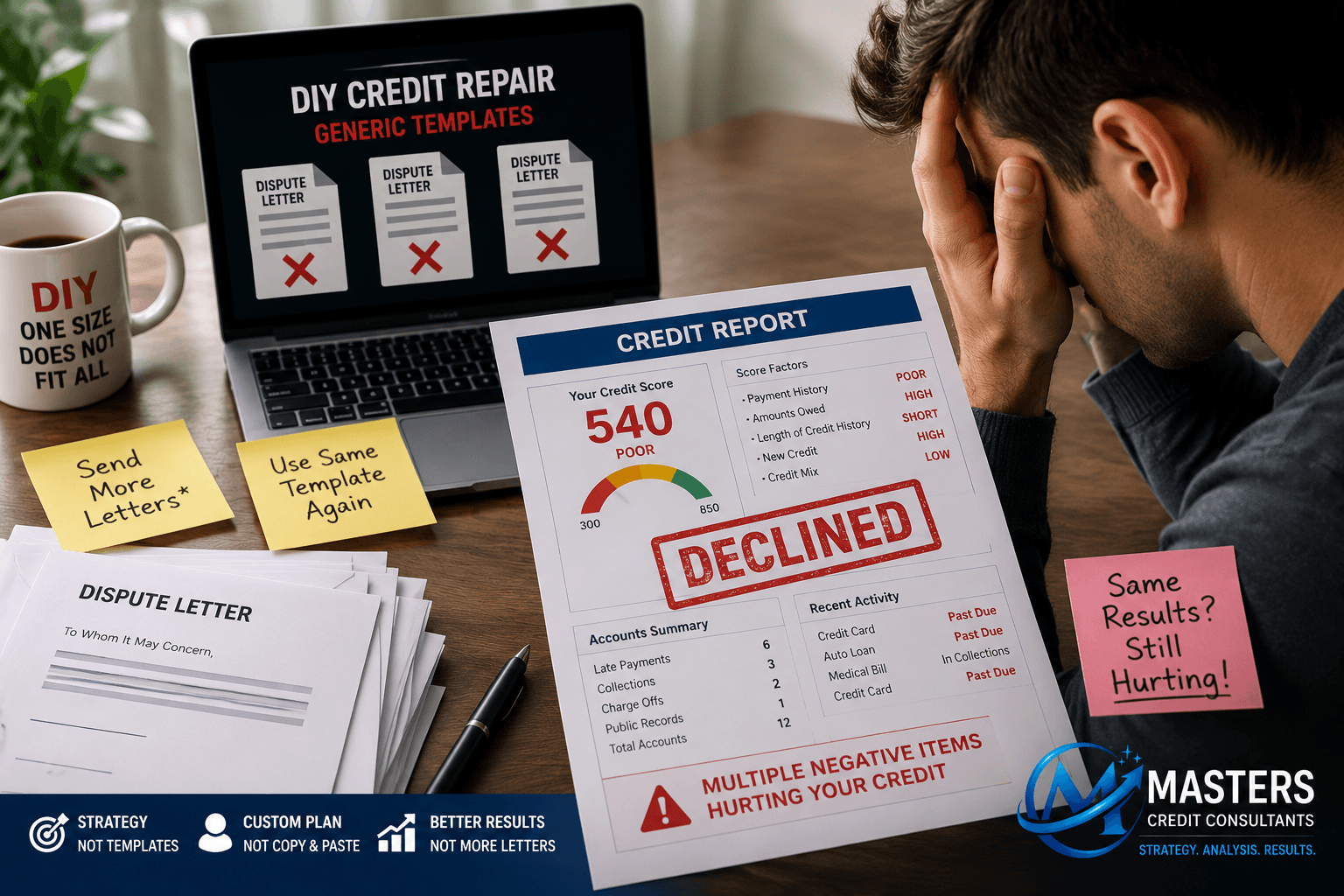

DIY Credit Repair May Be Hurting Your Credit: Why Strategy Matters More Than Templates

Can DIY Credit Repair Actually Hurt Your Chances of Improving Your Credit?

Yes—sometimes it can. While consumers have every legal right to dispute inaccurate information on their credit reports, repeatedly using generic dispute letters or following a one-size-fits-all approach may make future disputes more challenging. Credit repair isn’t simply about sending letters—it’s about understanding your credit report, your dispute history, and choosing the right strategy for each account.

In This Article You’ll Learn

- Why inexpensive DIY credit repair programs often produce inconsistent results

- What comments like “Dispute Resolved; Consumer Disagrees” actually mean

- Why strategy—not templates—is often the biggest difference between successful and unsuccessful credit disputes

Table of Contents

- What Is DIY Credit Repair?

- Why Millions of Consumers Choose DIY Credit Repair

- Why Cheap Credit Repair Programs Cost So Little

- Credit Repair Isn’t One-Size-Fits-All

- What We Commonly See When Reviewing Credit Reports

- What Those Credit Report Comments Really Mean

- Why Previous Disputes Matter

- DIY Credit Repair vs Professional Credit Repair

- The Biggest DIY Credit Repair Mistakes

- How Credit Bureaus Investigate Disputes

- When Should You Stop Sending Generic Dispute Letters?

- Frequently Asked Questions

- Final Thoughts

What Is DIY Credit Repair?

DIY credit repair is exactly what it sounds like—repairing your own credit without hiring a professional.

Some consumers purchase inexpensive online memberships that provide dispute letter templates, while others search the internet for free sample letters or use automated dispute software. The goal is usually the same: remove inaccurate negative information and improve credit scores without paying for professional assistance.

There’s absolutely nothing wrong with wanting to repair your own credit.

In fact, the Fair Credit Reporting Act (FCRA) gives every consumer the right to dispute information they believe is inaccurate, incomplete, or unverifiable.

The challenge isn’t whether you can dispute your own accounts.

The challenge is knowing how to dispute them strategically.

Consumers absolutely have the right to repair their own credit. However, understanding how previous disputes, reporting history, documentation, and investigation results affect future disputes can make a significant difference in developing an effective strategy.

Why Millions of Consumers Choose DIY Credit Repair

It’s easy to understand why DIY credit repair has become so popular.

Advertisements often promise quick improvements for just a few dollars per month.

You’ll frequently see offers like:

- Credit Repair for $19

- Unlimited Disputes for $29

- Automated Credit Repair for $49

- DIY Credit Repair Kit for $99

For consumers already struggling financially, those prices are appealing. After all, if sending dispute letters is all that’s required, why spend more? Unfortunately, that’s where many people unknowingly oversimplify the credit repair process.

Why Cheap Credit Repair Programs Cost So Little

This is one of the biggest misconceptions consumers have.

Many people assume:

“If a company charges only $29 per month, they must simply be making less profit.”

In reality, inexpensive DIY credit repair programs are often built around automation.

Instead of reviewing each consumer’s credit report individually, many systems rely on standardized dispute templates that can be generated for thousands of users with minimal customization.

That business model allows providers to keep prices low because the same process is repeated across a large number of customers.

To be fair, some consumers do achieve results with template-based disputes—particularly when addressing straightforward reporting errors. However, more complex credit reports often require a much more individualized review.

Affordable doesn’t automatically mean ineffective. But low-cost DIY programs often provide limited personalization, which may not be sufficient for more complicated credit situations.

Credit Repair Isn’t One-Size-Fits-All

Imagine visiting a doctor.

Before recommending treatment, the doctor reviews your medical history, symptoms, lab work, medications, and diagnostic tests.

They don’t prescribe the same treatment to every patient.

Credit repair works much the same way.

Every credit report is unique.

Even when two people have the same collection account from the same creditor, factors such as reporting history, payment history, prior disputes, documentation, and investigation outcomes may require different approaches.

That’s one reason why experienced professionals spend time reviewing an entire credit profile before deciding how to move forward.

What We Commonly See When Reviewing Credit Reports

One of the first things we review isn’t simply the negative accounts.

We look at what has already happened.

Over the years, we’ve reviewed thousands of consumer credit reports and one pattern appears repeatedly.

Consumers often come to us after trying DIY credit repair for several months—or after using inexpensive online dispute programs.

Many of those reports contain comments such as:

- Charged Off as Bad Debt

- Consumer Disputes After Resolution

- Dispute Resolved; Customer Disagrees

- Account Was in Dispute—Now Resolved

- Subscriber Reports Dispute Resolved

- Consumer Disputes; Meets FCRA Requirements

- Account Closed at Consumer’s Request and Dispute Resolved

Most consumers never notice these comments.

To an experienced credit professional, however, they provide valuable context about the account’s dispute history.

What Those Credit Report Comments Really Mean

Seeing these remarks doesn’t automatically mean an account can never be challenged again.

However, they often indicate that:

- The account has previously been disputed.

- The credit bureau or furnisher completed an investigation.

- The information continued to be reported after that investigation.

For example, if you see:

“Dispute Resolved; Consumer Disagrees.”

It generally means an investigation took place, the reporting remained unchanged, and the consumer did not agree with the outcome.

Likewise, a remark such as:

“Consumer Disputes After Resolution.”

Often indicates the consumer continued disputing the account after a previous investigation had already concluded.

These comments don’t necessarily tell us whether the reporting is accurate or inaccurate. Instead, they help establish the account’s history, which is an important consideration when evaluating future dispute strategies.

Does “Dispute Resolved; Consumer Disagrees” mean you’ve lost your dispute?

No. It means an investigation was completed and the information continued to be reported. Depending on the circumstances, additional options may still exist, but repeating the same generic dispute may not produce a different result.

Why Previous Disputes Matter

Think of previous disputes like chapters in a book.

Every investigation becomes part of the account’s history.

When another dispute is submitted, the bureau or furnisher isn’t necessarily seeing the account for the first time—they may already have records of prior investigations.

That history can influence how future disputes are evaluated.

This is why understanding what has already been disputed, how it was disputed, and what responses were received is often an important part of developing an effective strategy.

It’s not simply about sending another letter.

It’s about understanding what has already happened and deciding whether a different approach is warranted.

DIY Credit Repair vs. Professional Credit Repair

One of the biggest misconceptions is that the only difference between DIY credit repair and working with a professional is who places the letter in the mailbox.

In reality, the difference often lies in the review process before any dispute is ever prepared.

| DIY Credit Repair | Professional Credit Review |

|---|---|

| Often relies on generic templates | Individual review of each credit profile |

| Standardized dispute process | Strategy tailored to the reporting history |

| Limited review of previous disputes | Reviews dispute history before proceeding |

| Consumer decides what to dispute | Accounts evaluated before recommendations |

| Minimal documentation review | Documentation reviewed when applicable |

| Same approach for many users | Different approach based on individual circumstances |

| Limited education | Ongoing guidance throughout the process |

| Lower upfront cost | Greater emphasis on individualized analysis |

Neither approach is inherently right or wrong.

The key difference is that one emphasizes standardization, while the other emphasizes personalization based on the consumer’s unique credit profile.

The Biggest Mistake Consumers Make

Many people believe that if one dispute letter doesn’t work, sending five more identical letters will eventually produce a different outcome.

In many cases, that simply isn’t how the investigation process works.

Effective credit repair isn’t about the number of disputes sent.

It’s about understanding why an account is being disputed, what supports the dispute, and whether a different strategy is appropriate based on the account’s history.

The 12 Biggest DIY Credit Repair Mistakes That Can Slow Your Progress

Most consumers who attempt DIY credit repair are trying to save money—not make mistakes.

Unfortunately, many of the mistakes we see aren’t caused by bad intentions. They’re caused by incomplete information and the assumption that every negative account can be handled the same way.

Let’s look at some of the most common issues.

- Using the Same Dispute Letter for Every Account

One of the biggest misconceptions about credit repair is believing one dispute letter works for everything.

A medical collection, repossession, charge-off, late payment, bankruptcy, and identity theft account all involve different circumstances.

Using the exact same template for every account ignores the unique facts behind each item.

The stronger your dispute strategy matches the facts of a specific account, the more meaningful the investigation can be than simply sending a generic template.

- Disputing Accurate Information

Federal law gives consumers the right to dispute information they believe is inaccurate or incomplete.

However, disputing information that is accurately reported simply because it’s negative may not lead to its removal.

Before submitting any dispute, ask yourself:

- Is this information inaccurate?

- Is it incomplete?

- Is it being reported consistently?

- Do I have documentation supporting my position?

- Never Reviewing Previous Dispute History

This is one of the most overlooked parts of credit repair.

Consumers often focus on the account itself while overlooking the comments that tell the story of what has already happened.

For example:

- Consumer Disputes After Resolution

- Dispute Resolved; Customer Disagrees

- Meets FCRA Requirements

- Account Was in Dispute—Now Resolved

Those remarks don’t necessarily mean future action is impossible.

They simply indicate there is already a history that should be understood before deciding what to do next.

- Assuming More Disputes Equal Better Results

This may be the biggest myth in DIY credit repair.

Many consumers think:

“If I dispute this account every month, eventually they’ll remove it.”

Unfortunately, investigations don’t always work that way.

Submitting the same dispute repeatedly without new information or a different basis may simply result in another verification of the account.

- Trusting Every Credit Repair Video on Social Media

Social media has made financial education more accessible than ever.

Unfortunately, it has also made misinformation easier to spread.

Videos promising:

- “Delete every collection in 30 days.”

- “Remove any charge-off instantly.”

- “Use this secret dispute letter.”

- “One letter removes everything.”

often oversimplify a process that depends heavily on the facts of each individual account.

There are no universally successful dispute letters.

- Focusing Only on Removing Negative Accounts

Many people believe credit repair is only about deletions.

In reality, improving a credit profile often includes:

- Building positive payment history.

- Reducing revolving utilization.

- Maintaining on-time payments.

- Avoiding unnecessary inquiries.

- Establishing healthy credit habits.

Removing negative information is only one piece of a much larger financial picture.

- Ignoring Supporting Documentation

Documentation can play an important role in certain disputes.

Depending on the circumstances, records such as account statements, payment confirmations, identity theft reports, correspondence, or other supporting documents may help clarify a consumer’s position.

Not every dispute requires documentation, but failing to organize important records can make the process more difficult.

- Disputing Everything at Once

Another common mistake is disputing every negative account simultaneously without understanding how each account relates to the others.

Some situations may require different timing or different approaches based on the facts involved.

A thoughtful strategy is often more effective than simply disputing every account immediately.

- Forgetting That Credit Reports Change

Your credit report isn’t static.

Balances update.

Payment histories change.

Accounts transfer.

Collections are sold.

New information appears.

A strategy that made sense six months ago may not be the best approach today.

That’s why periodic reviews of your credit report are important.

- Ignoring the Positive Side of Credit Building

Even if every negative item disappeared tomorrow, poor financial habits could eventually recreate the same problems.

Strong credit isn’t built only by removing negatives.

It’s also built by consistently adding positive information over time.

- Believing Every Credit Report Is the Same

One consumer may have:

- two collections

- one charge-off

- no late payments

Another may have:

- multiple charge-offs

- repossessions

- high utilization

- judgments

- recent inquiries

Although both consumers need credit improvement, their situations are completely different.

The best strategy for one person may be ineffective for another.

- Giving Up Too Early

Some consumers stop after receiving one unfavorable investigation result.

Others continue sending identical disputes month after month.

Neither extreme is ideal.

Sometimes the next step isn’t another dispute.

Sometimes it’s gathering documentation.

Sometimes it’s improving the overall credit profile.

Sometimes it’s simply reevaluating the strategy.

How Credit Bureaus Investigate Consumer Disputes

Many people imagine that a dispute immediately results in someone manually reviewing every piece of account history.

The reality is more structured.

While every situation is unique, a typical dispute process often includes:

Step 1

The consumer submits a dispute.

⬇

Step 2

The credit bureau reviews the dispute and forwards relevant information to the data furnisher when appropriate.

⬇

Step 3

The furnisher investigates the information it previously reported.

⬇

Step 4

The results are communicated back to the credit bureau.

⬇

Step 5

The bureau updates the consumer’s credit report based on the investigation results.

The outcome may include:

- Information updated

- Information corrected

- Information removed

- Information verified and continued

Understanding this process helps explain why repeatedly sending the same dispute may not always produce a different outcome.

| Myth | Fact |

|---|---|

| Every negative account can be removed. | Some information may be accurately reported and remain on a credit report for the period allowed by law. |

| More dispute letters always increase your chances. | Repeating the same dispute without a different basis may not change the investigation outcome. |

| Every DIY template works the same. | Different accounts often require different approaches based on their reporting history. |

| Cheap credit repair programs do exactly what professionals do. | Programs vary widely in the level of analysis, personalization, and support they provide. |

| Credit repair only means removing negatives. | Long-term credit improvement also includes building positive payment history and responsible credit management. |

What Happens When Generic Templates Stop Working?

One of the patterns we frequently observe is that consumers come to us after several months of sending template disputes with little or no progress.

At that point, our first question usually isn’t:

“What account do you want removed?”

Instead, it’s:

“What has already been done?”

Understanding the history matters because it helps determine whether:

- previous disputes addressed the same issue,

- reporting has changed over time,

- additional documentation exists,

- or a different strategy may be appropriate.

That’s why reviewing the entire credit picture—not just the negative account—is such an important part of the process.

DIY Credit Repair Timeline

Many consumers expect immediate results, but credit improvement often takes time.

| Timeline | What May Happen |

|---|---|

| Week 1 | Consumer sends a dispute or enrolls in a DIY program. |

| Weeks 2–4 | Credit bureau processes the dispute and coordinates the investigation. |

| Weeks 4–6 | Results are returned and the credit report is updated if changes are made. |

| Month 2 | Many DIY programs send another template regardless of the previous outcome. |

| Months 3-4 | Consumers may become frustrated if the same accounts continue reporting. |

| Next Step | Review the dispute history, reporting details, and overall strategy before deciding what to do next. |

Every credit file is different. Timelines vary depending on the accounts involved, the information provided, and the investigation process.

Not Seeing Progress? It May Be Time for a Fresh Review

If you’ve already tried repairing your credit on your own and you’re seeing comments such as “Dispute Resolved,” “Consumer Disagrees,” or “Meets FCRA Requirements,” it may be worthwhile to step back and review your overall strategy before sending another template.

A professional review isn’t about replacing your rights as a consumer—it’s about helping you better understand your credit report, your dispute history, and your available options.

Schedule a free consultation with Masters Credit Consultants to have an experienced specialist review your credit profile and discuss your next steps.

Frequently Asked Questions About DIY Credit Repair

Can I legally repair my own credit?

Yes. The Fair Credit Reporting Act (FCRA) gives consumers the right to dispute information they believe is inaccurate or incomplete. Many people successfully handle certain credit issues on their own, particularly when correcting simple reporting errors. More complex situations, however, may require a more detailed review of the credit report and dispute history.

Does DIY credit repair actually work?

It can.

Some consumers successfully resolve reporting issues using their own documentation and well-supported disputes. The outcome often depends on the specific account, the accuracy of the information being reported, and the overall strategy used—not simply whether a dispute was submitted.

Why do so many DIY credit repair programs cost only $19 or $29?

Many lower-cost DIY programs rely heavily on automation, standardized dispute templates, and self-service tools. That business model allows them to serve a large number of consumers at a lower price point.

For consumers with straightforward reporting issues, those tools may be helpful. More complex credit situations often benefit from a more individualized review.

What does “Dispute Resolved; Consumer Disagrees” mean?

This comment generally indicates that a dispute investigation has been completed, but the consumer disagrees with the outcome.

It does not automatically mean the account can never be challenged again. It simply means the account already has dispute history that should be considered before deciding on the next step.

Does disputing an account hurt my credit score?

Simply filing a dispute does not, by itself, lower your credit score.

However, consumers should understand the dispute process before repeatedly challenging the same information, especially if previous investigations have already been completed.

Can I dispute the same account more than once?

Yes.

Whether another dispute is appropriate depends on the facts of your situation, including changes in reporting, new documentation, or other relevant information. Repeating the exact same dispute without any new basis may not lead to a different outcome.

Why was my dispute verified?

A verification generally means the investigation resulted in the information continuing to be reported.

That does not necessarily answer every question about the account. It simply reflects the outcome of that investigation based on the information reviewed at that time.

Should I dispute every negative account?

Not necessarily.

Each account should be evaluated individually. Different account types, reporting histories, and circumstances may call for different approaches.

Are online dispute templates effective?

Templates can be useful for organizing information and getting started.

However, they may not address the specific facts of every account, which is one reason many consumers eventually seek a more personalized review.

Why do some people see results while others don’t?

No two credit reports are exactly alike.

Factors such as account history, documentation, reporting accuracy, previous disputes, payment history, and creditor responses can all influence the outcome of a dispute.

Is professional credit repair just sending letters for me?

A reputable credit repair company generally does much more than mail dispute letters.

The process often includes reviewing the credit report, evaluating dispute history, identifying reporting inconsistencies, monitoring progress, educating the consumer, and adjusting strategies as circumstances change.

How long does credit repair take?

There is no universal timeline.

The length of the process depends on the complexity of the credit report, the number of accounts involved, investigation timelines, and each consumer’s overall financial situation.

Be cautious of anyone guaranteeing specific timeframes or results.

What should I do before disputing anything?

Before submitting a dispute:

- Review all three credit reports.

- Verify the information being reported.

- Gather supporting documentation.

- Read any previous dispute comments.

- Understand why you’re disputing the account.

Preparation often matters as much as the dispute itself.

When should I consider professional help?

If you’ve already tried repairing your credit yourself and aren’t making progress—or your report contains multiple negative accounts, prior dispute history, or complicated reporting issues—it may be beneficial to have your credit profile reviewed by an experienced professional.

Key Takeaways

Before you send another dispute letter, remember these important points:

✔ You have the legal right to dispute inaccurate or incomplete information.

✔ Every credit report is different.

✔ Generic dispute templates don’t address every situation.

✔ Previous dispute history matters.

✔ More disputes don’t automatically produce better results.

✔ Strong credit isn’t built only by removing negatives—it also requires responsible credit habits.

✔ Understanding the facts behind each account is often more valuable than sending another template.

Final Thoughts

DIY credit repair has helped many consumers correct errors on their credit reports and better understand how credit reporting works. Taking an active role in your financial future is something to be encouraged.

However, one of the biggest misconceptions in the credit repair industry is believing that every negative account can be addressed using the same dispute letter or automated process.

After reviewing thousands of consumer credit reports, we’ve learned that the most effective strategies begin with understanding the entire credit picture—not just the negative account.

Previous dispute history, reporting consistency, account documentation, payment history, and investigation outcomes all provide valuable context. Those details often help determine what the most appropriate next step may be.

Whether you decide to repair your own credit or seek professional assistance, the goal should always be the same:

Make informed decisions based on facts—not assumptions or one-size-fits-all templates.

At Masters Credit Consultants, we believe that education is the foundation of successful credit improvement. We strive to help consumers understand not only what is on their credit report, but also why it is there and how to develop a thoughtful strategy for moving forward.

Take Control of Your Financial Future Today

Don’t let credit issues hold you back from achieving your financial goals.

If you’ve already tried DIY credit repair—or simply want a professional review before submitting another dispute—our experienced credit specialists are here to help you better understand your credit profile and discuss your available options.

📞 Phone: 1-844-620-8796

🌐 Website: https://www.masterscredit.com

📅 Schedule Your Free Consultation:

https://masterscreditconsultantsfreeconsultationbooknow.as.me/schedule/912546ad/appointment/31582691/calendar/6643355

Additional Helpful Links

- Credit Repair Atlanta: Rejected Again? Here’s Why

- Southwest Credit Systems Dispute Guide for 2026: How to Protect Your Credit Score

- Credit Repair Services: The First Step Toward Approval

- Credit repair in Miami: Secrets to Boost Score Fast (2026 Guide)

Related Questions

- What is DIY credit repair?

- Will credit repair services hurt my credit score?

- Which strategies can help you avoid the consequences of wrongfully pulling a customer’s credit report?

- How to clear my credit score?

- How to improve credit score if you have no debt?

- How to increase credit score quickly?

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment