Ultimate Guide to Credit Repair: A Proven Blueprint to Rebuild Your Credit and Create More Financial Opportunities

Credit repair is the process of improving the accuracy, health, and strength of your credit profile so you can qualify for better financial opportunities. While no legitimate company can guarantee a specific credit score, correcting inaccurate information, reducing debt responsibly, and building positive financial habits can significantly improve your long-term creditworthiness.

In This Article You’ll Learn

- How bad credit silently costs thousands of dollars and how to stop it.

- A step-by-step blueprint to rebuild your credit with confidence.

- How to choose the best credit repair strategy based on your financial goals.

Table of Contents

- Why This Ultimate Guide Is Different

- Why Bad Credit Costs More Than You Think

- Understanding How Credit Really Works

- What Makes Up Your Credit Score?

- The Credit Repair Roadmap

- The Biggest Credit Repair Mistakes

- DIY vs Professional Credit Repair

- Credit Repair for Homebuyers

- Credit Repair for Entrepreneurs

- How to Choose a Credit Repair Company

- 90-Day Credit Improvement Plan

- Frequently Asked Questions

- Final Thoughts

Why This Ultimate Guide Is Different

Search for “Ultimate Guide to Credit Repair”, and you’ll find hundreds of articles explaining what credit repair is. Most cover the same basic topics, repeat the same advice, and leave readers with more questions than answers.

This guide takes a different approach.

Instead of simply defining credit repair, it explains how credit works, why many consumers struggle to improve their scores, and what practical strategies can help you create lasting financial progress.

Whether you’re preparing to buy a home, finance a vehicle, qualify for business funding, or simply improve your financial health, this guide is designed to help you make smarter decisions based on facts—not myths.

Throughout this article, you’ll find comparison tables, expert insights, practical checklists, and easy-to-understand visual roadmaps that simplify even the most complex credit concepts.

Improving your credit isn’t about chasing the highest possible score. It’s about building a credit profile that lenders view as stable, trustworthy, and financially responsible. A strategic plan almost always produces better long-term results than reacting to individual negative accounts one at a time.

Why Bad Credit Costs More Than You Think

Most people associate bad credit with loan denials.

In reality, that’s only part of the story.

Poor credit quietly increases the cost of everyday life. It affects the interest you pay, the financing options available to you, and even the opportunities you can pursue as a homeowner, entrepreneur, or investor.

Imagine two individuals purchasing the exact same vehicle.

Both qualify for financing.

However, one has excellent credit while the other has a lower credit score.

Although they drive away in identical vehicles, the borrower with stronger credit may pay substantially less in total interest over the life of the loan.

The same principle applies to mortgages, personal loans, credit cards, and business financing.

How Poor Credit Can Affect Your Financial Life

| Financial Goal | Strong Credit | Poor Credit |

|---|---|---|

| Buying a Home | Better interest rates | Higher monthly payments |

| Auto Financing | Lower loan costs | Higher financing charges |

| Credit Cards | Better rewards and lower APRs | Higher interest rates |

| Apartment Rental | Easier approval | Larger deposits may be required |

| Business Funding | More financing options | Limited lender choices |

| Insurance (where applicable) | Potentially lower premiums | Potentially higher costs |

The financial impact extends beyond borrowing money.

Many business owners discover that their personal credit history influences their ability to secure startup funding, commercial financing, or equipment loans.

Improving your credit isn’t just about repairing the past.

It’s about creating more affordable opportunities for your future.

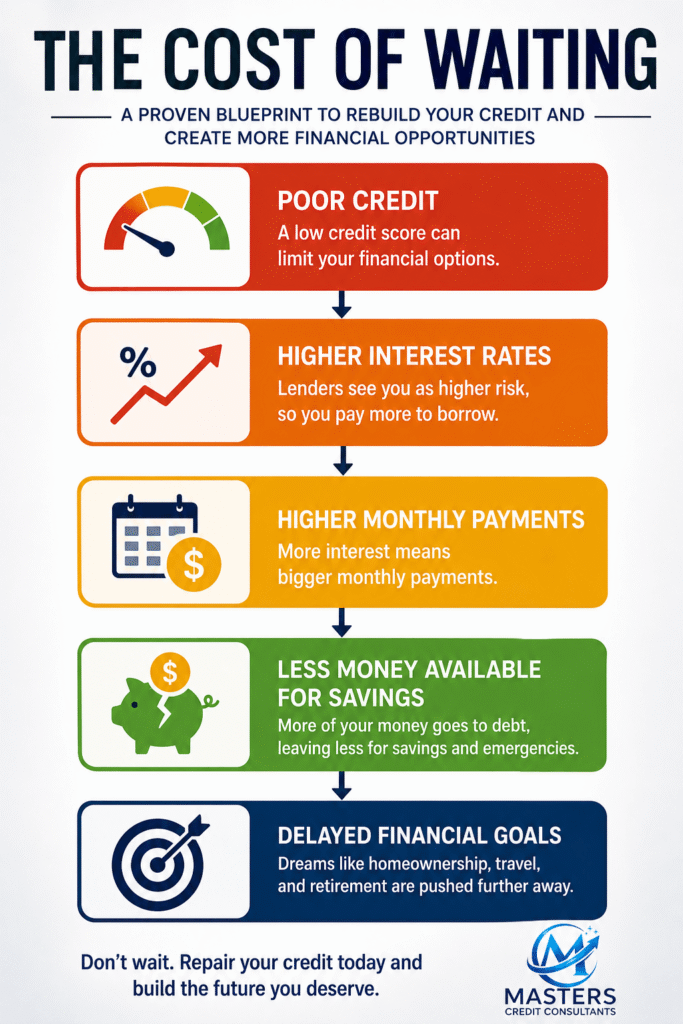

The Cost of Waiting: Discover how poor credit increases borrowing costs, reduces savings, and delays major financial milestones—and why rebuilding your credit sooner can save you thousands.

Understanding How Credit Really Works

One of the biggest misconceptions about credit repair is believing that your credit score is created by one company.

It isn’t.

Your credit profile is built from information shared by lenders, organized by credit bureaus, and evaluated by future lenders whenever you apply for financing.

Understanding this system helps explain why successful credit repair involves much more than submitting dispute letters.

The Credit Ecosystem

The Credit Ecosystem: Learn how your financial activity flows through the credit system—from lenders to credit bureaus, credit reports, and credit scores—and how it influences loans, housing, insurance, and financial opportunities.

Every organization has a different responsibility.

Creditors

Banks, credit unions, finance companies, mortgage lenders, and credit card issuers report information about your accounts.

This information includes:

- Payment history

- Account balances

- Credit limits

- Account status

- Delinquencies

- Charge-offs

If inaccurate information is reported, it may affect your credit profile until corrected.

Credit Bureaus

Credit bureaus collect information reported by creditors and organize it into credit reports.

These reports become one of the primary resources lenders use when evaluating loan applications.

Credit bureaus don’t decide whether you’re approved.

They simply organize and distribute information.

Collection Agencies

Unpaid debts may eventually be transferred or sold to collection agencies.

Collection accounts can significantly influence lending decisions, making it important to review them carefully for reporting accuracy.

Lenders

Every lender has different approval criteria.

Mortgage lenders often emphasize payment history.

Auto lenders may focus more heavily on recent payment behavior.

Business lenders frequently review both personal and business credit before approving financing.

Understanding these differences helps you develop a smarter credit improvement strategy.

Two lenders reviewing the exact same credit report may reach different lending decisions because each institution uses its own underwriting guidelines and evaluates risk differently.

What Makes Up Your Credit Score?

Many consumers focus entirely on the final score without understanding the factors behind it.

Your score is influenced by several key components, each carrying a different level of importance.

Payment history generally carries the greatest influence because lenders want evidence that you consistently repay borrowed money.

Credit utilization—the percentage of available revolving credit you’re using—is another major factor.

High balances may negatively affect your score even if you’re making every payment on time.

Credit Score Breakdown

Credit Score Ranges

| Credit Score | Rating | Typical Lending Outlook |

|---|---|---|

| 800–850 | Exceptional | Best financing opportunities |

| 740–799 | Very Good | Excellent approval potential |

| 670–739 | Good | Competitive lending options |

| 580–669 | Fair | Higher borrowing costs |

| 300–579 | Poor | Limited financing options |

Your goal shouldn’t necessarily be an 850 credit score.

Instead, focus on building a healthy, sustainable credit profile that supports your financial goals.

Many borrowers become eligible for significantly better financing before reaching a perfect credit score. Strategic improvement often matters more than perfection.

Myth vs. Fact

There’s no shortage of misinformation about credit repair.

Let’s separate fact from fiction.

| Myth | Fact |

|---|---|

| Paying every collection immediately raises your score. | It depends on the scoring model and your overall credit profile. |

| Credit repair is illegal. | Credit repair is legal when conducted ethically and within consumer protection laws. |

| You need an 850 score to qualify for loans. | Many lenders approve qualified borrowers with much lower scores. |

| Checking your own credit lowers your score. | Reviewing your own credit is generally considered a soft inquiry and does not lower your score. |

| Credit repair happens overnight. | Meaningful improvement usually requires consistency, patience, and a strategic plan. |

One of the biggest mistakes consumers make is believing there is a single shortcut to better credit.

There isn’t.

Successful credit improvement combines accurate reporting, responsible borrowing, smart financial planning, and consistent positive habits.

The Credit Repair Roadmap

There isn’t a magic formula for improving your credit.

There is, however, a proven process.

Many people become overwhelmed because they try to fix everything at once. They dispute every account, close old credit cards, pay off debts in the wrong order, or apply for new credit hoping for a quick score increase. These actions often create more problems than they solve.

The most effective credit repair strategy is systematic. Each step builds on the previous one, creating a stronger and healthier credit profile over time.

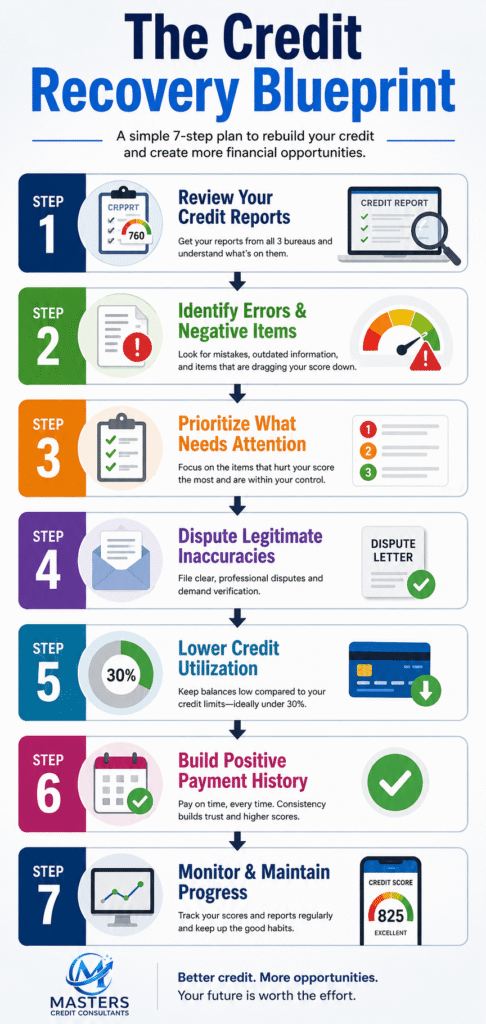

The Credit Recovery Blueprint: Follow this proven 7-step credit repair strategy to improve your credit score, strengthen your financial health, and unlock better lending opportunities.

Think of this roadmap as a long-term financial improvement plan rather than a quick fix. Every positive decision you make today helps strengthen your financial future tomorrow.

Step 1: Review Your Credit Reports Carefully

Before making any changes, understand exactly where you stand.

Many consumers only check their credit score and never review the report behind it. However, your score is simply the outcome of the information contained in your credit report.

Review each report carefully and verify:

- Personal information

- Current and previous addresses

- Employment information

- Open accounts

- Closed accounts

- Payment history

- Collection accounts

- Public records

- Hard inquiries

- Credit limits and balances

Don’t assume every entry is correct.

Even small reporting errors may influence lending decisions.

One inaccurate late payment reported on a long-standing account can have a greater impact than many consumers realize. Reviewing your reports line by line is one of the most valuable steps in the credit repair process.

Step 2: Identify Reporting Errors

Not every negative item should automatically be disputed.

Instead, determine whether the information is complete, accurate, and properly reported.

Examples of information that deserves closer review include:

| Potential Reporting Issue | Why It Matters |

|---|---|

| Incorrect late payments | May negatively affect payment history. |

| Duplicate accounts | Can make debt appear larger than it actually is. |

| Incorrect balances | May increase credit utilization. |

| Accounts that aren’t yours | May indicate reporting mistakes or identity theft. |

| Incorrect personal information | Can create confusion during credit reporting. |

| Outdated information | May no longer belong on your credit report under applicable reporting rules. |

Taking the time to verify your credit report before acting helps you avoid unnecessary disputes and develop a more effective strategy.

Step 3: Prioritize Your Credit Goals

Not every consumer has the same objective.

Someone planning to purchase a home within six months will likely need a different strategy than someone rebuilding after financial hardship.

Ask yourself:

- Are you preparing to buy a home?

- Do you need financing for a vehicle?

- Are you planning to start a business?

- Do you want to qualify for better credit cards?

- Are you trying to reduce interest costs?

Your financial goals should determine where you focus your attention first.

Goal-Based Credit Strategy

| Your Goal | Primary Focus |

|---|---|

| Buying a Home | Payment history and debt reduction |

| Auto Financing | Lower credit utilization and maintain a stable payment history |

| Business Funding | Build strong personal credit and keep revolving debt low |

| Credit Card Approval | Improve credit utilization and reduce recent credit inquiries |

| Financial Recovery | Create a budget, make on-time payments, and monitor your credit regularly |

Step 4: Build Positive Credit Habits

Credit repair isn’t only about correcting mistakes.

It’s equally important to demonstrate responsible financial behavior moving forward.

Successful borrowers consistently practice habits that strengthen their financial profile.

Daily Credit Success Checklist

☐ Pay every bill before the due date.

☐ Keep revolving balances as low as possible.

☐ Avoid applying for unnecessary credit.

☐ Review your monthly statements.

☐ Monitor your credit reports regularly.

☐ Build an emergency savings fund.

☐ Create and follow a realistic budget.

These habits may seem simple, but they form the foundation of excellent credit.

Payment history is generally considered the most influential factor in many credit scoring models. Even one missed payment can remain on your credit report for years, making consistent on-time payments one of the most powerful ways to strengthen your credit profile.

The 15 Biggest Credit Repair Mistakes Consumers Make

Many consumers unintentionally delay their own progress.

Avoiding these common mistakes can save both time and money.

| Mistake | Better Strategy |

|---|---|

| Waiting until you need a loan | Monitor your credit year-round. |

| Ignoring your credit reports | Review them regularly. |

| Closing old credit cards | Consider the impact on your credit age before closing accounts. |

| Maxing out credit cards | Keep your credit utilization low. |

| Applying for multiple loans at once | Apply only when necessary. |

| Believing every online “credit hack” | Follow trusted financial guidance. |

| Missing payment due dates | Automate payments whenever possible. |

| Ignoring budgeting | Build a spending plan based on your income. |

| Paying collections without a strategy | Understand your options before making payments. |

| Forgetting emergency savings | Set aside funds for unexpected expenses. |

| Co-signing loans without understanding the risks | Evaluate the long-term responsibility before agreeing. |

| Ignoring identity theft warning signs | Monitor your accounts and credit reports consistently. |

| Focusing only on the score | Improve your overall credit profile and financial habits. |

| Expecting overnight results | Take a long-term approach to credit improvement. |

| Giving up too early | Stay consistent, patient, and committed to your plan. |

The Biggest Mistake Consumers Make

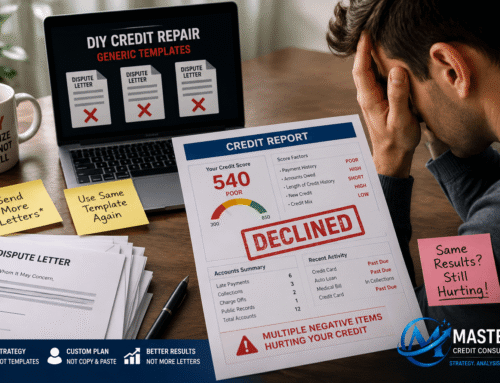

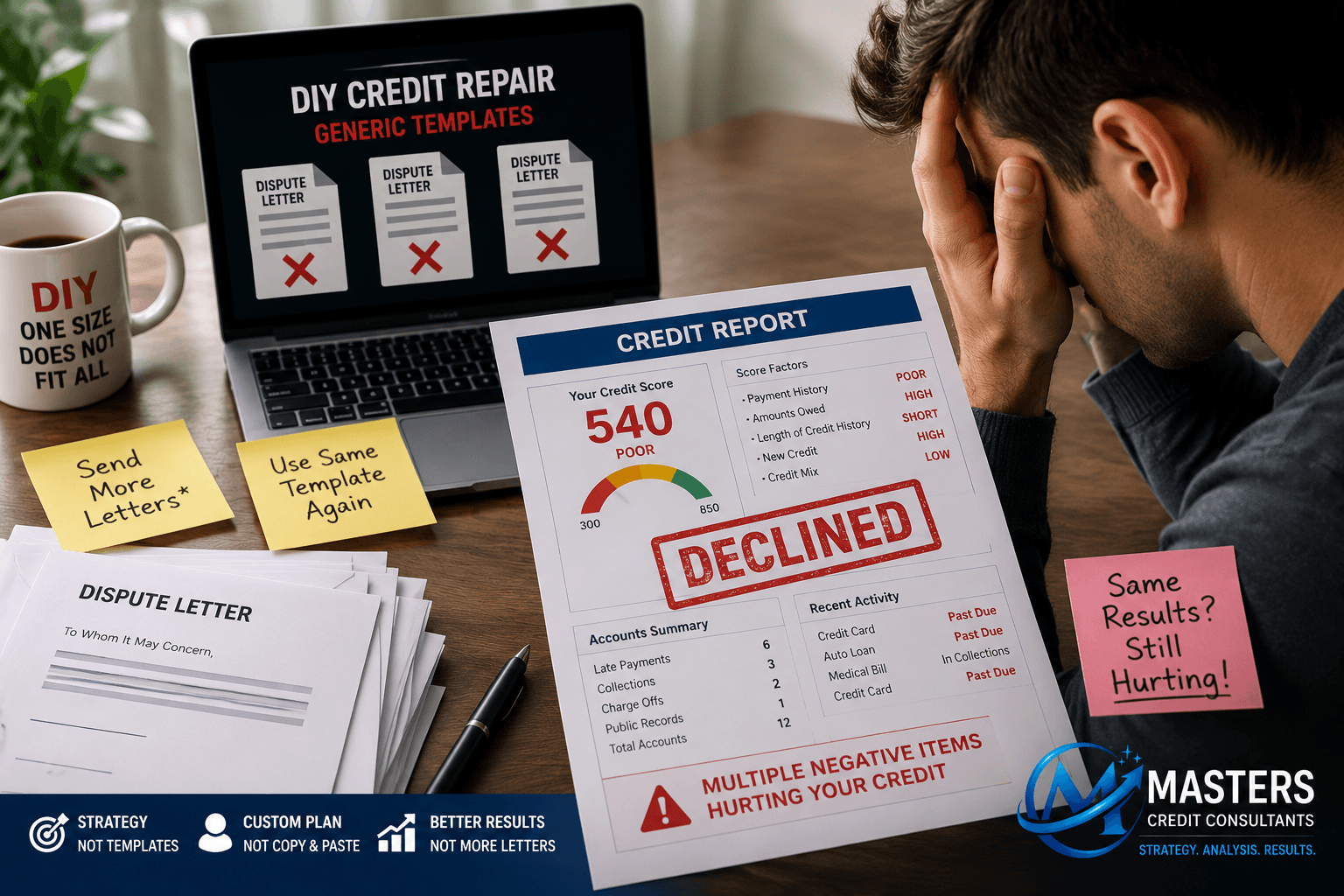

Many people believe that if one dispute letter doesn’t work, sending five more identical letters will eventually produce a different outcome.

In many cases, that simply isn’t how the investigation process works.

Effective credit repair isn’t about the number of disputes sent.

It’s about understanding why an account is being disputed, what supports the dispute, and whether a different strategy is appropriate based on the account’s history.

DIY Credit Repair vs. Professional Credit Repair Services

One of the most common questions people ask is whether they should repair their credit on their own or work with professionals.

The answer depends on your situation.

If your credit history is relatively simple and you have time to learn the process, a DIY approach may work well.

However, more complex situations often benefit from experienced guidance.

| DIY Credit Repair | Professional Credit Repair Services |

|---|---|

| Lower upfront cost | Personalized credit strategy |

| Requires extensive research | Saves time and effort |

| Self-managed documentation | Professional organization and guidance |

| Best for simple credit situations | Helpful for complex credit histories |

| Limited support | Ongoing education and progress reviews |

There is no universally correct choice.

The best approach depends on your financial goals, available time, and confidence in navigating the credit repair process.

Professional credit repair should never replace responsible financial habits. Instead, it should complement them by providing education, organization, and a personalized strategy that supports your long-term financial success.

Credit Repair for Every Stage of Life

One of the biggest misconceptions about credit repair is that it’s only for people with poor credit.

In reality, credit improvement is beneficial for anyone preparing for a major financial milestone. Whether you’re buying your first home, starting a business, rebuilding after a financial setback, or planning for retirement, a healthier credit profile can create more opportunities and reduce borrowing costs.

The key is understanding how your credit aligns with your goals.

Credit Repair for First-Time Homebuyers

Buying a home is one of the largest financial decisions most people will ever make.

Even a modest improvement in your credit profile may help you qualify for:

- More competitive mortgage interest rates

- Lower monthly mortgage payments

- Better loan options

- Reduced borrowing costs over the life of the loan

Homebuyer Credit Checklist

Before applying for a mortgage:

☐ Review all three credit reports.

☐ Verify your personal information.

☐ Correct legitimate reporting inaccuracies.

☐ Reduce revolving credit card balances.

☐ Avoid opening new credit accounts.

☐ Continue making every payment on time.

☐ Avoid large unexplained deposits or new debt before closing.

Don’t wait until you’ve found your dream home to check your credit. Preparing six to twelve months in advance gives you more time to strengthen your credit profile before lenders evaluate your application.

Credit Repair for Entrepreneurs

Entrepreneurs often focus on business plans, marketing, and financing while overlooking one critical factor—personal credit.

Many lenders review your personal credit history before approving:

- Startup financing

- SBA loans

- Business credit cards

- Equipment financing

- Commercial vehicle loans

- Business lines of credit

For many new businesses, personal credit serves as the foundation for establishing business credit.

Personal Credit vs. Business Credit

| Personal Credit | Business Credit |

|---|---|

| Based on your personal borrowing history | Based on your company’s financial history |

| Used for many startup financing decisions | Used as your business grows |

| May require a personal guarantee | May eventually stand on its own |

| Impacts personal lending opportunities | Supports business financing and vendor relationships |

Strong personal credit can help entrepreneurs access financing that supports expansion, hiring, inventory purchases, and equipment investments.

Credit Repair After Financial Hardship

Life doesn’t always go according to plan.

Medical emergencies, unexpected job loss, divorce, natural disasters, or economic downturns can disrupt even the healthiest financial situations.

The important thing to remember is that financial setbacks do not define your future.

A structured recovery plan may include:

- Creating a realistic monthly budget.

- Bringing delinquent accounts current when possible.

- Reviewing reports for inaccuracies.

- Reducing revolving debt.

- Building emergency savings.

- Monitoring progress consistently.

The sooner you begin rebuilding, the sooner you create opportunities for future financial success.

Credit Repair After Identity Theft

Identity theft can damage your credit profile even when you’ve done nothing wrong.

Common warning signs include:

- Accounts you don’t recognize.

- Unexpected hard inquiries.

- Incorrect addresses.

- Unknown employers listed on your report.

- Collection accounts that don’t belong to you.

If you suspect identity theft:

- Review all three credit reports.

- Contact affected financial institutions.

- Report fraudulent activity to the appropriate authorities.

- Consider placing a fraud alert or security freeze where appropriate.

- Keep detailed records of every communication.

Early action may help reduce long-term financial damage.

Credit Repair for Military Families

Military families often experience frequent relocations, deployments, and unique financial challenges.

Maintaining healthy credit can make it easier to:

- Purchase a home.

- Finance reliable transportation.

- Qualify for favorable lending terms.

- Prepare for civilian career transitions.

Consistently monitoring your credit while keeping personal information updated can help prevent reporting issues during frequent moves.

Credit Repair for Young Professionals

Your first few years in the workforce establish many of the financial habits that will influence your future.

Good credit can help you:

- Rent your first apartment.

- Purchase a reliable vehicle.

- Obtain lower-interest credit cards.

- Build savings.

- Prepare for homeownership.

Simple habits such as paying every bill on time and avoiding excessive credit card balances can make a significant difference over time.

Credit Repair for Families

Families often balance multiple financial priorities at once.

Mortgage payments.

Childcare.

Education expenses.

Healthcare.

Emergency savings.

Strong credit provides flexibility during these important life stages by improving access to affordable financing when it’s genuinely needed.

When Professional Credit Repair Services May Be Worth Considering

Not every credit situation requires professional assistance.

However, there are circumstances where experienced guidance may help simplify the process.

You may benefit from professional credit repair services if you:

- Have multiple collection accounts.

- Are preparing to buy a home soon.

- Have experienced identity theft.

- Need to organize a complex credit history.

- Are seeking business financing.

- Feel overwhelmed by the dispute process.

Professional guidance should never replace responsible financial habits.

Instead, it should support them through education, organization, and personalized recommendations.

Decision Matrix: Should You Handle Credit Repair Yourself?

| Situation | DIY | Professional Guidance |

|---|---|---|

| One reporting error | ✔ | — |

| Multiple collection accounts | — | ✔ |

| Identity theft | — | ✔ |

| Mortgage preparation | — | ✔ |

| Building business credit | — | ✔ |

| Minor balance corrections | ✔ | — |

| Complex credit history | — | ✔ |

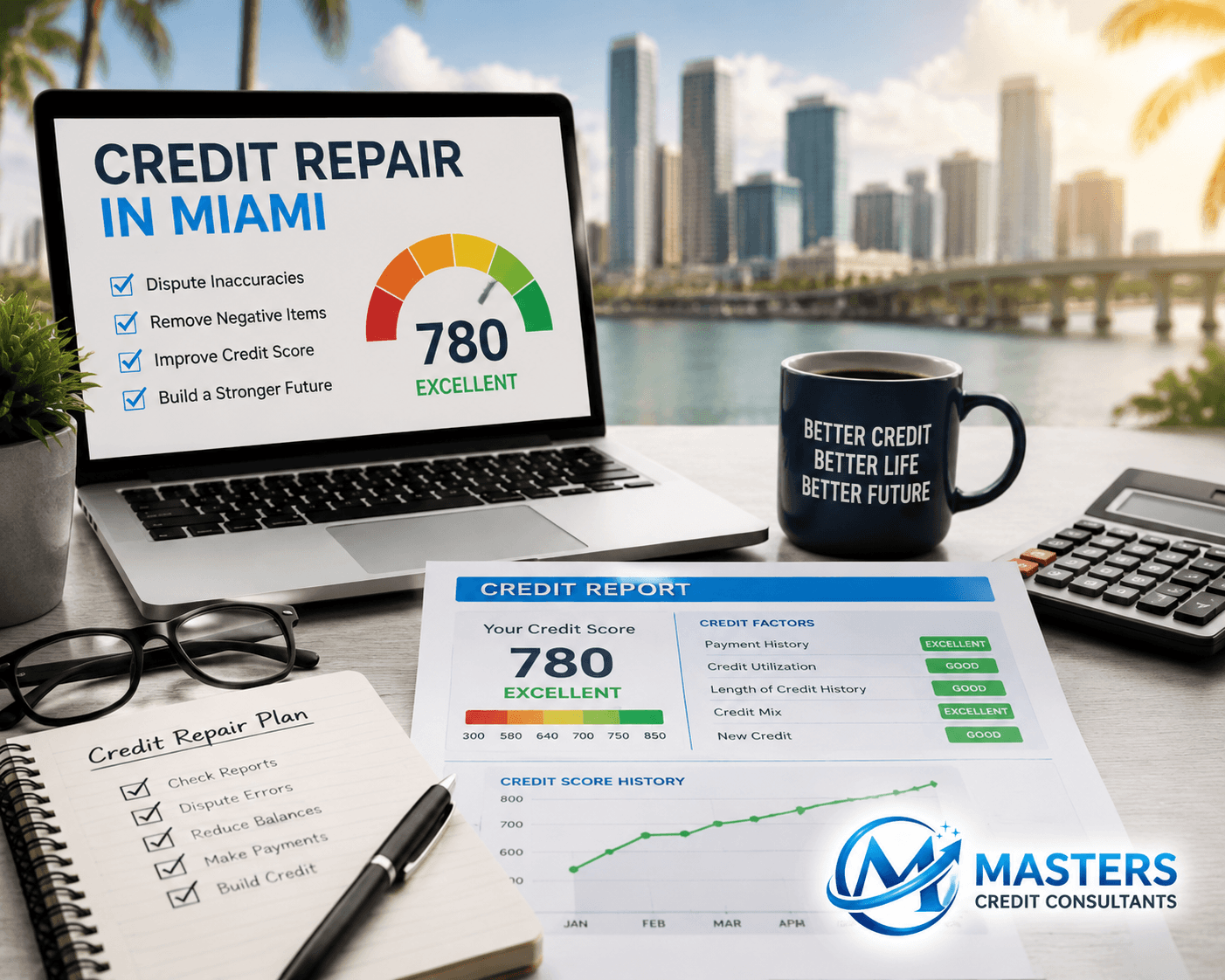

How to Choose the Right Credit Repair Company

Searching online for credit repair near me, credit repair services near me, or credit repair agencies can produce hundreds of results.

Choosing the right company requires more than reading advertisements.

Look for a company that values education, transparency, and realistic expectations.

Questions Every Consumer Should Ask

✔ How will my credit reports be reviewed?

✔ Will I receive a personalized strategy?

✔ How will progress be communicated?

✔ What services are included?

✔ Are fees clearly explained?

✔ Does the company educate clients throughout the process?

Warning Signs

Be cautious if a company:

- Guarantees a specific credit score.

- Promises overnight results.

- Claims it can legally remove every negative item.

- Pressures you into making an immediate decision.

- Avoids explaining its process.

Ethical credit repair focuses on improving reporting accuracy, strengthening financial habits, and helping consumers understand their rights. Be cautious of unrealistic promises or guarantees.

Looking for Credit Repair Services Near You?

Whether you’re searching for credit repair near me, credit repair services, credit repair company near me, or Credit Repair Miami, the most important factor is choosing a company that prioritizes education, personalized strategies, and long-term financial success.

Improving your credit isn’t about finding a shortcut.

It’s about finding the right strategy.

A trusted credit professional can help you understand where you are today, where you want to go, and the practical steps that may help you get there.

Your 90-Day Credit Improvement Action Plan

One of the biggest misconceptions about credit repair is that it requires years before you see progress. While every credit profile is different, the actions you take during the first 90 days can lay the foundation for meaningful long-term improvement.

Think of this plan as a roadmap rather than a race. The objective isn’t to create a perfect credit score overnight. It’s to build consistent financial habits that lenders value.

Month 1: Understand Your Credit Profile

Before making changes, understand exactly where you stand.

During the first 30 days, your priority should be education and organization.

Week 1: Obtain Your Credit Reports

Request and review your credit reports carefully.

Look for:

- Incorrect personal information

- Accounts that don’t belong to you

- Duplicate accounts

- Incorrect payment history

- Incorrect balances

- Collection accounts

- Charge-offs

- Hard inquiries you don’t recognize

Your credit score only tells you the result. Your credit report tells you the story behind the score. Always review the report—not just the number.

Week 2: Organize Your Finances

Create a complete picture of your financial situation.

Document:

- Monthly income

- Monthly expenses

- Outstanding debts

- Minimum payments

- Interest rates

- Savings

- Financial goals

This information will help you prioritize which accounts deserve immediate attention.

Week 3: Build Your Budget

A successful credit repair strategy begins with a realistic spending plan.

Focus on:

✔ Paying every bill on time

✔ Eliminating unnecessary expenses

✔ Increasing available cash flow

✔ Building emergency savings

Even small improvements create momentum.

Week 4: Prioritize High-Impact Actions

Not every account affects your financial goals equally.

Focus first on:

- High credit card balances

- Recently delinquent accounts

- Accounts with inaccurate reporting

- Upcoming loan applications

Month 1 Progress Tracker

| Task | Status |

|---|---|

| Reviewed all credit reports | ☐ |

| Organized financial records | ☐ |

| Created a monthly budget | ☐ |

| Identified reporting concerns | ☐ |

| Listed financial goals | ☐ |

Month 2: Strengthen Your Credit Profile

Once you’ve identified your priorities, begin strengthening your overall credit profile.

Week 5–6

Focus on reducing revolving balances whenever possible.

Lower utilization often has a meaningful impact on your overall credit profile.

Avoid:

- Maxing out credit cards

- Opening unnecessary accounts

- Missing payment due dates

Week 7

Review any changes to your credit reports.

Continue documenting your progress.

Ask yourself:

- Are balances decreasing?

- Have inaccurate items been addressed?

- Am I consistently paying on time?

Consistency matters more than speed.

Week 8

Evaluate your financial goals.

Are you preparing to:

- Purchase a home?

- Buy a vehicle?

- Start a business?

- Qualify for business funding?

Your credit improvement strategy should always align with your next financial objective.

Month 2 Success Checklist

☐ Lowered revolving balances

☐ Continued on-time payments

☐ Reviewed credit reports

☐ Avoided unnecessary credit applications

☐ Updated financial goals

Month 3: Build Long-Term Momentum

By now, you’ve created the foundation.

Now it’s time to strengthen it.

Continue:

- Paying every account on time

- Keeping utilization low

- Monitoring your reports

- Building emergency savings

- Reviewing your budget monthly

Remember:

Healthy credit isn’t built through one good month.

It’s built through years of responsible financial decisions.

Your Credit Improvement Journey

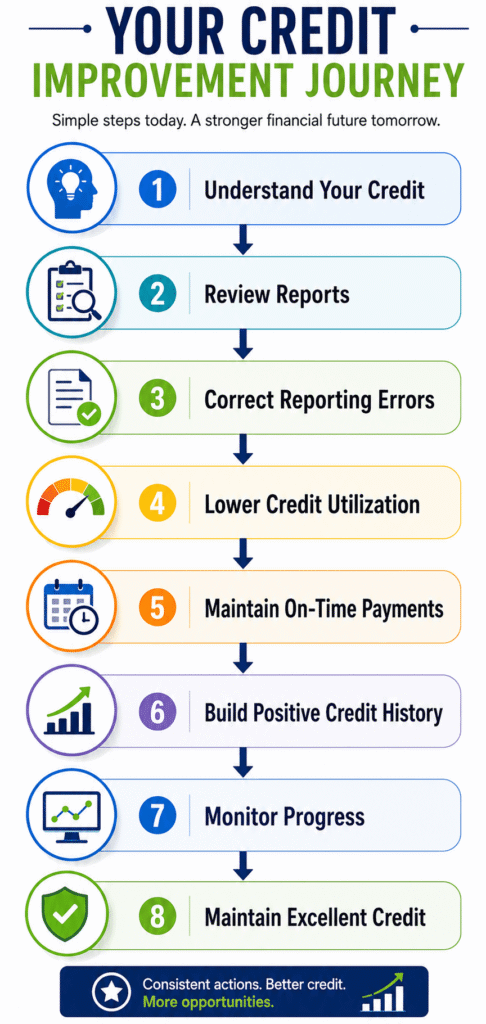

Your Credit Improvement Journey: Follow these eight practical steps to build stronger credit, improve your financial health, and unlock more lending and financial opportunities.

Frequently Asked Questions (People Also Ask)

Does credit repair really work?

Yes—when it’s based on accurate information, responsible financial habits, and a realistic strategy. Credit repair isn’t about removing truthful information; it’s about correcting inaccuracies, improving financial behaviors, and strengthening your overall credit profile over time.

How long does credit repair usually take?

Every situation is unique. Some consumers notice improvements within a few months, while more complex credit histories may require additional time. Factors such as payment history, debt levels, reporting accuracy, and financial habits all influence the timeline.

Can I repair my credit myself?

Yes. Many people successfully improve their credit independently by reviewing their reports, correcting legitimate reporting errors, reducing debt, and consistently making on-time payments. Others prefer professional guidance for more complex situations.

What is the fastest way to improve a credit score?

There is no guaranteed shortcut. However, consistently making on-time payments, reducing credit card balances, correcting reporting inaccuracies, and avoiding unnecessary new credit are among the most effective ways to improve your credit profile.

Is professional credit repair worth it?

For consumers with complicated credit histories, multiple collection accounts, identity theft concerns, or limited time, professional guidance may provide organization, education, and a personalized strategy that supports long-term financial success.

Can paying off debt hurt my credit score?

In some situations, a score may fluctuate temporarily after paying off certain accounts due to changes in credit utilization or account mix. However, reducing debt responsibly is generally beneficial for your long-term financial health.

How often should I check my credit report?

Reviewing your credit reports several times each year—or before applying for major financing—can help you identify reporting inaccuracies and monitor your financial progress.

What’s the difference between credit repair and credit counseling?

Credit repair focuses on reviewing credit reports, addressing reporting inaccuracies, and improving your credit profile. Credit counseling generally emphasizes budgeting, debt management, and financial education.

Final Thoughts: Your Credit Is More Than a Number

Your credit score is important—but it doesn’t tell your entire financial story.

Every on-time payment, every responsible borrowing decision, and every positive financial habit contributes to a stronger future.

Whether your goal is purchasing a home, financing a vehicle, growing a business, or simply reducing financial stress, improving your credit is an investment in yourself.

The most successful consumers don’t look for shortcuts.

They build strategies.

They stay consistent.

And they understand that good credit is the result of good financial habits practiced over time.

At Masters Credit Consultants, the goal isn’t simply to help clients improve a credit score. It’s to help individuals, families, entrepreneurs, and future homeowners create stronger financial foundations through education, personalized strategies, and long-term planning.

Whether you’re looking for Credit Repair Services, Credit Repair Near Me, Credit Repair Services Near Me, Credit Repair Miami, or a trusted credit repair company near me, having the right guidance can make your journey more organized and more effective.

If you’re ready to take the next step toward better financial opportunities, schedule a free consultation and begin building a strategy that’s tailored to your goals—not someone else’s.

🚀 Schedule Your Free Credit Consultation with Masters Credit Consultants

Whether you’re rebuilding after financial hardship, preparing to buy a home, qualifying for business funding, or simply looking to improve your financial future, professional guidance can help you better understand your credit profile and develop a personalized strategy.

📞 Phone: 1-844-620-8796

🌐 Website: https://www.masterscredit.com

📅 Schedule Your Free Consultation

https://www.masterscredit.com/sign-up/

Additional Helpful Links

- DIY Credit Repair May Be Hurting Your Credit: Why Strategy Matters More Than Templates

- Southwest Credit Systems Dispute Guide for 2026: How to Protect Your Credit Score

- Credit Repair Services: The First Step Toward Approval

- Credit repair in Miami: Secrets to Boost Score Fast (2026 Guide)

Related Questions

- What is DIY credit repair?

- Will credit repair services hurt my credit score?

- Which strategies can help you avoid the consequences of wrongfully pulling a customer’s credit report?

- How to clear my credit score?

- How to improve credit score if you have no debt?

- How to increase credit score quickly?

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment