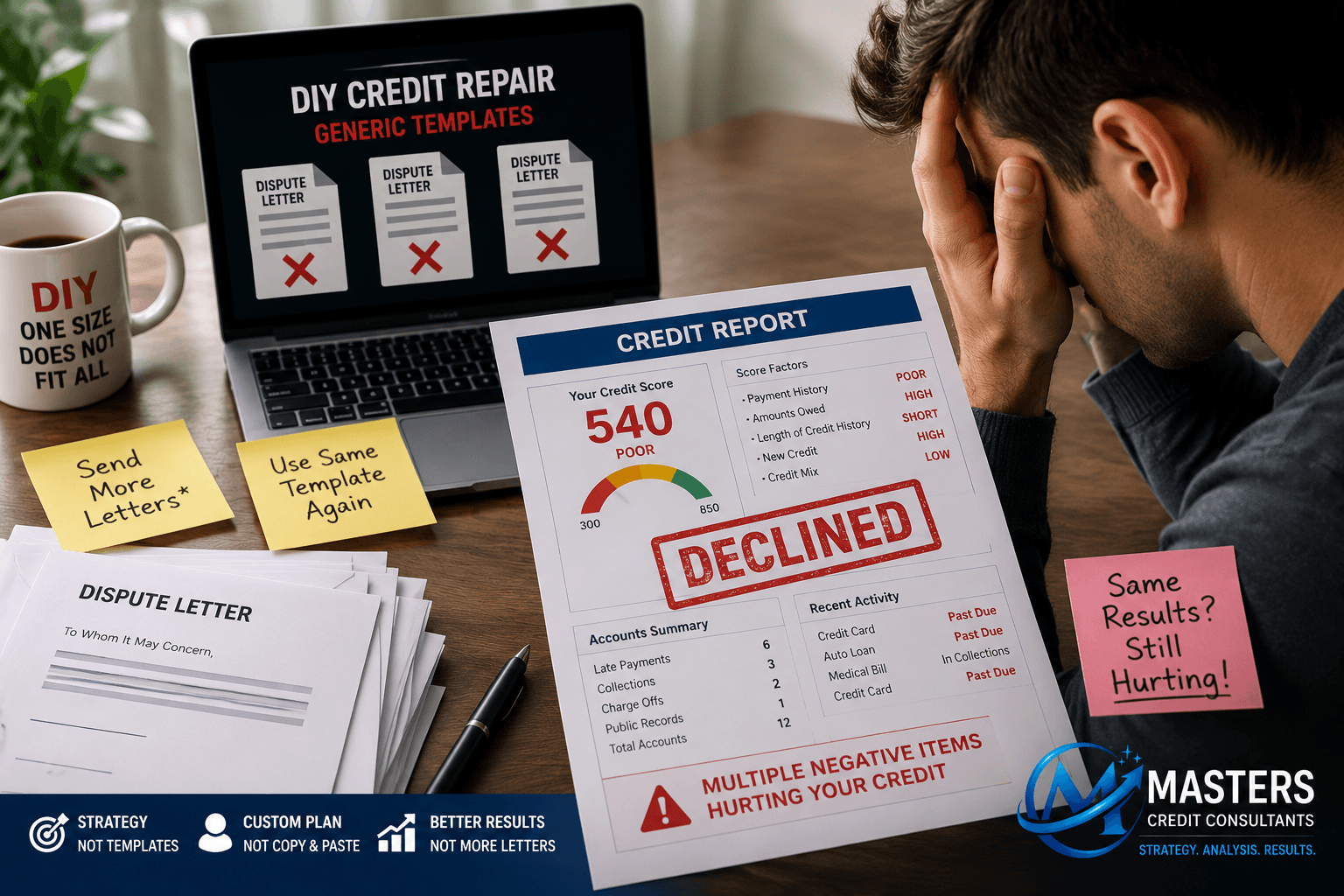

Common Repossession Reporting Errors

Many repossession accounts contain issues consumers never notice.

Common Errors Include:

- Wrong balance amounts

- Incorrect late payment history

- Duplicate repossession listings

- Incorrect auction deficiency balances

- Wrong dates

- Inconsistent reporting between bureaus

- Incomplete account details

- Accounts reported after legal reporting limits

Because credit reporting systems are automated heavily, mistakes happen frequently.

How to Dispute a Repossession in 2026

If you want to remove repossession credit damage, the dispute process matters.

Step 1 — Review All 3 Credit Reports

You should carefully review:

- Experian

- Equifax

- TransUnion

Look for inconsistencies between all three reports.

For ongoing monitoring, many consumers use IdentityIQ for 3-bureau monitoring and credit tracking with a $1 trial (7-day trial).

IdentityIQ includes:

- Experian, Equifax, and TransUnion monitoring

- Daily alerts

- Score tracking

- Dark web monitoring

- $1,000,000 identity theft insurance

Step 2 — Document All Errors

You should gather:

- Account statements

- Payment records

- Auction paperwork

- Loan agreements

- Credit report screenshots

Documentation strengthens disputes significantly.

Step 3 — Submit Disputes Properly

You may dispute:

- Directly with credit bureaus

- Directly with lenders

- Through CFPB complaints when appropriate

The Fair Credit Reporting Act requires investigations into disputed information.

Step 4 — Follow Up Consistently

Many consumers stop after one dispute.

However, successful credit repair often requires:

- Multiple investigation rounds

- Documentation updates

- Ongoing monitoring

- Strategy adjustments

Consistency matters heavily in credit restoration.

Should You Pay a Repossession Balance?

This depends on the situation.

Paying a repossession balance does NOT automatically remove the repossession from your credit report.

Many consumers misunderstand this.

Instead:

- A paid repossession may still report negatively

- The account may simply update to “Paid”

- Score improvements vary

However, resolving balances may help:

- Reduce collection activity

- Improve debt ratios

- Help future underwriting reviews

How to Rebuild Credit After Repossession

Removing repossession credit damage is only part of recovery.

You also need new positive accounts reporting consistently.

Best Ways to Rebuild Credit Fast

Lower Credit Utilization

High utilization can suppress scores dramatically.

Experts often recommend staying below 10% utilization for optimal scoring.

Add Positive Credit Accounts

Positive reporting helps offset older negative accounts.

Many consumers use secured cards responsibly to rebuild.

Popular options include:

Maintain Perfect Payment History

Payment history remains the largest scoring factor.

Even one new late payment can slow recovery significantly.

Avoid Excessive Hard Inquiries

Too many applications may temporarily lower scores further.

Apply strategically.

Schedule Your Credit Consultation Now

If you are struggling with repossession reporting issues, inaccurate negative accounts, or low credit scores, working with a professional credit repair company may help improve your overall credit profile.

👉 Schedule Your Free Consultation Here:

Free Credit Consultation

Why Clients Choose Masters Credit Consultants

Why Clients Choose Masters Credit Consultants

With a 5.0-star rating across 80+ verified reviews, clients consistently trust Masters Credit Consultants to deliver real results and guidance they can rely on.

Many consumers choose Masters Credit Consultants because the company focuses on:

- Credit report analysis

- Dispute strategy assistance

- Credit education

- Score rebuilding guidance

- Ongoing client communication

- Personalized action plans

Additionally, many clients see results in 60–90 days, while some may see improvements even sooner depending on the credit profile.

Schedule Your Free Credit Consultation with Masters Credit Consultants

If you are trying to remove a repossession from your credit report in 2026, professional guidance may help you identify reporting errors and create a personalized recovery strategy.

📞 Phone: 1-844-620-8796

🌐 Website: Masters Credit Consultants

👉 Schedule Your Free Consultation:

Book Your Consultation Now

Additional Helpful Links

- “How Long Does a Repossession Stay on Your Credit Report?”

Masters Credit Consultants Blog Hub - “Repossession vs Charge-Off Explained”

Masters Credit Consultants Homepage - “Why Do I Owe a Balance After My Car Was Repossessed and Auctioned?”

Masters Credit Consultants Blog Hub - “How Auto Repossession Affects Credit Score”

Masters Credit Consultants Blog Hub

People Also Ask

Can paying off a repossession improve credit?

Yes, paying a repossession balance may help improve underwriting evaluations and debt ratios. However, the repossession may still remain on the report.

How many points does a repossession lower your credit score?

A repossession may lower scores significantly, sometimes between 80–150 points depending on the overall profile.

Can repossessions be removed if paid?

Possibly. Payment does not automatically remove repossessions, but inaccurate reporting may still qualify for disputes.

Is a voluntary repossession better?

Voluntary repossession may look slightly better to lenders, but it still negatively impacts credit.

Related Questions

- How do I rebuild credit after repossession?

- Can repossessions be disputed legally?

- How long does a deficiency balance last?

- Should I settle a repossession collection?

- What credit score is needed after repossession recovery?

- Can I finance another vehicle after repossession?

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment