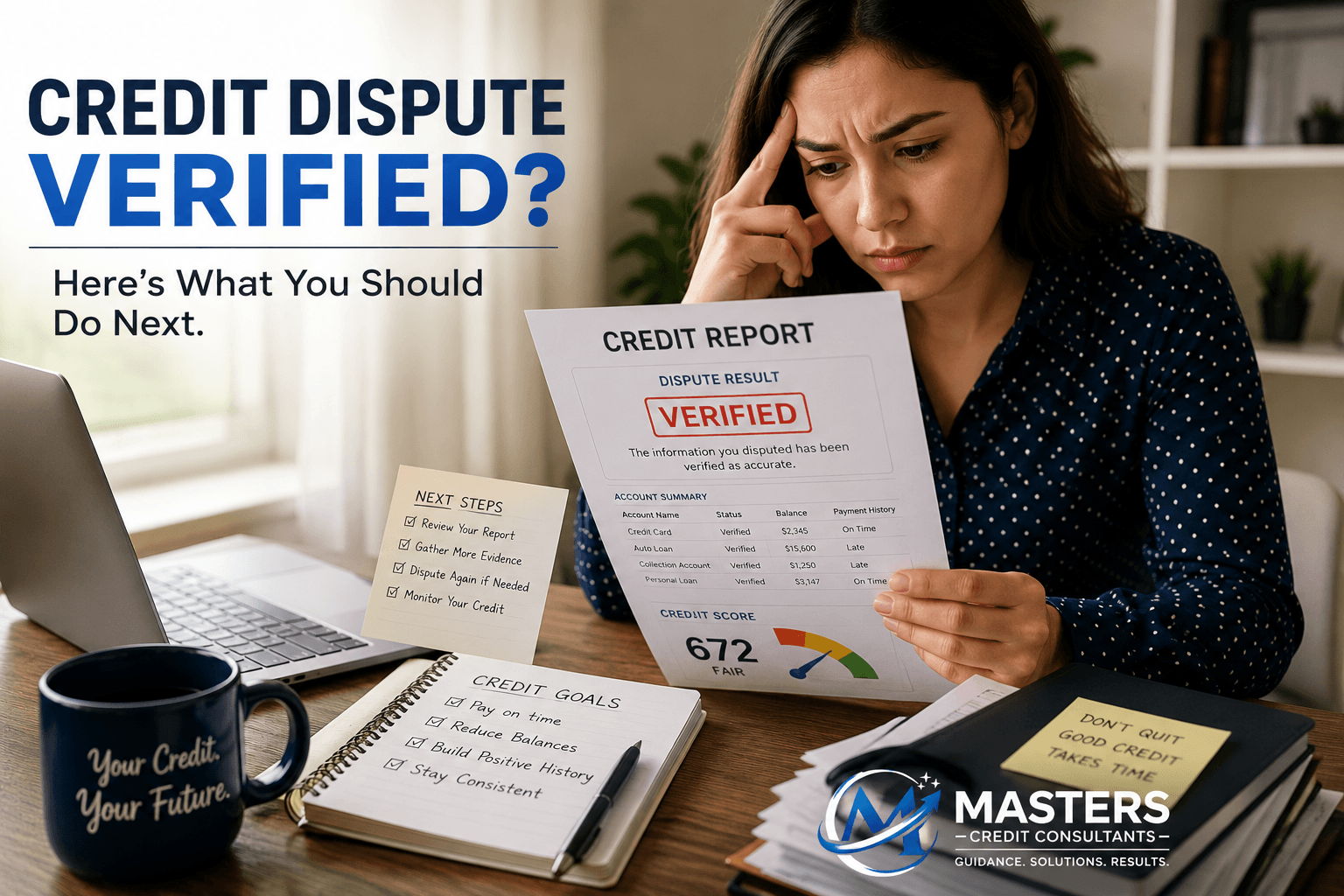

Why Your Credit Dispute Was Verified: Now What?

The Complete Guide to Understanding Verified Credit Disputes and Your Next Steps

If your credit dispute was verified, it means the credit bureau confirmed the disputed information with the creditor or data furnisher. It does not automatically mean the information is accurate. If you have new evidence or believe an error still exists, you may submit another dispute, contact the creditor directly, or seek professional credit repair services to continue challenging inaccurate reporting.

In This Article You’ll Learn

- How the credit dispute verification process works and why disputes get verified.

- What steps you can take if you believe the information is still inaccurate.

- How to build a stronger strategy for improving your credit and protecting your financial future.

Table of Contents

- What Does “Credit Dispute Verified” Really Mean?

- Understanding How the Credit Dispute Process Works

- Why Credit Bureaus Verify Disputed Accounts

- Why Verified Doesn’t Always Mean Accurate

- Common Reasons Credit Disputes Are Verified

- Review Your Credit Report Like an Expert

- Collect Stronger Evidence Before Filing Again

- Know Your Rights Under the FCRA

- Should You File Another Dispute?

- When to Escalate Your Dispute

- Contact the Creditor Directly

- Build Better Credit While Waiting

- Improve Your Credit Utilization

- Common Credit Dispute Mistakes

- When Professional Credit Repair Services Can Help

- Frequently Asked Questions

- Final Thoughts

Credit Dispute Statistics

What Does “Credit Dispute Verified” Really Mean?

Receiving a notification that your credit dispute was verified can be frustrating, especially if you know the account contains incorrect information. Many consumers mistakenly believe this response means the creditor thoroughly investigated every detail of their claim. In reality, that is often not the case.

When a dispute is submitted, the credit bureau contacts the company reporting the account—known as the data furnisher. If the furnisher confirms that its records match what appears on your credit report, the bureau typically marks the account as verified.

This process is largely administrative. It does not always involve reviewing every supporting document you may have submitted or conducting an independent investigation.

Because of this, a verified dispute should not automatically discourage you from taking additional action if the information is inaccurate.

How the Credit Dispute Process Works

Understanding the dispute process helps explain why verification happens so frequently.

Generally, the process follows these steps:

- You identify inaccurate information on your credit report.

- You submit a dispute with one or more credit bureaus.

- The bureau forwards the dispute to the company reporting the account.

- The furnisher reviews its records.

- The bureau updates you with the investigation results.

In many situations, the furnisher simply compares the disputed information with its internal records. If everything appears consistent, the account is verified.

That does not necessarily prove the original information is correct. It simply confirms that the furnisher believes its own records are accurate.

Why Credit Bureaus Verify Disputed Accounts

Credit bureaus process millions of disputes every year. Because of this enormous volume, investigations often rely on automated systems rather than detailed manual reviews.

Several factors contribute to a dispute being verified:

- The creditor confirms the balance.

- The payment history matches its records.

- The account ownership appears correct.

- The dates reported remain unchanged.

- No additional documentation changes the creditor’s position.

This explains why many consumers receive verified results even when they sincerely believe errors exist.

The verification process is designed to determine whether the information matches the furnisher’s records—not necessarily whether those records are completely accurate.

Common Reasons a Credit Dispute Gets Verified

Several common situations lead to verified disputes.

The Creditor Never Received Enough Evidence

Submitting a dispute with only a brief explanation often limits what the investigator can review.

Instead of saying,

“This account is wrong.”

Provide documentation such as:

- Payment confirmations

- Bank statements

- Settlement agreements

- Identity theft reports

- Court documents

- Account closure letters

Specific evidence gives investigators more context and may increase the likelihood of a different outcome during a future investigation.

The Information Actually Matches the Creditor’s Records

Sometimes the reported information is technically correct, even if it feels unfair.

For example:

- A legitimate late payment

- A correctly reported collection account

- An accurate loan balance

- A valid repossession

- A bankruptcy filing

In these cases, disputing factual information is unlikely to result in removal.

Instead, your focus should shift toward rebuilding your credit profile.

The Wrong Type of Dispute Was Filed

Not every dispute addresses the real issue.

For example, disputing an account balance when the actual problem is incorrect payment history may result in verification because the balance itself is accurate.

Carefully identify exactly which element is incorrect before filing another dispute.

The Investigation Was Automated

Many investigations rely on electronic communication systems between credit bureaus and furnishers.

Rather than manually reviewing every document, automated verification compares electronic account records.

Although efficient, automation sometimes overlooks supporting evidence submitted by consumers.

Verification Doesn’t Always Mean Accuracy

One of the biggest misconceptions about credit reporting is that verification equals truth.

It doesn’t.

Credit reporting systems are built on information supplied by lenders, collection agencies, and other financial institutions. Like any large database, mistakes can happen.

Examples include:

- Mixed credit files

- Duplicate accounts

- Incorrect balances

- Identity theft

- Accounts belonging to another individual

- Incorrect payment histories

- Reporting after legal time limits

If inaccurate information remains on your report after verification, you still have the right to challenge it.

Persistence, combined with proper documentation, often produces better results than repeatedly sending the same generic dispute.

Review Your Credit Report Carefully

Before submitting another dispute, carefully analyze your credit report.

Don’t focus only on the account that was verified.

Instead, review every section for potential inaccuracies.

Look for:

- Incorrect personal information

- Misspelled names

- Wrong addresses

- Duplicate accounts

- Incorrect account status

- Wrong payment dates

- Accounts that should have aged off

- Incorrect credit limits

- Unauthorized inquiries

Review Checklist

✅ Personal information

✅ Addresses

✅ Employers

✅ Duplicate accounts

✅ Payment history

✅ Credit limits

✅ Balances

✅ Collection accounts

✅ Public records

✅ Hard inquiries

Many consumers discover multiple reporting errors after taking a closer look.

Correcting several inaccuracies can have a greater long-term impact than focusing on just one account.

Gather Better Supporting Documentation

Strong documentation often separates successful disputes from unsuccessful ones.

The more objective evidence you provide, the easier it becomes to demonstrate inconsistencies.

Helpful documents may include:

- Monthly account statements

- Payment receipts

- Cancelled checks

- Bank transaction history

- Loan payoff letters

- Identity theft affidavits

- Police reports

- Correspondence from lenders

- Settlement agreements

- Collection removal confirmations

Organize your documents before submitting another dispute.

A clear, well-supported dispute is generally more persuasive than a short explanation without evidence.

Keep digital copies of important financial records in a secure folder. Organized documentation can save time whenever you need to dispute inaccurate reporting or verify account history.

Know Your Rights Under Federal Law

Consumers have important protections under the Fair Credit Reporting Act (FCRA).

These protections include the right to:

- Receive accurate credit reporting.

- Dispute inaccurate information.

- Request investigations.

- Receive investigation results.

- Have unverifiable information removed.

- Obtain copies of your credit reports.

Understanding these rights helps you advocate for yourself more effectively throughout the dispute process.

If an investigation appears incomplete or inaccurate, you may have grounds to pursue additional action depending on your circumstances.

Knowing your legal protections also helps you distinguish between legitimate credit repair strategies and unrealistic promises.

Consider Filing Another Credit Dispute

A verified dispute is not always the end of the road.

If you have obtained new documentation or identified additional inaccuracies, filing another dispute may be appropriate.

Before doing so:

- Review the previous investigation results.

- Gather stronger supporting evidence.

- Clearly identify the specific reporting error.

- Explain why the previous verification was incorrect.

- Include copies—not originals—of your documentation.

Avoid sending the exact same dispute repeatedly without new information. Providing additional evidence or clarifying the issue gives the credit bureau and data furnisher more reason to conduct a meaningful review.

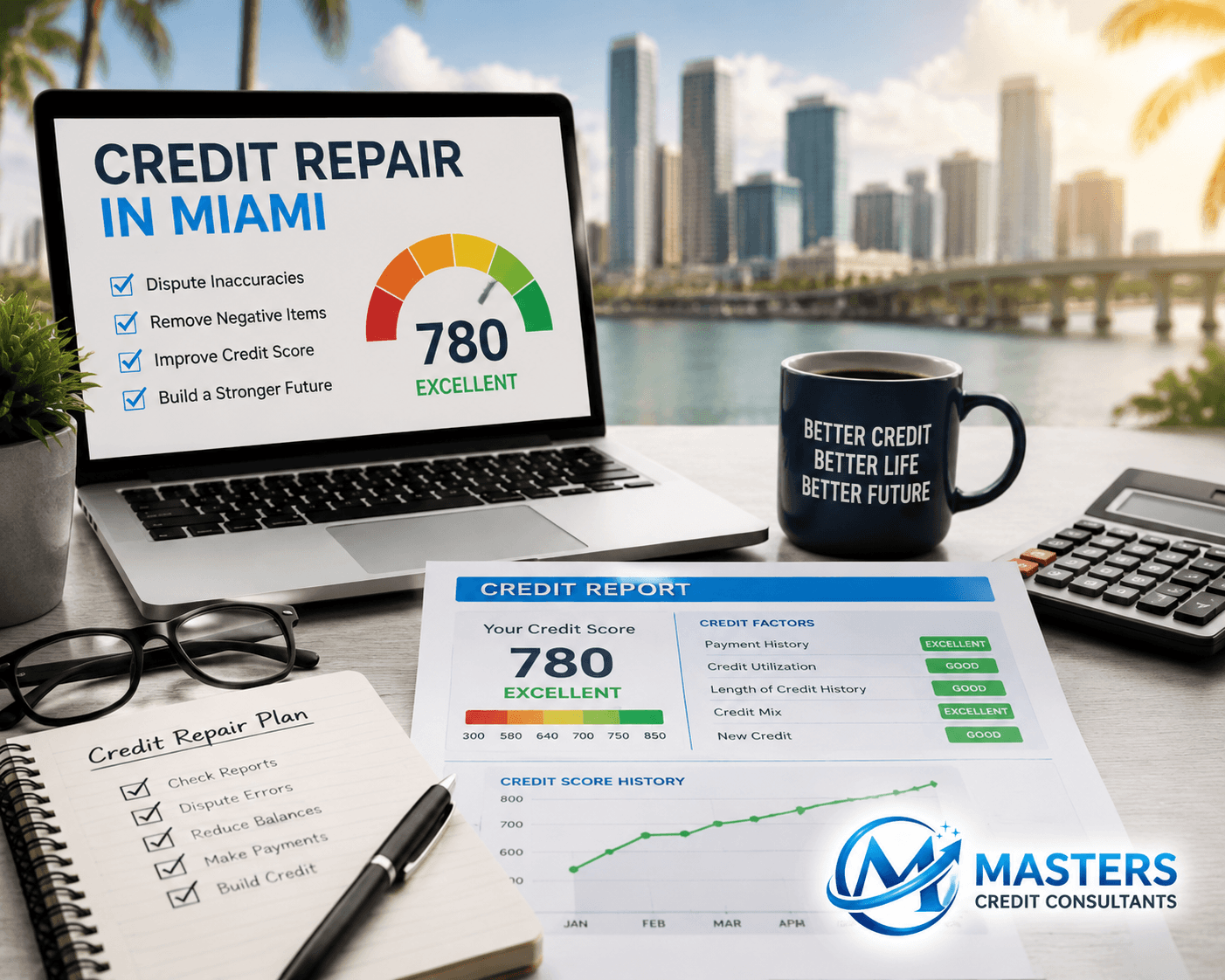

For individuals who find the process confusing or overwhelming, working with experienced credit repair services can provide guidance in reviewing reports, organizing documentation, and developing a strategy tailored to your situation. Whether you’re searching for a credit repair company near me, credit repair near me, or exploring Credit Repair Miami and Credit Repair Services Near Me, understanding your options is the first step toward making informed financial decisions.

When Should You Escalate a Credit Dispute?

If your dispute has been verified but you still believe the information is inaccurate, it may be time to escalate the matter. Escalating doesn’t mean becoming confrontational—it means using the proper channels to request a more thorough review.

Consider escalating your dispute if:

- You have new evidence that wasn’t included in your original dispute.

- The creditor failed to address the specific issue you raised.

- The same inaccurate information continues to appear after multiple investigations.

- You suspect identity theft or fraudulent activity.

- The account contains factual errors, such as incorrect dates, balances, or payment history.

Keep copies of every dispute letter, email, and supporting document. Maintaining a detailed paper trail can be invaluable if further action becomes necessary.

Stay organized by creating a folder for all dispute-related documents, investigation results, and correspondence. Good recordkeeping makes future disputes much easier.

Contact the Creditor Directly

Many consumers focus solely on the credit bureaus, but the company reporting the account can often resolve reporting issues directly.

When contacting the creditor:

- Clearly explain the reporting error.

- Include copies of supporting documents.

- Request a written investigation.

- Ask for written confirmation if corrections are made.

In some situations, resolving the issue directly with the furnisher is faster than repeatedly disputing through the credit bureaus.

Remain professional and factual. Emotional language rarely helps your case, while clear documentation often does.

Continue Building Positive Credit While Disputes Are Pending

Waiting for dispute results doesn’t mean your financial progress has to stop.

Positive credit habits can gradually strengthen your credit profile, even if some negative items remain.

Focus on:

- Paying every bill on time.

- Keeping credit card balances low.

- Avoiding unnecessary hard inquiries.

- Maintaining older credit accounts whenever possible.

- Monitoring your credit reports regularly.

- Creating a realistic monthly budget.

These habits demonstrate responsible credit management and contribute to long-term credit improvement.

Improve Your Credit Utilization Ratio

One of the fastest ways to improve many credit scores is by lowering your credit utilization ratio.

Credit utilization refers to the percentage of available revolving credit you’re using.

For example:

- Credit Limit: $10,000

- Current Balance: $8,000

- Utilization: 80%

Reducing that balance to $2,000 lowers your utilization to 20%, which is generally viewed much more favorably by scoring models.

Whenever possible:

- Pay balances before the statement closing date.

- Spread balances across multiple cards.

- Avoid maxing out credit cards.

- Request higher credit limits only when appropriate.

Even small improvements can make a noticeable difference over time.

Don’t Make These Common Credit Dispute Mistakes

Many verified disputes happen because consumers unknowingly weaken their own case.

Avoid these common mistakes:

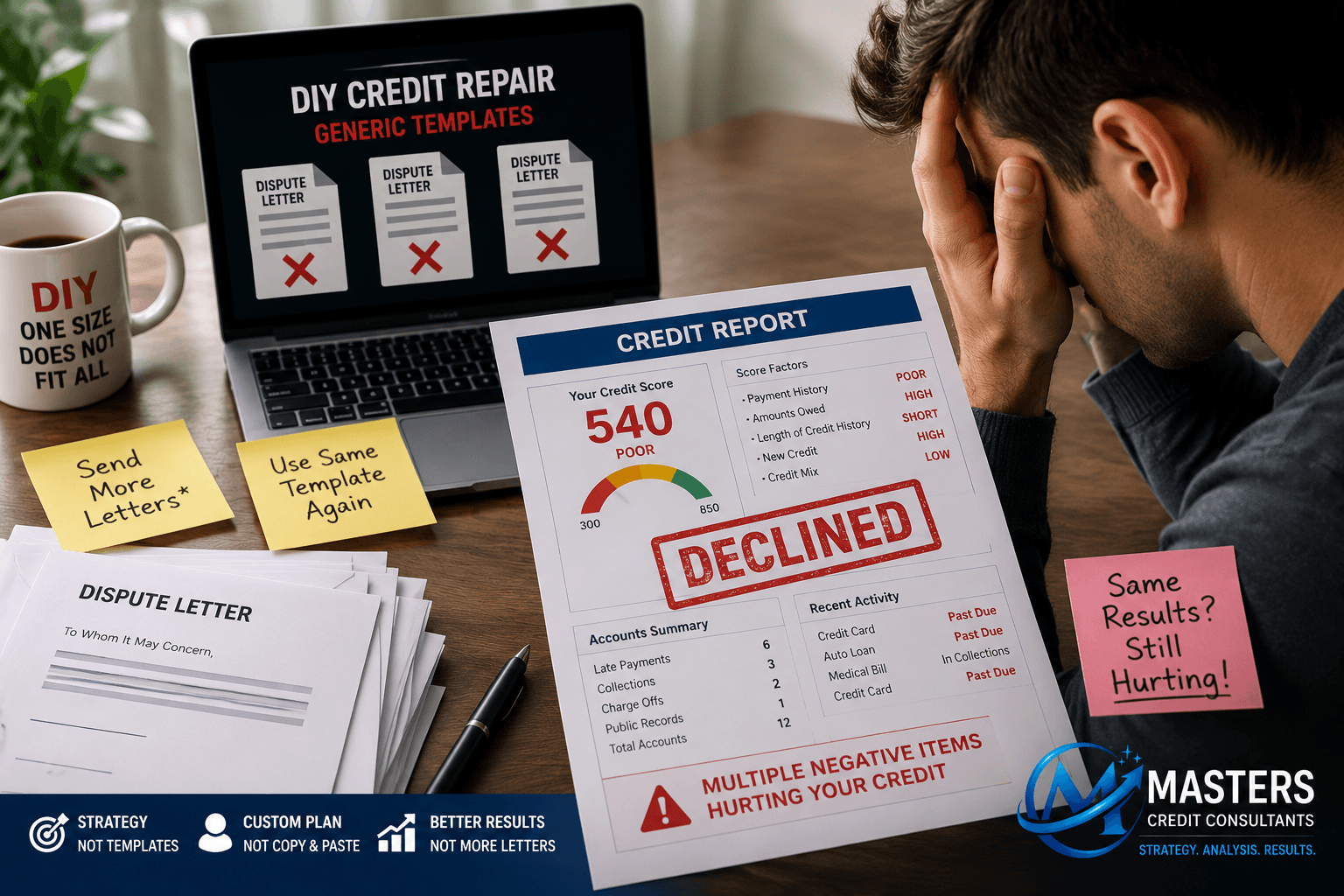

Filing Generic Disputes

Statements like “This account is wrong” provide little information.

Instead, identify the exact error and explain why it is inaccurate.

Disputing Accurate Information

Legitimate late payments or accurately reported balances usually cannot be removed simply because they negatively affect your score.

Focus your efforts on factual inaccuracies rather than accurate negative information.

Sending Incomplete Documentation

Supporting evidence is often the strongest part of a dispute.

Include:

- Statements

- Receipts

- Settlement letters

- Identity theft documentation

- Account correspondence

The stronger your evidence, the stronger your dispute.

Ignoring Future Credit Habits

Some consumers focus entirely on removing negative items while neglecting the behaviors that improve credit over time.

Remember that rebuilding credit involves both correcting errors and establishing positive financial habits.

How Professional Credit Repair Services May Help

Credit reporting laws can be complicated, especially when disputes become repetitive or involve multiple creditors.

Professional credit repair services may assist by:

- Reviewing your credit reports for inaccuracies.

- Identifying reporting inconsistencies.

- Organizing supporting documentation.

- Preparing dispute strategies.

- Monitoring investigation results.

- Providing education about credit improvement.

If you’ve searched for Credit Repair Services Near Me, credit repair company near me, Credit Repair Agencies, Credit Repair Services, or Credit Repair in Miami, choose a company that emphasizes transparency, education, and realistic expectations.

A reputable credit repair company should never promise to remove accurate information or guarantee a specific credit score increase.

Need Personalized Guidance?

Every credit situation is different. What works for one consumer may not be the best solution for another.

If you’re unsure about your next steps after a verified dispute, consider scheduling a professional consultation. An experienced credit specialist can review your credit reports, identify potential reporting issues, and recommend strategies tailored to your financial goals.

Whether you’re rebuilding your personal credit, preparing for a mortgage, financing a vehicle, or working toward business funding, having a customized plan can make the process more manageable.

Why Good Credit Matters for Entrepreneurs

Strong personal credit often creates opportunities beyond personal borrowing.

Entrepreneurs with healthier credit profiles may find it easier to:

- Qualify for business financing.

- Secure lower interest rates.

- Obtain business credit cards.

- Lease commercial property.

- Purchase equipment.

- Expand operations with greater financial flexibility.

Improving your credit isn’t just about increasing a score—it’s about creating more opportunities for your future.

Frequently Asked Questions About Credit Dispute

Can I dispute the same account more than once?

Yes. If you have new information or additional documentation that supports your claim, you may submit another dispute. Repeating the exact same dispute without new evidence is less likely to produce a different outcome.

Does “verified” mean the account is definitely correct?

No. Verification simply means the creditor confirmed the information currently matches its records. It does not automatically prove those records are free from errors.

How long does it take to improve my credit after a verified dispute?

The timeline varies depending on your overall credit profile. Consistently making on-time payments, reducing credit utilization, correcting reporting errors, and practicing responsible credit management can gradually improve your credit over time.

What does “Dispute Resolved; Consumer Disagrees” mean?

This comment generally indicates that a dispute investigation has been completed, but the consumer disagrees with the outcome.

It does not automatically mean the account can never be challenged again. It simply means the account already has dispute history that should be considered before deciding on the next step.

Does disputing an account hurt my credit score?

Simply filing a dispute does not, by itself, lower your credit score.

However, consumers should understand the dispute process before repeatedly challenging the same information, especially if previous investigations have already been completed.

Can I dispute the same account more than once?

Yes.

Whether another dispute is appropriate depends on the facts of your situation, including changes in reporting, new documentation, or other relevant information. Repeating the exact same dispute without any new basis may not lead to a different outcome.

Why was my dispute verified?

A verification generally means the investigation resulted in the information continuing to be reported.

That does not necessarily answer every question about the account. It simply reflects the outcome of that investigation based on the information reviewed at that time.

Should I dispute every negative account?

Not necessarily.

Each account should be evaluated individually. Different account types, reporting histories, and circumstances may call for different approaches.

Are online dispute templates effective?

Templates can be useful for organizing information and getting started.

However, they may not address the specific facts of every account, which is one reason many consumers eventually seek a more personalized review.

Why do some people see results while others don’t?

No two credit reports are exactly alike.

Factors such as account history, documentation, reporting accuracy, previous disputes, payment history, and creditor responses can all influence the outcome of a dispute.

Is professional credit repair just sending letters for me?

A reputable credit repair company generally does much more than mail dispute letters.

The process often includes reviewing the credit report, evaluating dispute history, identifying reporting inconsistencies, monitoring progress, educating the consumer, and adjusting strategies as circumstances change.

How long does credit repair take?

There is no universal timeline.

The length of the process depends on the complexity of the credit report, the number of accounts involved, investigation timelines, and each consumer’s overall financial situation.

Be cautious of anyone guaranteeing specific timeframes or results.

What should I do before disputing anything?

Before submitting a dispute:

- Review all credit reports:

- Experian, Equifax and TransUnion™ Reports & Scores Can Be Refreshed Every 30 Days

- 3 Bureau Daily Monitoring & Alerts

- Dark Web Monitoring

- $1,000,000 Identity Theft Insurance

- Verify the information being reported.

- Gather supporting documentation.

- Read any previous dispute comments.

- Understand why you’re disputing the account.

Preparation often matters as much as the dispute itself.

When should I consider professional help?

If you’ve already tried repairing your credit yourself and aren’t making progress—or your report contains multiple negative accounts, prior dispute history, or complicated reporting issues—it may be beneficial to have your credit profile reviewed by an experienced professional.

Final Thoughts

Receiving a “verified” response after submitting a credit dispute can feel discouraging, but it doesn’t necessarily mean you’ve reached the end of the process.

Take time to review your credit reports carefully, strengthen your documentation, and determine whether additional action is appropriate. Sometimes the issue lies not in the dispute itself, but in the evidence presented or the reporting practices of the creditor.

At the same time, continue building positive financial habits. Responsible credit management, timely payments, and lower credit utilization can have a lasting impact on your overall credit health regardless of the outcome of a single dispute.

If you need experienced guidance, Masters Credit is a trusted credit repair company dedicated to helping individuals and entrepreneurs repair their credit, improve their credit score faster through proven strategies, meet their unique credit needs, and prepare for future financial opportunities. Whether you’re working toward homeownership, business funding, or long-term financial stability, a strategic credit improvement plan can help you move forward with greater confidence.

Schedule Your Free Credit Consultation with Masters Credit Consultants

If you are trying to improve your credit after a verified dispute in 2026, professional guidance may help you identify reporting errors and create a personalized recovery strategy.

📞 Phone: 1-844-620-8796

🌐 Website: https://www.masterscredit.com

📅 Schedule Your Free Consultation:

https://www.masterscredit.com/sign-up/

Additional Helpful Links

- Ultimate Guide to Credit Repair: A Proven Blueprint to Rebuild Your Credit and Create More Financial Opportunities

- DIY Credit Repair May Be Hurting Your Credit: Why Strategy Matters More Than Templates

- Credit repair in Miami: Secrets to Boost Score Fast (2026 Guide)

- Credit Repair Atlanta: Rejected Again? Here’s Why

Related Questions

- Can I dispute the same item on my credit report after it has been verified?

- What does “verified as accurate” mean on a credit dispute?

- How do I remove a verified collection account from my credit report?

- What should I do if the credit bureau verifies incorrect information?

- Will a verified credit dispute hurt my credit score?

- Should I hire a credit repair company if my dispute was verified?

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment