How Credit Bureaus Investigate Credit Disputes: A Complete Guide to Understanding the Process (2026)

When you file a credit dispute, credit bureaus such as Experian, Equifax, and TransUnion investigate by contacting the company that reported the information (known as the data furnisher). They review the evidence provided, verify the account details, and determine whether the disputed information should be corrected, updated, or remain unchanged. Most investigations are completed within 30 days, although additional time may apply in certain situations.

In This Article You’ll Learn

- How credit bureaus investigate credit disputes from start to finish.

- What happens after you submit a dispute and why some disputes succeed while others don’t.

- Practical strategies to improve your chances of correcting inaccurate credit report information.

Table of Contents

- What Is a Credit Dispute?

- Who Are the Three Major Credit Bureaus?

- How Credit Bureaus Investigate Credit Disputes

- The Credit Dispute Investigation Timeline

- How Data Furnishers Respond to Disputes

- What Evidence Makes a Credit Dispute Stronger?

- Common Reasons Credit Disputes Are Verified

- How to Improve Your Chances of Success

- When Professional Credit Repair Services Can Help

- People Also Ask

- Final Thoughts

What Is a Credit Dispute?

A credit dispute is a formal request asking a credit bureau to investigate information on your credit report that you believe is inaccurate, incomplete, outdated, or the result of fraud.

Rather than immediately changing your report, the bureau must investigate the disputed information before making any updates.

This process protects both consumers and lenders by helping ensure that credit reports remain as accurate as possible.

If you’ve searched for credit repair near me or credit repair services, chances are you’re looking for guidance on navigating this process effectively. A reputable credit fixing service can help review your credit report, identify potential reporting errors, and explain your available options. Learn more about professional credit assistance at https://www.masterscredit.com/.

Credit bureaus investigate disputes by forwarding the disputed information to the company that reported the account. The furnisher reviews its records, responds to the bureau, and the bureau determines whether the information should remain, be corrected, or be removed. Most investigations are completed within 30 days.

Who Are the Three Major Credit Bureaus?

The United States has three nationwide credit bureaus that collect and maintain consumer credit information.

Although these bureaus often contain similar information, your credit reports may not be identical because creditors are not required to report to all three.

This is why it’s important to review each report separately when identifying errors.

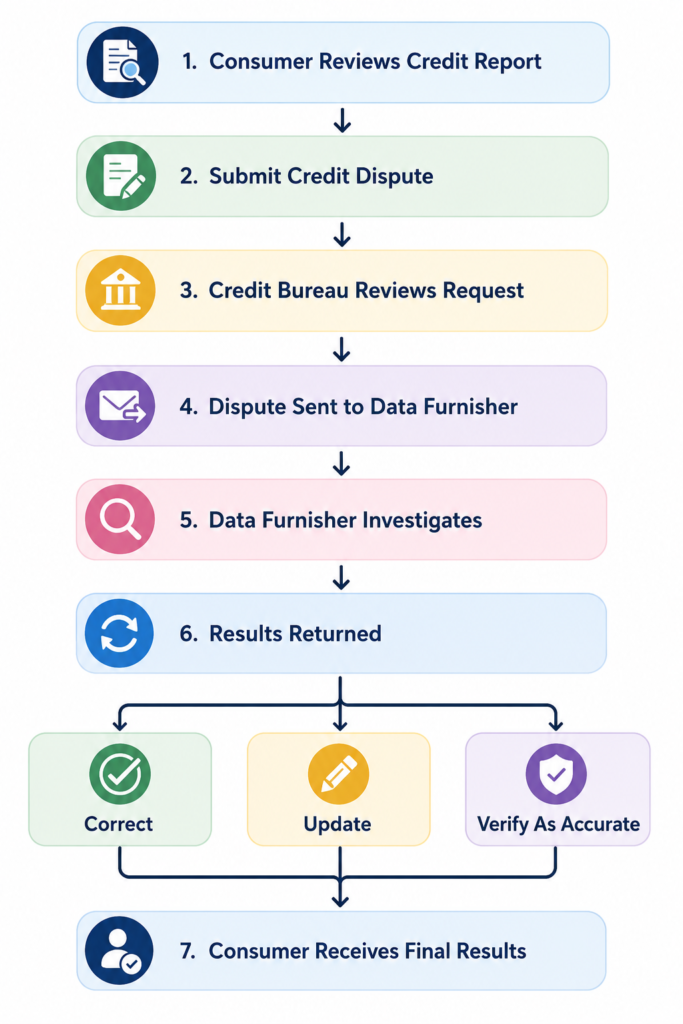

How Credit Bureaus Investigate Credit Disputes

Many consumers assume that credit bureaus manually investigate every account themselves.

In reality, the process is more structured and involves communication between the bureau and the company that originally reported the account.

The investigation generally follows these steps:

1. Your Dispute Is Submitted

You submit a dispute through:

- Online dispute portal

- Certified mail

- Telephone (less recommended)

- Professional credit repair representative

Providing supporting documentation at this stage can significantly strengthen your dispute.

2. The Bureau Reviews Your Submission

The bureau checks whether your dispute contains enough information to begin an investigation.

Helpful documents include:

- Government-issued identification

- Utility bills

- Payment receipts

- Bank statements

- Court records

- Identity theft reports

- Collection settlement letters

The more specific your documentation, the easier it becomes to verify your claim.

3. The Information Is Sent to the Data Furnisher

Once accepted, the bureau forwards your dispute to the company reporting the account.

This company is called the data furnisher.

Examples include:

- Banks

- Credit card companies

- Auto lenders

- Mortgage companies

- Collection agencies

- Student loan servicers

The furnisher is responsible for reviewing its records and responding with supporting evidence.

Credit Dispute Investigation Flow

Understanding the Investigation Timeline

Although every dispute is different, most follow a predictable timeline.

If you submit additional documentation during the investigation, the bureau may require additional time as permitted under the Fair Credit Reporting Act (FCRA).

Keep copies of every dispute letter, supporting document, and response you receive. Organized records can make future disputes easier and provide valuable evidence if further action becomes necessary.

Why Documentation Matters

One of the biggest misconceptions about credit disputes is that simply stating “this account is wrong” is enough.

In reality, documentation often determines whether a dispute succeeds.

For example, if you claim that a late payment was reported incorrectly, providing canceled checks, bank statements, or payment confirmations gives investigators concrete evidence to review.

Strong documentation can help distinguish legitimate disputes from unsupported claims.

Factors That Strengthen a Credit Dispute

For entrepreneurs and small business owners, maintaining an accurate personal credit report is more than a financial housekeeping task—it can directly influence access to business financing, equipment loans, commercial leases, and favorable lending terms. Addressing credit report inaccuracies early may help position your business for future growth opportunities.

How Data Furnishers Respond to Credit Disputes

Once a credit bureau receives your dispute, it doesn’t make an immediate decision about whether the information should be changed. Instead, the bureau contacts the company that reported the account—known as the data furnisher—and requests verification.

A data furnisher may be:

- Banks

- Credit card issuers

- Mortgage lenders

- Auto finance companies

- Collection agencies

- Student loan servicers

- Credit unions

The furnisher is legally responsible for reviewing its records and responding with accurate information. If it cannot verify the disputed information, the Fair Credit Reporting Act (FCRA) generally requires that the inaccurate information be corrected or removed.

What Information Does a Data Furnisher Review?

The investigation often includes a review of the company’s internal records.

Typical documents include:

- Original credit applications

- Payment history

- Signed contracts

- Electronic account records

- Billing statements

- Collection notes

- Correspondence with the consumer

The furnisher compares your dispute with its own records before responding to the credit bureau.

How Credit Bureaus Communicate with Creditors

Many consumers imagine that credit bureaus manually call every creditor during an investigation. In reality, much of the dispute process is electronic.

The three nationwide credit bureaus commonly use an automated communication platform to exchange dispute information with participating data furnishers. This allows disputes to move through the investigation process efficiently while maintaining standardized reporting procedures.

The system typically includes:

- Consumer dispute codes

- Supporting information

- Account identifiers

- Requested investigation actions

- Final response from the furnisher

This standardized workflow helps ensure disputes are processed consistently across millions of credit records each year.

Why Some Credit Disputes Are Verified

One of the most common questions consumers ask is:

“Why was my dispute verified if I know the information is wrong?”

Verification simply means the data furnisher responded that, based on its available records, the information is accurate.

It does not necessarily mean every aspect of the account has been independently reviewed by the credit bureau.

Several situations can lead to verification.

The Information Is Actually Accurate

Sometimes consumers misunderstand how an account should appear.

Examples include:

- A legitimate late payment

- A correctly reported collection account

- An accurate balance

- A valid charge-off

In these cases, the bureau will typically leave the account unchanged.

Insufficient Supporting Documentation

A dispute without evidence is much harder to evaluate.

For example:

❌ “This account isn’t mine.”

versus

✅ Police report

✅ Identity theft affidavit

✅ Driver’s license

✅ Utility bill

The second dispute gives investigators substantially more information to review.

The Wrong Reason Was Selected

Many online dispute portals ask consumers to choose from a list of dispute reasons.

Selecting an inaccurate reason may slow the investigation or make it more difficult for the furnisher to understand your claim.

Being specific—and including a clear written explanation—can improve communication.

Duplicate or Frivolous Disputes

Submitting the same dispute repeatedly without providing new evidence generally does not strengthen your case.

Instead, it may delay the process or result in the bureau determining that no additional investigation is necessary.

If new documentation becomes available, include it with any subsequent dispute.

Focus on factual inaccuracies rather than simply requesting account removal. Clear documentation and specific explanations often lead to stronger dispute outcomes.

Common Reasons Credit Disputes Are Successful

Although not every dispute results in changes, many consumers successfully correct inaccurate reporting.

Common examples include:

- Identity theft accounts

- Duplicate collection accounts

- Incorrect account balances

- Accounts belonging to another consumer

- Incorrect payment dates

- Incorrect late payment history

- Paid collections still reported as unpaid

- Accounts reported beyond the legal reporting period

- Incorrect personal identifying information

Many of these errors occur because information passes through multiple systems before appearing on a credit report.

Most Frequently Corrected Credit Report Errors

What Happens After the Investigation?

After reviewing the furnisher’s response, the credit bureau determines the appropriate action.

Generally, one of four outcomes occurs.

The bureau then sends you the results of the investigation, usually by mail or through your online dispute portal.

If changes were made, your updated credit report should reflect those corrections.

Your Rights Under the Fair Credit Reporting Act (FCRA)

The Fair Credit Reporting Act gives consumers important rights during the credit dispute process.

These rights help promote fair and accurate credit reporting.

As a consumer, you generally have the right to:

- Dispute inaccurate information.

- Receive the results of an investigation.

- Obtain a corrected credit report when changes are made.

- Add a consumer statement in certain situations.

- Dispute directly with the data furnisher.

- Request free copies of your credit reports under qualifying circumstances.

Understanding these rights allows you to participate more confidently in the dispute process.

The FCRA is designed to promote accuracy, fairness, and privacy in consumer credit reporting. While it doesn’t guarantee that every dispute will result in a deletion, it does require credit bureaus and data furnishers to investigate legitimate disputes and correct information that cannot be verified.

Can You Improve Your Chances of a Successful Credit Dispute?

Yes. While no outcome is guaranteed, certain best practices can strengthen your dispute.

Consider these recommendations:

- Review all three credit reports before filing.

- Clearly identify the specific error.

- Include supporting documentation whenever possible.

- Keep copies of everything you submit.

- Follow up if you don’t receive a response within the expected timeframe.

- Avoid submitting generic or repetitive disputes without new evidence.

- Monitor your reports after the investigation is complete.

These steps help create a more organized and persuasive dispute.

If you’re reviewing your credit reports and aren’t sure whether an item is being reported accurately, it may be helpful to seek professional guidance before filing multiple disputes. A knowledgeable credit professional can review your reports, explain your options, and help you determine an appropriate strategy based on your unique financial goals.

If you’d like personalized assistance, you can schedule a consultation through https://www.masterscredit.com/sign-up/ to discuss your credit profile and next steps.

A clean and accurate credit report isn’t just important for personal finances—it can also influence business loan approvals, vendor financing, commercial leases, and startup funding opportunities. Correcting reporting errors today can help strengthen your financial foundation for future business growth.

Common Mistakes People Make When Filing Credit Disputes

Filing a credit dispute may seem straightforward, but many disputes are delayed or denied because consumers make avoidable mistakes. Understanding these common pitfalls can save time and improve the quality of your dispute.

One of the biggest misconceptions is believing that simply disputing an account will automatically remove it from your credit report. Credit bureaus do not delete accurate information simply because it has been challenged. Instead, they investigate whether the information is complete, accurate, and verifiable.

Let’s look at some of the most common mistakes.

Filing a Dispute Without Reviewing Your Entire Credit Report

Many consumers immediately dispute an account after seeing something they don’t recognize.

However, it’s important to review your entire credit report before submitting a dispute.

You may discover:

- Duplicate accounts

- Incorrect personal information

- Mixed credit files

- Multiple reporting errors from the same creditor

- Identity theft indicators

Reviewing the complete report helps you build a stronger, more organized dispute rather than filing multiple separate disputes.

Disputing Accurate Information

Not every negative account is an error.

For example:

- A legitimate late payment

- A valid collection account

- An accurate charge-off

- Correctly reported credit utilization

These items generally cannot be removed simply because they negatively affect your credit score.

Instead, disputes should focus on information that is:

- Incorrect

- Incomplete

- Outdated

- Fraudulent

- Unable to be verified

Providing Little or No Documentation

Supporting evidence is one of the strongest parts of any dispute.

Examples include:

- Bank statements

- Payment confirmations

- Identity theft reports

- Settlement agreements

- Account closure letters

- Court documents

Without documentation, investigators often have little information beyond your statement.

Sending Generic Dispute Letters

Many online templates contain the exact same language.

Credit bureaus process millions of disputes each year.

A personalized dispute that clearly explains:

- what is incorrect,

- why it is incorrect,

- and what documentation supports your claim,

is generally more helpful than a copied template.

Submitting Multiple Disputes at the Same Time

Some consumers believe repeatedly disputing the same account increases the likelihood of removal.

In reality, duplicate disputes without new evidence may delay the process.

Quality is usually more important than quantity.

DIY Credit Repair vs. Professional Credit Repair Services

Many consumers wonder whether they should handle disputes on their own or work with a professional.

The answer depends on the complexity of the situation.

Simple errors may be easy to resolve independently, while more complicated cases involving identity theft, multiple creditors, or inconsistent reporting may benefit from professional guidance.

Neither option guarantees a specific outcome. The right choice depends on your goals, available time, and comfort level with the dispute process.

If you’re researching Credit Repair Services Near Me, Credit Repair Agencies, Credit Repair Miami, or a trusted credit repair company near me, look for organizations that emphasize transparency, education, and compliance rather than unrealistic promises.

You can also explore the educational resources available through Masters Credit Consultants at https://www.masterscredit.com/.

How Accurate Credit Reports Support Business Growth

For entrepreneurs, your personal credit history often plays a larger role than you might expect.

Many lenders evaluate personal credit before approving:

- Business credit cards

- Startup loans

- SBA-backed financing

- Equipment financing

- Commercial vehicle loans

- Vendor credit accounts

- Commercial leases

An inaccurate late payment or collection account could reduce financing opportunities or result in higher interest rates.

That’s why addressing legitimate reporting errors is an important part of preparing for business growth.

When Should You Consider Professional Help?

There are situations where additional guidance may be beneficial.

Examples include:

- Multiple inaccurate accounts

- Identity theft

- Mixed credit files

- Repeated verification of information you believe is incorrect

- Collection agency reporting inconsistencies

- Preparing for a mortgage

- Preparing to launch a business

- Seeking business funding

Professional assistance should focus on helping you understand your rights, organize documentation, and navigate the dispute process—not promising guaranteed deletions.

Need Help Understanding Your Credit Report?

If you’re uncertain about how to proceed after receiving dispute results, a professional review may help clarify your options.

Scheduling a consultation can provide insight into your current credit profile, identify potential reporting concerns, and help you develop a strategy aligned with your financial and business goals.

Learn more by visiting:

https://www.masterscredit.com/sign-up/

Frequently Asked Questions

How long does a credit bureau take to investigate a dispute?

Most credit bureaus complete investigations within 30 days after receiving a dispute. In some cases, additional time may be allowed if new information is submitted during the investigation. Once the review is complete, you’ll receive written notice explaining whether the disputed information was verified, updated, corrected, or removed.

Can a credit bureau remove accurate negative information?

Generally, no. Credit bureaus are responsible for maintaining accurate credit reports. If a lender verifies that the reported information is correct, the account typically remains. Only inaccurate, incomplete, outdated, or unverified information is eligible for correction or removal under applicable credit reporting laws.

What happens if my credit dispute is verified?

If your dispute is verified, the information usually stays on your credit report because the data furnisher confirmed its accuracy based on available records. If you later obtain additional documentation supporting your claim, you may submit another dispute or communicate directly with the creditor.

Final Thoughts

Understanding how credit bureaus investigate credit disputes empowers you to make informed financial decisions. While the dispute process may seem complex, it follows a structured framework designed to promote fair and accurate credit reporting.

The most successful disputes are typically supported by clear documentation, accurate information, and a well-organized explanation of the issue. Rather than relying on myths or shortcuts, focus on understanding your credit reports, exercising your rights under the Fair Credit Reporting Act, and maintaining complete financial records.

For entrepreneurs, accurate credit reporting can have an even greater impact. Your personal credit profile may influence access to startup funding, business credit, equipment financing, commercial leases, and future growth opportunities. Addressing legitimate reporting errors today can help build a stronger financial foundation for tomorrow.

Masters Credit Consultants is committed to helping individuals and entrepreneurs better understand the credit reporting process. Through educational resources, personalized guidance, and responsible credit repair strategies, Masters Credit helps clients improve their credit profile, prepare for financing opportunities, strengthen business readiness, and work toward long-term financial success.

Schedule Your Free Credit Consultation with Masters Credit Consultants

If you are trying to improve your credit after a verified dispute in 2026, professional guidance may help you identify reporting errors and create a personalized recovery strategy.

📞 Phone: 1-844-620-8796

🌐 Website: https://www.masterscredit.com

📅 Schedule Your Free Consultation:

https://www.masterscredit.com/sign-up/

Additional Helpful Links

- Ultimate Guide to Credit Repair: A Proven Blueprint to Rebuild Your Credit and Create More Financial Opportunities

- DIY Credit Repair May Be Hurting Your Credit: Why Strategy Matters More Than Templates

- Credit repair in Miami: Secrets to Boost Score Fast (2026 Guide)

- Credit Repair Atlanta: Rejected Again? Here’s Why

Related Questions

- How long do credit bureaus take to investigate a credit dispute?

- What happens after you file a credit dispute?

- How do credit bureaus verify disputed information?

- What evidence should I include in a credit dispute?

- Why was my credit dispute verified instead of removed?

- Can a credit bureau remove accurate negative information?

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave A Comment