Everything You Need To Know About Credit Utilization Ratios

Credit utilization ratios are one of the most important factors in your credit score. They’re a measure of how much of your available credit you’re using, and they have a big impact on your credit score.

We have a new location: Credit repair Chicago IL is now open!

Here’s everything you need to know about credit utilization ratios:

What Is A Credit Utilization Ratio?

A credit utilization ratio is a measure of how much of your available credit you’re using. It’s calculated by dividing your total outstanding debt by your available credit.

For example, if you have $1,000 in outstanding debt and $10,000 in available credit, your credit utilization ratio would be 10%.

What Is A Good Credit Utilization Ratio?

Ideally, you want to keep your credit utilization ratio below 30%. That means you’re using less than 30% of your available credit, which is a good sign to creditors that you’re a responsible borrower.

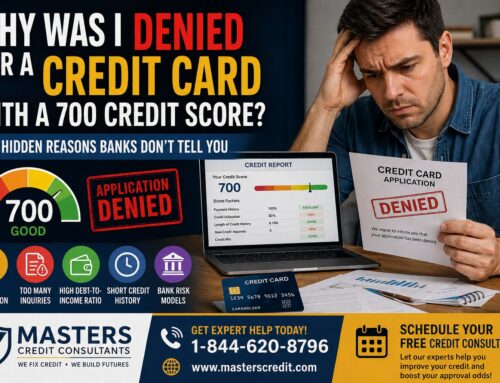

How Does Credit Utilization Affect My Credit Score?

Your credit utilization ratio is one of the most important factors in your credit score. It makes up 30% of your FICO Score, which is the most popular type of credit score.

A high credit utilization ratio can hurt your credit score because it indicates to creditors that you’re using a lot of your available credit.

This can be a sign that you’re struggling to manage your debt, and it can make it more difficult for you to get approved for new loans or lines of credit.

How Can I Lower My Credit Utilization Ratio?

There are a few things you can do to lower your credit utilization ratio:

Pay down your debt: This is the most obvious way to lower your credit utilization ratio. If you can pay off some of your outstanding debt, it will reduce the amount that’s being divided by your total available credit, and lower your ratio.

Request a credit limit increase: Another way to lower your credit utilization ratio is to request a credit limit increase from your creditors. If your credit limits are increased, it will increase the denominator in the equation, and lower your ratio.

Keep balances on multiple cards: If you have multiple credit cards, you can keep balances on each of them to lower your overall credit utilization ratio.

This is because the total amount of debt divided by the number of cards you have will be less than if you had the same balance on just one card.

What Else Do I Need To Know About Credit Utilization Ratios?

There are a few other things to keep in mind when it comes to credit utilization ratios:

They’re just one factor in your credit score: While credit utilization ratios are essential, they’re just one factor that’s considered when calculating your credit score. Other factors, such as payment history and credit history, are also important.

You don’t need to pay off your balances every month: There’s a common misconception that you need to pay off your balances in full every month to avoid harming your credit score.

However, this isn’t the case. As long as you make your payments on time and keep your balances below 30% of your credit limits, you’ll be in good shape.

Utilization ratios can fluctuate: Your credit utilization ratio can fluctuate from month to month, depending on how much debt you’re carrying and what your credit limits are. That’s why it’s important to keep an eye on your ratios and work on lowering them if they start to creep up.

Your credit utilization ratio is an important factor in your credit score, which you should keep an eye on. By paying down your debt and keeping your balances low, you can help to improve your credit score and make it easier to get approved for loans and lines of credit.

Take action now! Fix your credit to get the houses, cars, apartments, or credit cards you truly deserve. When you successfully do credit repair, you level up your life! Contact us today for easy and fast credit repair. Masters Credit Consultants is here to help you now.

[wpi_designer_button slide_id=6350]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment